Assessing Northrop Grumman (NOC) Valuation After A Strong Recent Share Price Run

Northrop Grumman Corp. NOC | 702.50 | +0.79% |

What recent performance says about Northrop Grumman (NOC)

Without a single defining news headline driving trading, Northrop Grumman (NOC) has still drawn attention after a recent move in its share price, paired with solid trailing returns and multi segment exposure across aerospace and defense.

At a share price of $695.35, Northrop Grumman has recently shown strong momentum, with a 21.02% 1 month share price return and a 46.35% 1 year total shareholder return, pointing to improving sentiment around its long term prospects and risk profile.

If Northrop Grumman’s recent run has caught your eye, it could be a good moment to see what else is moving across aerospace and defense stocks as the sector reshapes.

With Northrop Grumman trading at $695.35, only about 3% below the average analyst price target and carrying a middling value score of 3, you have to ask yourself whether there is still a buying opportunity here or if the market is already pricing in future growth.

Most Popular Narrative: 2.2% Overvalued

Northrop Grumman’s fair value in the most followed narrative sits at about $680.44, slightly below the current $695.35 share price. This frames a modest premium and puts the focus on what is driving that gap.

Analysts have lifted their price targets for Northrop Grumman, supporting a fair value move from about $665.20 to roughly $680.44 as they factor in updated sector views, modestly higher projected revenue growth, profit margins, and future P/E assumptions.

Curious what kind of revenue path, margin profile, and future earnings multiple need to line up to reach that fair value? The full narrative lays out the cash flow story in detail and shows how a relatively small tweak to growth and profitability assumptions can shift the valuation more than you might expect.

Result: Fair Value of $680.44 (OVERVALUED)

However, the story can change quickly if major U.S. defense programs face budget cuts or if tighter rules on buybacks limit support for EPS.

Another View: Earnings Multiple Paints A Different Picture

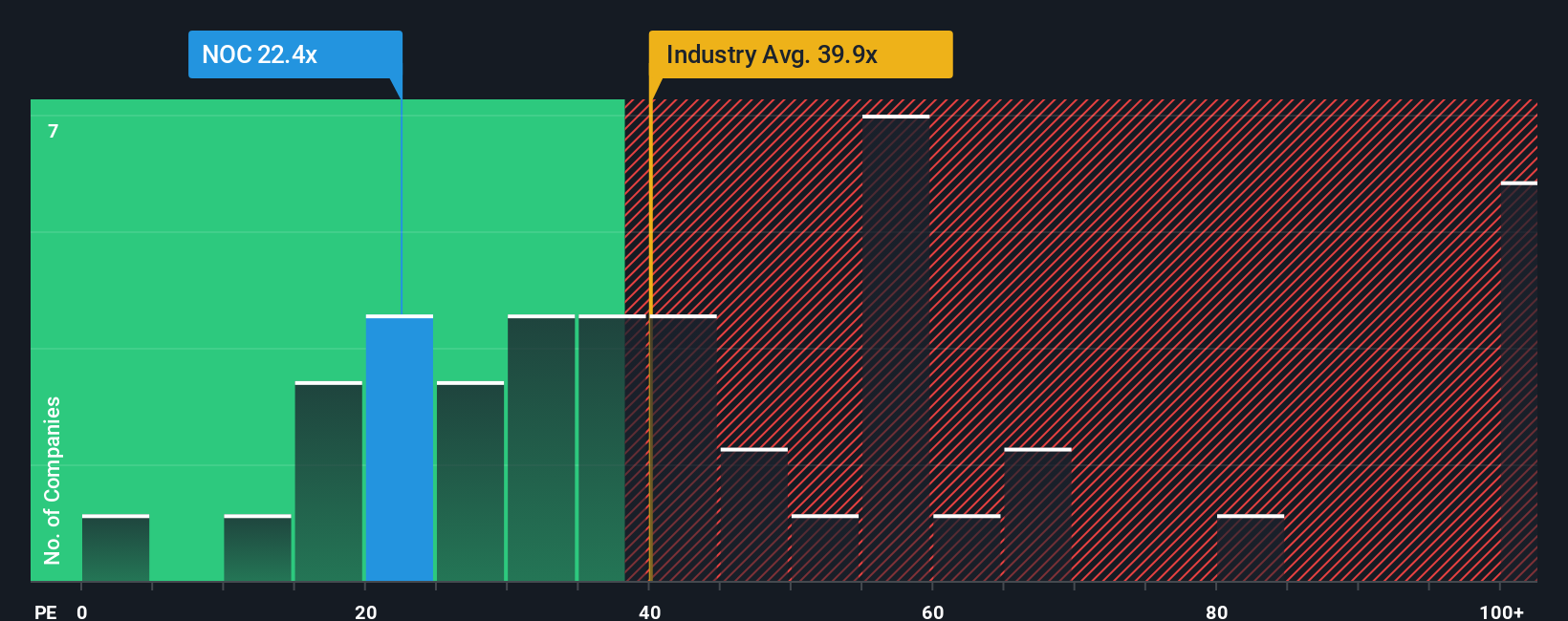

While the narrative model suggests Northrop Grumman is 2.2% overvalued, its current P/E of 23.6x tells a softer story. That multiple sits well below the US Aerospace & Defense industry at 41.5x, the peer average at 38.1x, and even the 27.5x fair ratio our work points to, which reduces the risk of paying an extreme price for each dollar of earnings. So if one framework says the shares are a touch rich, how much weight do you put on a market multiple that still looks restrained?

Build Your Own Northrop Grumman Narrative

If you look at the numbers and reach a different conclusion, or simply prefer to test your own assumptions against the data, you can build a tailored view in just a few minutes with Do it your way.

A great starting point for your Northrop Grumman research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Now that you have a handle on Northrop Grumman, do not stop there. Broaden your watchlist so you are not relying on a single opportunity.

- Spot potential bargains early by checking out these 865 undervalued stocks based on cash flows that appear attractively priced relative to their cash flows and underlying fundamentals.

- Tap into fast moving themes by scanning these 23 AI penny stocks that are tied to artificial intelligence and related growth stories.

- Strengthen your income focus by reviewing these 14 dividend stocks with yields > 3% that currently offer yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.