Assessing Nucor (NUE) Valuation After Earnings Miss And 2026 Growth Guidance

Nucor Corporation NUE | 172.46 | -0.73% |

Nucor (NUE) is back in focus after its fourth quarter and full year 2025 results came in below analyst earnings projections, prompting a negative market reaction and sharpening attention on the company’s 2026 guidance.

The mixed reaction to Nucor’s earnings and 2026 outlook sits against a strong recent run, with a 30 day share price return of 9.17% and a 1 year total shareholder return of 42.09%. This points to momentum building over the longer term, despite short term volatility.

If this earnings story has you thinking more broadly about industrial exposure, it could be a good time to review other materials heavy names and related sectors, using fast growing stocks with high insider ownership as a starting point.

With Nucor trading close to its US$185 price target and carrying a high value score alongside a large intrinsic discount, the key question is simple: are you looking at an underappreciated compounding story, or a stock that already reflects future growth?

Most Popular Narrative: 1.4% Undervalued

Against Nucor’s last close of $179.91, the most followed narrative pegs fair value at about $182.38, using a detailed cash flow and margin outlook.

Nucor's significant capital reinvestment of $860 million, with two-thirds directed towards projects commencing operations within two years, is expected to diversify and strengthen future earnings. This impacts revenue and net margins through enhanced production capacity and efficiencies.

Curious what kind of revenue path, margin rebuild, and future earnings multiple are needed to get to that fair value number? The full narrative lays out a step by step financial path, including how capital spending, pricing assumptions, and future valuation multiples fit together into a single number.

Result: Fair Value of $182.38 (UNDERVALUED)

However, you still need to weigh the risk that weaker steel demand or hiccups in bringing new mills online could challenge those margin and earnings assumptions.

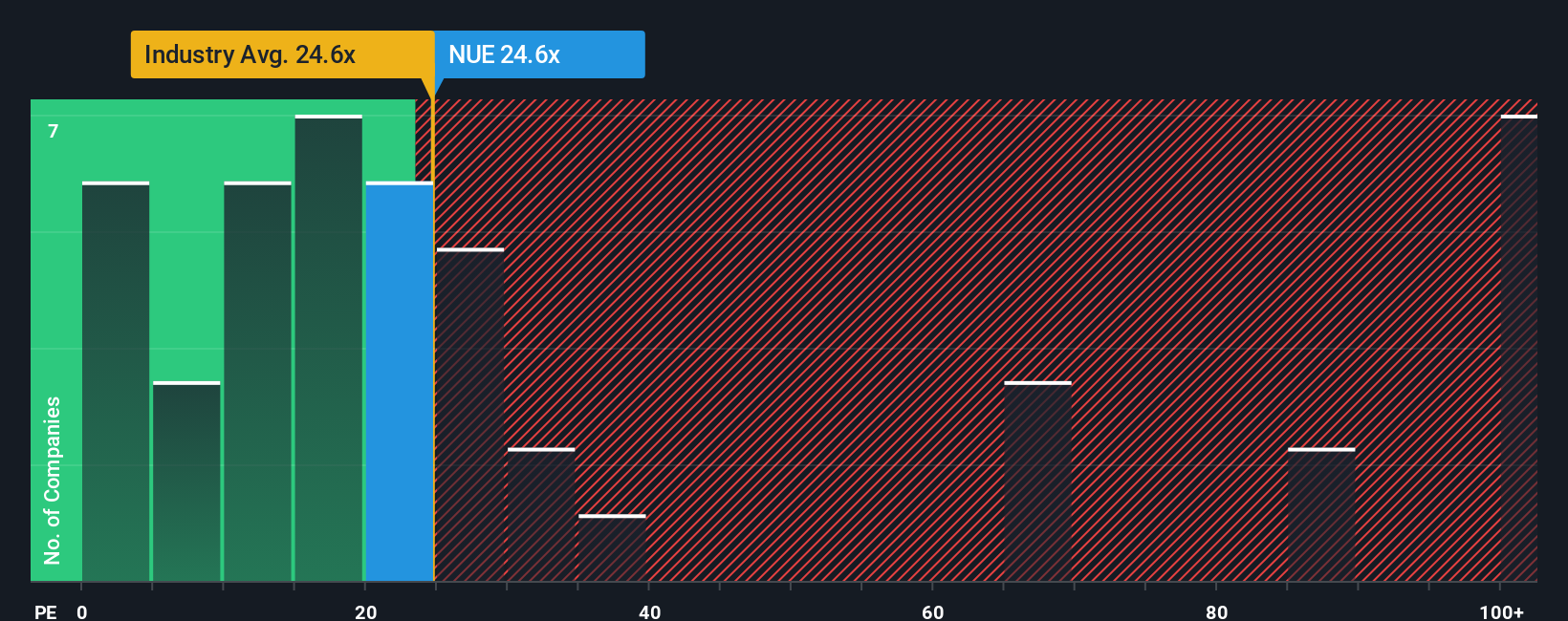

Another Angle: What The P/E Says

That 1.4% undervaluation story sits awkwardly next to the P/E picture. Nucor trades on 23.6x earnings, richer than the 20.2x peer average, yet below the US Metals and Mining average of 26x and a fair ratio of 27.5x that our model suggests the market could move toward.

This mix of higher pricing than peers, but a discount to the fair ratio, leaves you with a simple question: do you see more valuation risk if sentiment cools, or room for the multiple to catch up if earnings progress as expected?

Build Your Own Nucor Narrative

If the assumptions here do not align with your perspective, or you would rather develop your own thesis from the data, you can create a complete narrative in just a few minutes with Do it your way.

A great starting point for your Nucor research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If you are serious about building a stronger watchlist, do not stop at a single stock. Use these focused screens to surface more potential candidates today.

- Target income focused opportunities by scanning these 14 dividend stocks with yields > 3% that may suit investors who want yield alongside equity exposure.

- Tap into potential pricing gaps by reviewing these 865 undervalued stocks based on cash flows that might offer more appealing entry points based on cash flow estimates.

- Get ahead of long term tech shifts by checking out these 24 quantum computing stocks shaping future computing themes before they become crowded trades.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.