Assessing On Holding (NYSE:ONON) Valuation After CFO Appointment And Upgraded Growth Outlook

On Holding AG Class A ONON | 33.03 | -5.00% |

New CFO appointment puts leadership in focus

On Holding (NYSE:ONON) is back in the spotlight after naming seasoned finance executive Frank Sluis as its next Chief Financial Officer, a leadership shift that has drawn fresh attention from investors.

Sluis is set to join on May 1, 2026, succeeding CEO Martin Hoffmann, who has been handling both the chief executive and finance roles. Hoffmann plans to oversee the finance team until the transition is complete to support continuity.

At a share price of US$43.47, On Holding has recently seen a 10.67% one-month share price decline and a 7.41% year-to-date share price decline, even though its three-year total shareholder return is about 2x.

If this CFO appointment has you thinking about where leadership and growth stories meet, it could be a moment to broaden your watchlist with 22 top founder-led companies.

With revenue of US$2.88b, net income of US$224.2m and a share price that has slipped in recent months, is On now trading below what its growth story suggests, or is the market already pricing in the road ahead?

Most Popular Narrative: 30.4% Undervalued

With On Holding's fair value narrative sitting at about $62.48 against a last close of $43.47, the spread between story and market is wide enough to pay attention to.

The acceleration in DTC (Direct-to-Consumer) and e-commerce channels, with DTC reaching new highs (41.1% of sales in Q2 and up 54% YoY), gives On more control over brand, pricing, and customer data while increasing gross and EBITDA margins. This is an operational catalyst that is likely to further expand profitability as DTC continues its mix shift.

Curious what kind of revenue path, margin lift, and future earnings multiple are needed to support that fair value gap? The narrative bakes in brisk top line growth, meaningfully higher profitability, and a valuation framework that assumes investors will still pay up for that profile. The details of those assumptions are where the story really gets interesting.

Result: Fair Value of $62.48 (UNDERVALUED)

However, that fair value gap could narrow quickly if premium pricing starts to affect consumer demand or if heavier DTC spending continues to pressure EBIT margins.

Another View: High P/E Puts Pressure On The Story

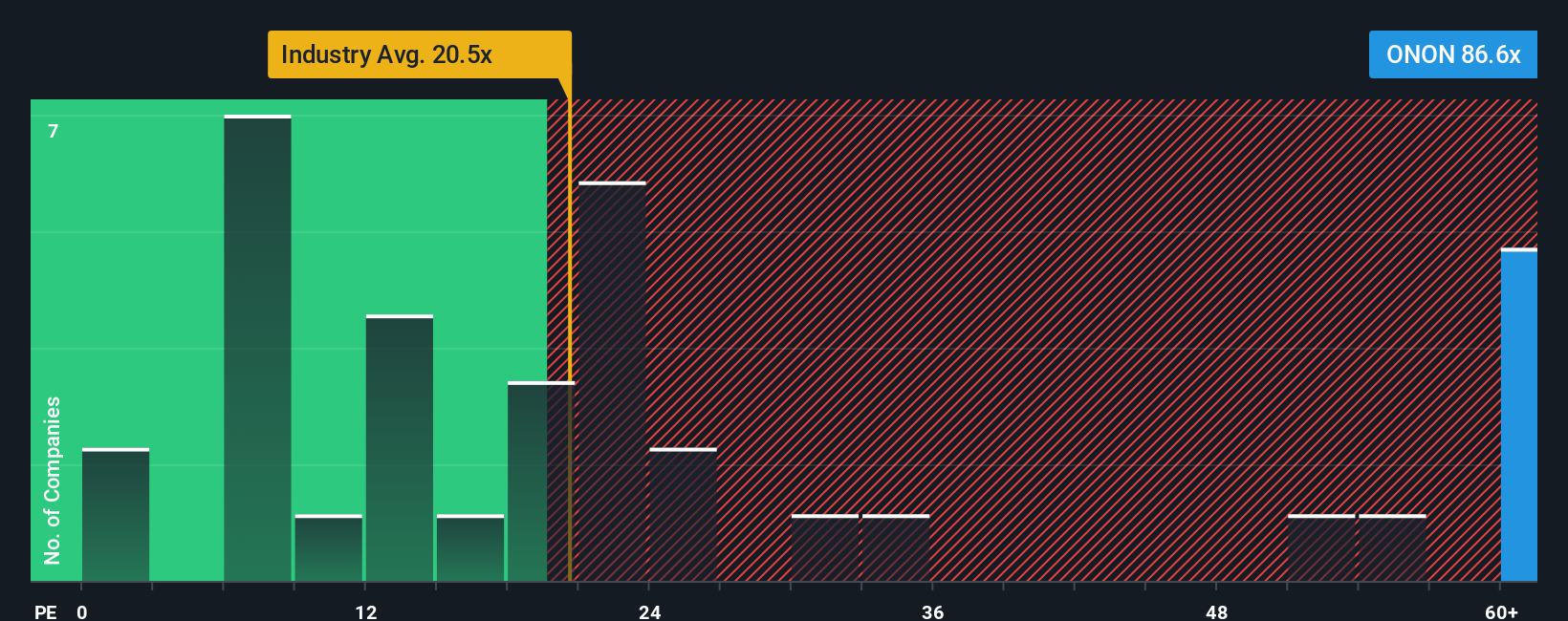

That US$62.48 fair value narrative treats On as undervalued, but the current P/E of 50.1x tells a tougher story. It sits well above the US Luxury industry at 20.9x and the fair ratio of 31.1x, so a lot of future success already seems baked into the price. If growth or margins soften, how much room is there for error?

Build Your Own On Holding Narrative

If parts of this story do not quite fit your view, or you would rather test the assumptions yourself, you can build a custom thesis in just a few minutes, starting with Do it your way

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding On Holding.

Looking for more investment ideas?

If On is already on your radar, do not stop there. Use the screener to quickly surface fresh ideas that actually fit what you want in a portfolio.

- Target potential mispricings by checking out companies our screen flags as 53 high quality undervalued stocks that may warrant a closer look.

- Prioritize resilience and sleep a little easier by reviewing 86 resilient stocks with low risk scores that score well on our risk checks.

- Get ahead of the crowd by scanning the screener containing 24 high quality undiscovered gems that our filters highlight but many investors might still be overlooking.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.