Assessing Omnicom Group (OMC) Valuation After US$2.14b Shelf Registration For Common Stock Offering

Omnicom Group Inc OMC | 74.81 | -0.53% |

Omnicom Group (OMC) has drawn fresh attention after filing a shelf registration for up to US$2.14 billion of common stock, related to an employee stock ownership plan offering of 27,390,000 shares.

At a share price of US$70.75, Omnicom Group has recently seen pressure, with a 7 day share price return of 7.54% and a 30 day share price return of 10.53%, while the 1 year total shareholder return of 11.11% and 3 year total shareholder return of 15.95% contrast with a 5 year total shareholder return of 27.21%. This suggests momentum has cooled compared to earlier years as investors weigh the ESOP related issuance and broader expectations for the business.

If this ESOP related move has you thinking about where else capital might find opportunities, it could be a good time to scan a curated list of 22 top founder-led companies.

With Omnicom trading around US$70.75 on roughly 7.2x forward P/E and at a discount to some analyst estimates and intrinsic value models, is this an overlooked entry point, or is the market already pricing in future growth?

Most Popular Narrative: 30% Undervalued

With Omnicom Group last closing at $70.75 against a narrative fair value of about $101.10, the current gap centers on how its data and AI push could shape future earnings power.

The pending acquisition and integration of Interpublic is set to create the industry's largest, most data rich global marketing services company, unlocking significant cross selling opportunities, cost synergies, and expanded capabilities across digital, analytics, and high growth verticals. This is likely to drive both top line revenue growth and margin expansion post closing.

Want to see what sits underneath that confidence in higher earnings and a higher future multiple? The narrative leans heavily on tighter margins, steadier revenue growth and a different pricing of those profits compared to today. The full story shows how those moving parts line up to support that fair value.

Result: Fair Value of $101.10 (UNDERVALUED)

However, that story can change quickly if clients ramp up in house capabilities, or if integration issues around Interpublic and data privacy rules hit revenue and margins.

Another Angle On Valuation

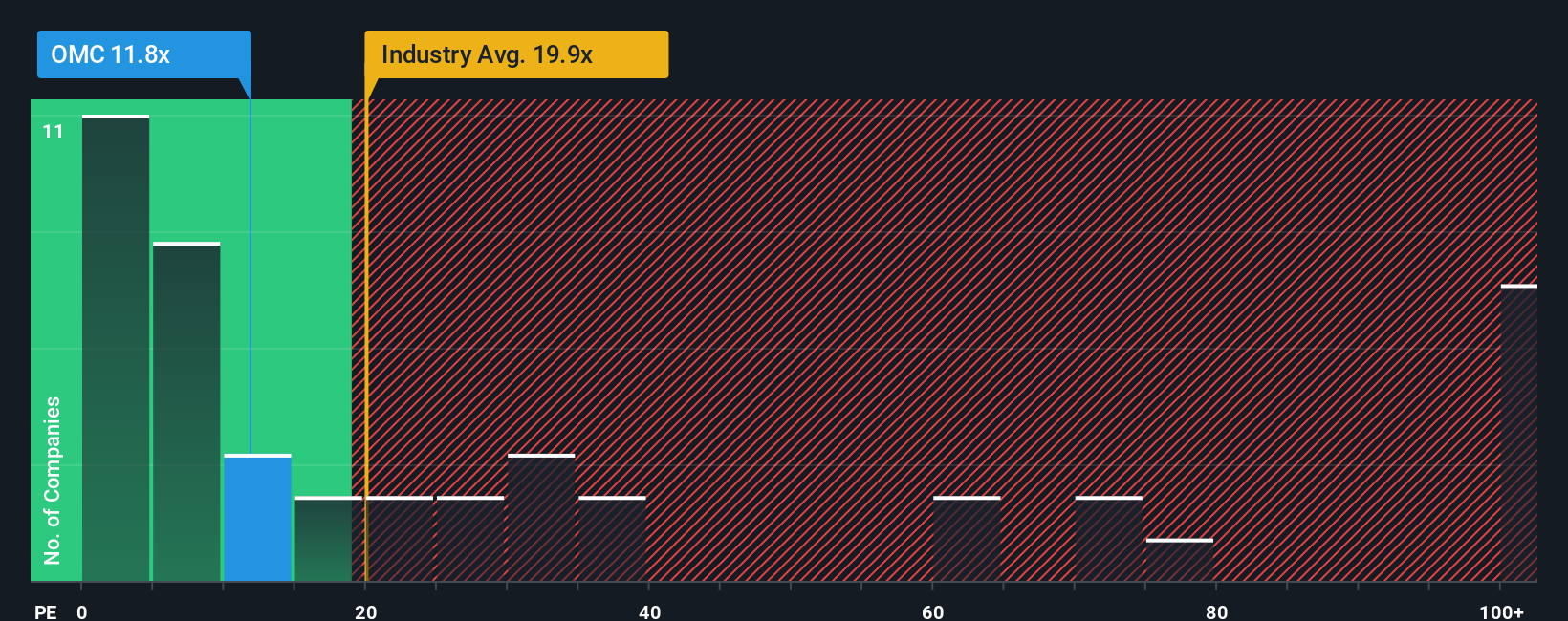

On earnings, things look a bit more mixed. Omnicom trades on a P/E of 16.7x, which is higher than the US Media industry at 15.1x, yet below a fair ratio of 23.6x and far under a peer average of 40.2x. Is that a valuation cushion, or a sign the market is already paying up?

Build Your Own Omnicom Group Narrative

If you look at the numbers and come to a different conclusion, or simply prefer to test your own view against the data, you can sketch out a customised thesis in just a few minutes, starting with Do it your way.

A great starting point for your Omnicom Group research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Omnicom has piqued your interest, do not stop here. You might miss other opportunities that fit your goals and risk comfort better.

- Target reliable cash generators by scanning our list of screener containing 24 high quality undiscovered gems that pair solid fundamentals with under the radar potential.

- Prioritise resilience by reviewing the 82 resilient stocks with low risk scores that score well on stability and downside protection.

- Focus on value and quality together through the solid balance sheet and fundamentals stocks screener (45 results) that highlight companies with stronger financial footing.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.