Assessing Nuvation Bio (NUVB) Valuation After The Eisai Taletrectinib Partnership Announcement

NUVATION BIO INC NUVB | 4.41 | -2.22% |

What the Eisai partnership means for Nuvation Bio

Nuvation Bio (NUVB) has drawn fresh attention after signing an exclusive license and collaboration agreement with Eisai covering taletrectinib for ROS1-positive non small cell lung cancer across multiple international markets.

Under the deal, Nuvation Bio is set to receive an upfront payment of €50 million, potential regulatory and commercial milestones of up to €145 million, and double digit tiered royalties on future net sales in Eisai’s licensed territories.

The Eisai agreement lands after a sharp 40.53% 1 month share price decline and a 5.41% 1 day drop to US$5.59. However, the 1 year total shareholder return of 121.83% and 3 year total shareholder return of roughly 2.3x suggest longer term momentum has previously been strong, even as recent share price performance has cooled.

If this deal has you looking across oncology and drug development, it could be a useful moment to scan other healthcare stocks that might fit your watchlist next.

With the Eisai deal in place, a 1 year total return above 120% and a recent 1 month slide of more than 40%, you have to ask yourself: is Nuvation Bio mispriced today, or is the market already assuming future growth?

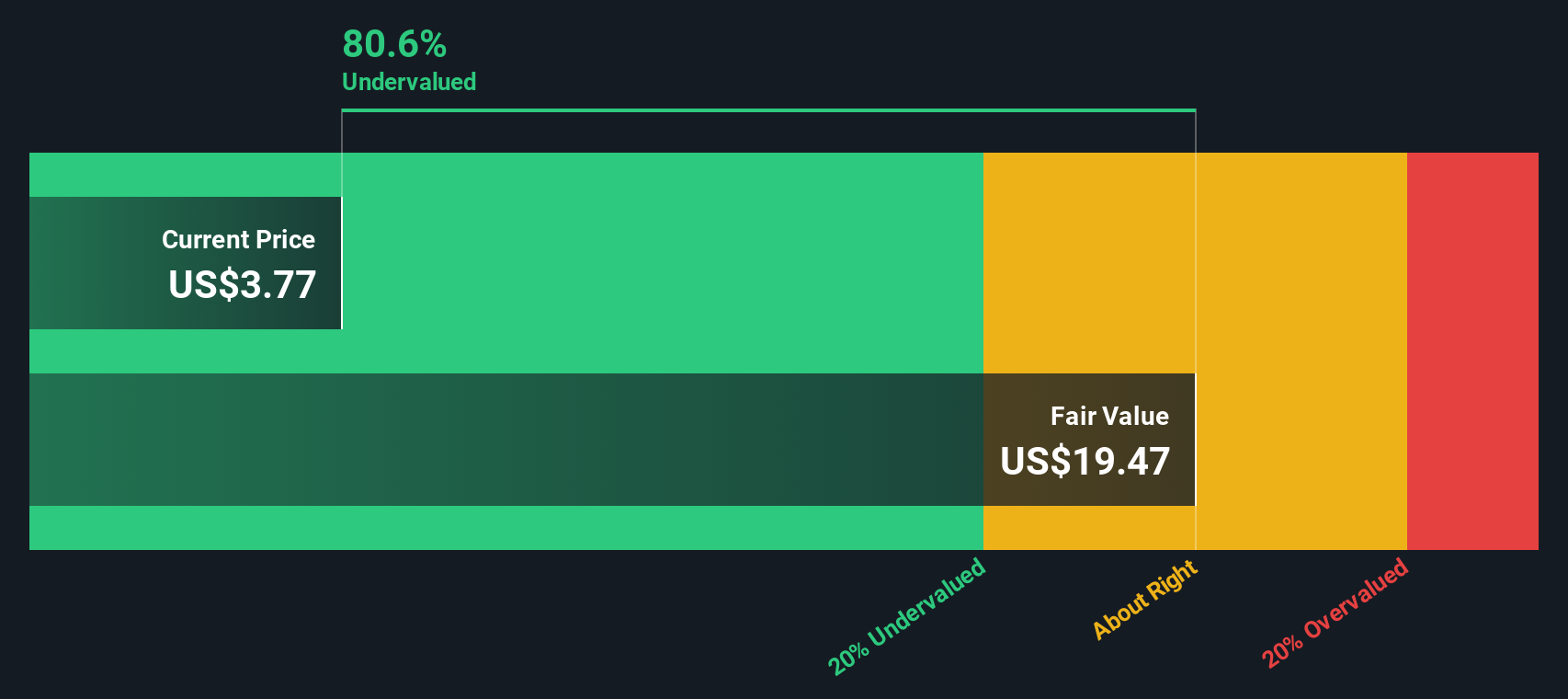

Most Popular Narrative: 45.5% Undervalued

The most followed narrative puts Nuvation Bio's fair value at $10.25 compared with the last close of $5.59, indicating a wide valuation gap to consider.

Advancement of safusidenib into a pivotal Phase III high grade IDH1 mutant glioma maintenance study, targeting a population underserved by existing therapies, could position the company to tap into a durable brain tumor market and add a second meaningful revenue pillar that has the potential to scale earnings beyond IBTROZI.

Want to see what is driving that kind of upside gap? The narrative emphasizes sharp revenue growth, a shift toward profitability and a future earnings multiple that is anything but ordinary.

Result: Fair Value of $10.25 (UNDERVALUED)

However, this upside story can unravel if IBTROZI faces tougher competition than expected or if safusidenib timelines slip, which would keep Nuvation Bio reliant on a single key asset.

Another way to look at Nuvation Bio’s value

The first narrative leans heavily on future earnings to call Nuvation Bio undervalued at $10.25 per share. Our DCF model presents an even more aggressive picture, with a future cash flow value of $42.41, which is very far above the current $5.59 share price.

The gap between those two fair values suggests that small changes in assumptions about revenue growth, profitability or timing can significantly affect the outcome. That kind of spread can look appealing, but it also raises a simple question for you: which set of assumptions do you trust more?

Build Your Own Nuvation Bio Narrative

If you see the story differently, or simply prefer to weigh the numbers yourself, you can shape a custom view in just a few minutes with Do it your way.

A great starting point for your Nuvation Bio research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If you only focus on one company, you could miss other opportunities waiting in plain sight, so take a few minutes to scan fresh ideas before markets move.

- Spot potential bargains by checking out these 872 undervalued stocks based on cash flows that the market may be pricing conservatively based on their cash flows.

- Explore companies involved in artificial intelligence by reviewing these 24 AI penny stocks that are building products and services around AI.

- Target income-focused opportunities by scanning these 13 dividend stocks with yields > 3% that currently offer yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.