Assessing Oceaneering International (OII) Valuation After Strong Recent Gains And A Mixed Short Term Pullback

Oceaneering International, Inc. OII | 0.00 |

Recent performance snapshot and why the stock is on investors’ radar

Oceaneering International (OII) has drawn attention after a mixed stretch in its share performance, with a 1 day return of a 1.3% decline and a 7 day move of a 2.6% decline as investors reassess recent gains.

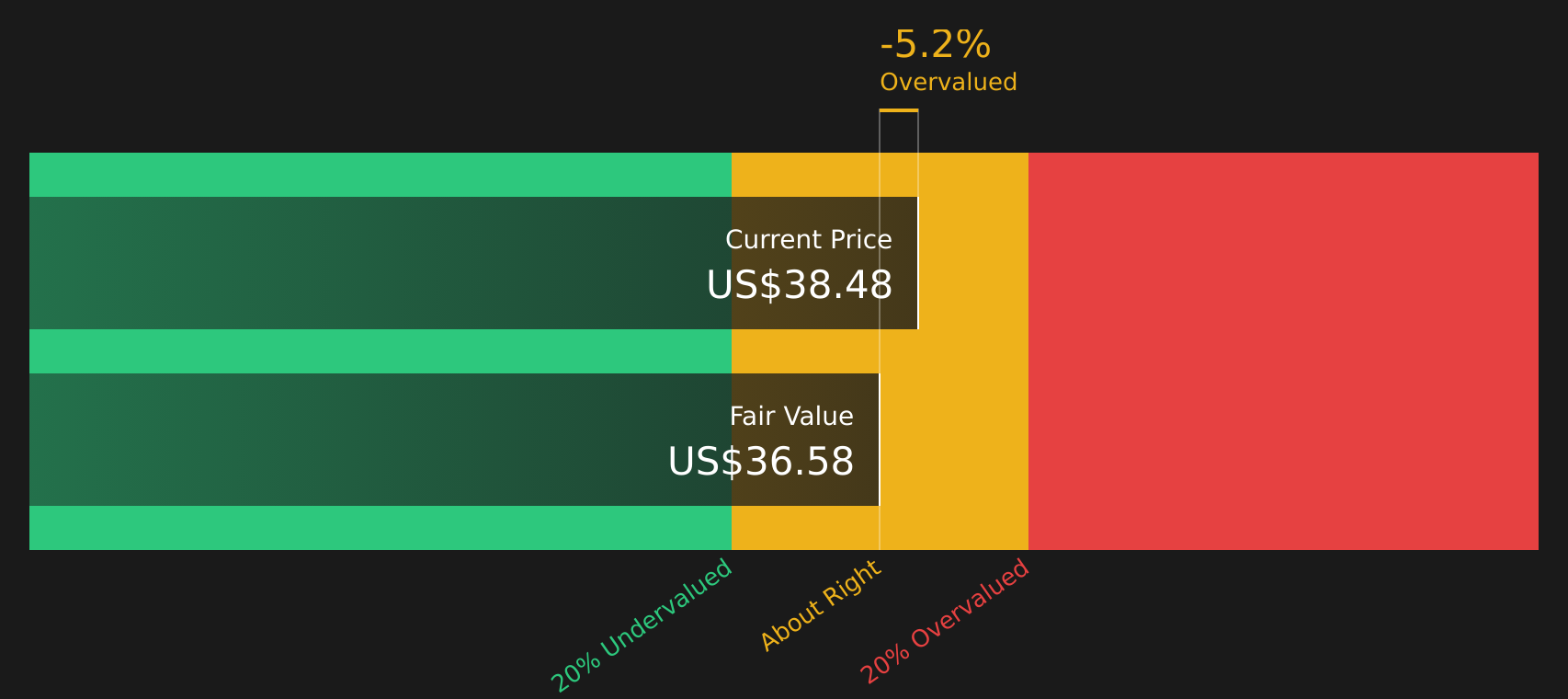

While the recent pullback, including a 2.4% 30 day share price return decline from the latest close of $36.58, hints at cooling short term momentum, the 47.2% year to date share price return and 92.7% 1 year total shareholder return point to a stock that has already seen a strong rerating as investors reassess its growth profile and risk outlook.

If robotics and automation in subsea and industrial settings interest you, it can be useful to widen the search using a screener focused on 32 robotics and automation stocks

With the stock trading slightly above the average analyst price target and only a small modelled intrinsic discount, the key question is whether Oceaneering International is still mispriced or if the market is already factoring in future growth.

Most Popular Narrative: 16.1% Overvalued

The most followed narrative sees fair value for Oceaneering International at $31.50, which sits below the last close at $36.58 and frames the stock as pricing in a rich future.

The ongoing global energy transition and intensifying decarbonization efforts continue to limit new offshore oil and gas developments. This threatens Oceaneering's long term project backlog and could ultimately reduce future revenue growth as the addressable market gradually contracts. There is increasing investor and regulatory pressure to reallocate capital away from traditional oilfield service providers. This trend is likely to hinder capital flows to Oceaneering's core business lines, potentially compressing growth prospects, restraining order activity, and constraining revenue and profit expansion.

Want to see what justifies paying above that $31.50 fair value marker? The narrative leans heavily on shifting margins, slower revenue expansion and a very punchy future earnings multiple. The exact mix of those assumptions might surprise you.

Result: Fair Value of $31.50 (OVERVALUED)

However, there are still a few watch points, including how cyclical offshore spending and rising competition in subsea robotics could pressure margins and test that rich P/E assumption.

Another View: Fair Value Almost Matches The Share Price

The narrative built around analyst targets paints Oceaneering International as 16.1% overvalued at $36.58 versus a $31.50 fair value. Yet our DCF model suggests a very different picture, with the stock trading just 0.08% below its estimated future cash flow value of $36.61. That leaves a simple question: is the real story about earnings multiples or cash generation over time?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Oceaneering International for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment split between rich valuation concerns and solid cash flow support, it makes sense to look at the data yourself and decide quickly where you stand. To weigh both sides using the same set of numbers, take a closer look at the 2 key rewards and 2 important warning signs

Looking for more investment ideas?

Do not stop with a single stock. Use focused screeners to quickly spot other opportunities that fit the way you like to invest.

- Target higher income potential by scanning companies in the 12 dividend fortresses that might suit a yield focused portfolio.

- Hunt for quality at a reasonable price by checking companies highlighted in the screener containing 23 high quality undiscovered gems before others catch on.

- Prioritize staying power by reviewing companies in the 72 resilient stocks with low risk scores that score well on resilience and downside protection.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.