Assessing Northrop Grumman (NOC) Valuation After Earnings Strength And New Defense Contract Wins

Northrop Grumman Corp. NOC | 702.50 | +0.79% |

Northrop Grumman (NOC) is back in focus after reporting full year 2025 earnings, with revenue of US$41.954b and net income of US$4.182b, along with new defense contract wins in microelectronics and threat training systems.

The earnings release and fresh contracts in microelectronics and threat training systems come after a strong run in the shares, with a 30 day share price return of 14.1% and a 1 year total shareholder return of 51.9%, which suggests momentum has been building recently.

If this defense news has you thinking more broadly about future tech, you may want to scan our list of 28 robotics and automation stocks as another source of potential ideas.

With Northrop Grumman now trading at US$696.5, only about 4% below the average analyst price target of roughly US$721, the key question is obvious: is there still an opportunity here or is the market already pricing in future growth?

Most Popular Narrative: 2.4% Overvalued

Northrop Grumman's most followed narrative points to a fair value of about $680.44, slightly below the current $696.5 share price, which keeps attention on the assumptions sitting behind those cash flow projections.

Supportive government actions to remove regulatory and contractual barriers are leading to faster program execution and improved incentives, which, coupled with targeted capital investments and a strong backlog, are expected to improve earnings stability, free cash flow, and long-term profitability.

For readers curious about what earnings path and margin profile need to hold for that fair value to align with the current price, and how much future P/E expansion is incorporated, the full narrative lays out those moving parts in detail.

Result: Fair Value of $680.44 (OVERVALUED)

However, those fair value assumptions could crack if large U.S. programs like B 21 or Sentinel hit delays, or if tighter buyback rules cap future price-to-earnings (P/E) expansion.

Another View: Market Multiple Points a Different Way

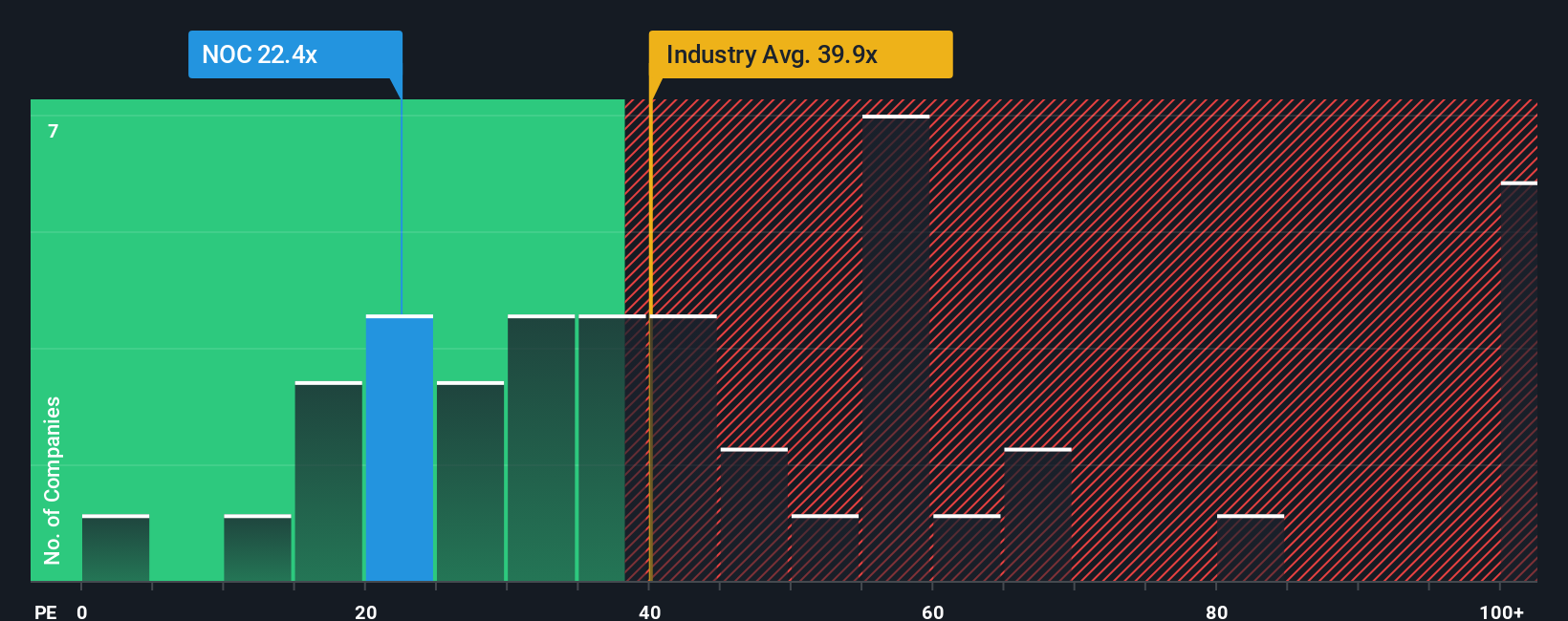

That 2.4% DCF based premium is only part of the story. On a P/E of 23.6x, Northrop Grumman sits well below both the US Aerospace & Defense industry at 40.1x and the peer average at 37x, and also below its own fair ratio of 30.1x. In practice, that gap suggests the market is currently pricing in less valuation risk than the DCF result implies. This raises the question of which signal is more informative for the next move.

Build Your Own Northrop Grumman Narrative

If you see the numbers differently or prefer to piece together your own view from the ground up, you can build a custom thesis in just a few minutes with Do it your way.

A great starting point for your Northrop Grumman research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investing ideas?

If Northrop Grumman is on your radar, do not stop there. A broader watchlist of opportunities from our screeners can help round out your research.

- Spot potential value plays by checking companies our screener flags as 55 high quality undervalued stocks that may warrant a closer look.

- Prioritise resilience with our list of 81 resilient stocks with low risk scores that score well on lower risk characteristics.

- Hunt for lesser known potential opportunities in our screener containing 25 high quality undiscovered gems that many investors may not be watching yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.