Assessing Ondas (ONDS) Valuation After New Defense Contract And Rotron Aero Acquisition

Ondas Holdings ONDS | 10.03 10.18 | +6.70% +1.50% Pre |

Ondas (ONDS) is back on investor radars after signing a new defense contract in the Asia Pacific region and agreeing to acquire UK based Rotron Aero, a specialist in advanced autonomous aerial systems.

At a share price of US$9.69, Ondas has seen a sharp 1 day share price return of 14.27% and a 90 day share price return of 64.80%. However, the 30 day share price return of 29.22% and year to date share price return of 12.07% show that momentum has recently cooled. Even so, the 1 year total shareholder return of 407.33% and 3 year total shareholder return of about 4x indicate that investors who stayed in over the longer term have experienced very strong gains.

If defense focused drone news has caught your attention, it could be a good time to widen your radar with our screener of 56 profitable AI stocks that aren't just burning cash as potential next ideas.

With Ondas trading at US$9.69 against an analyst price target of US$18.38 and an indicated intrinsic value gap of around 72%, the key question is whether this discount signals a buying opportunity or if the market is already pricing in future growth.

Most Popular Narrative: 47.3% Undervalued

Ondas' widely followed fair value estimate of US$18.38 sits well above the last close at US$9.69, which puts a lot of focus on what needs to go right to bridge that gap.

The analysts have a consensus price target of $2.5 for Ondas Holdings based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $3.0, and the most bearish reporting a price target of just $2.0.

Curious what justifies a fair value nearly double today's share price? The leading narrative leans on expectations for revenue expansion, margin improvement and a rich future earnings multiple. Want to see how those ingredients are combined into that target?

Result: Fair Value of $18.38 (UNDERVALUED)

However, you also need to weigh execution risks, including high operating expenses, reliance on debt and potential dilution from capital raises that could pressure future returns.

Another Angle on the Valuation

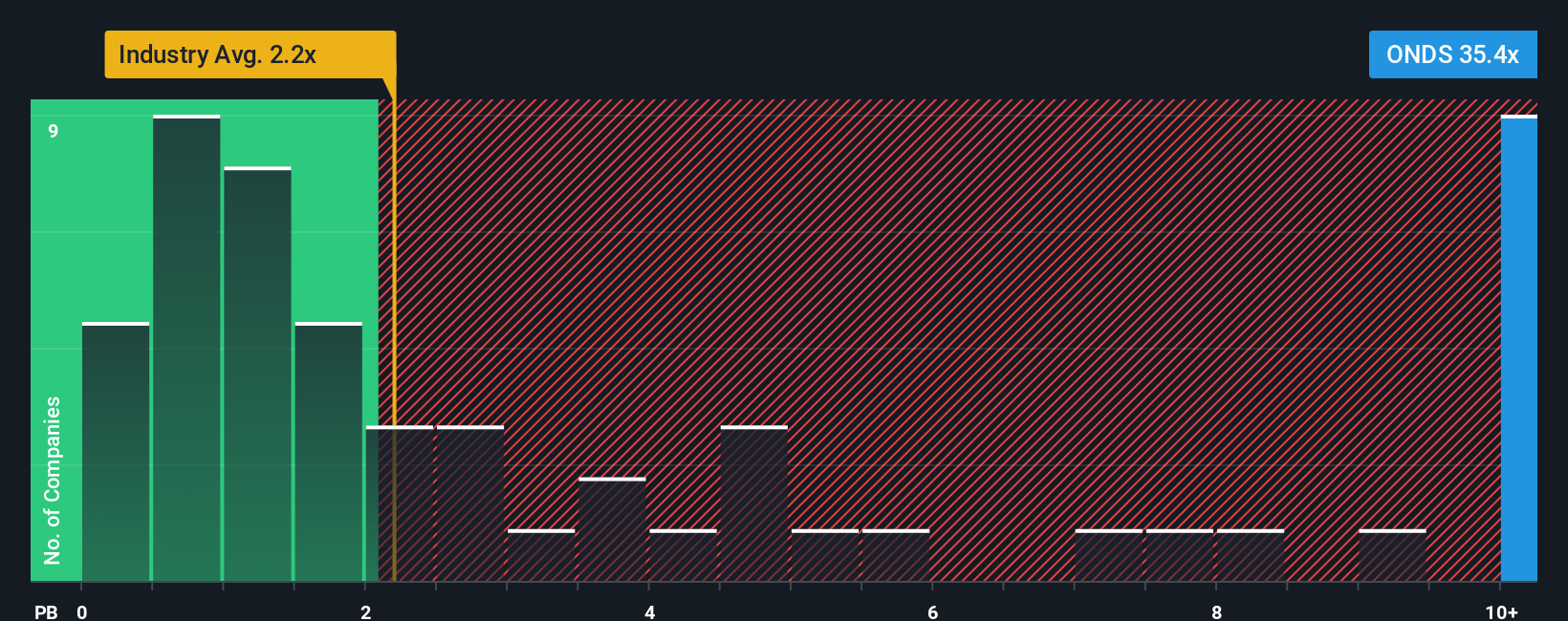

So far the conversation has leaned on fair value estimates and future earnings assumptions that flag Ondas as undervalued. If you look at a simpler yardstick like P/B instead, the story gets trickier. Ondas trades at a P/B of 8.5x, compared with about 2x for the wider US Communications industry and 4.5x for peers, while it remains unprofitable and carries funding and dilution risks. That kind of premium can reward investors if the bullish narrative plays out, but it can also unwind quickly if expectations reset. It is therefore important to be clear about which side of that trade you are relying on.

Build Your Own Ondas Narrative

If you are not fully sold on this view or prefer to lean on your own work, you can test the numbers yourself and build a custom thesis in just a few minutes, Do it your way.

A great starting point for your Ondas research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

Ready for more investment ideas?

If Ondas has sparked your interest, do not stop here. Use the Simply Wall St Screener to quickly surface other stocks that might fit your style and goals.

- Target income potential by scanning companies with 14 dividend fortresses that aim to combine higher yields with resilience.

- Hunt for value by reviewing screener containing 24 high quality undiscovered gems that could still be flying under most investors' radars.

- Prioritise resilience by focusing on 83 resilient stocks with low risk scores to see which businesses score well on our risk checks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.