Assessing Ondas (ONDS) Valuation After Raised 2026 Guidance And Strong Q4 2025 Update

Ondas Holdings ONDS | 0.00 |

Ondas (ONDS) is back in focus after its investor day, where management raised 2026 revenue guidance to a range of US$170 million to US$180 million and reported preliminary Q4 2025 sales that exceeded its earlier targets.

Those investor day upgrades landed after an intense run, with Ondas posting a 30 day share price return of 35.38% and a 90 day share price return of 77.76%, while its 1 year total shareholder return is very large. The recent 7 day pullback and 1 day decline suggest some momentum has cooled as investors digest the capital raise and faster growth ambitions.

If you are following Ondas because of its drone and wireless story, this can be a good moment to widen your radar and check out other high growth tech and AI stocks that are catching attention.

With the share price up sharply, revenue guidance lifted to US$170 million to US$180 million, and analysts setting higher targets, the key question now is simple: is Ondas still mispriced or is future growth already in the stock?

Price to Book of 10.9x: Is it justified?

Ondas trades on a P/B of 10.9x, versus peer levels around 4.1x, so the market is pricing the shares well above book based comparisons.

The P/B ratio compares the share price with the company’s net assets on the balance sheet. It is often used for asset light, early stage or loss making businesses where earnings based multiples are less useful. In Ondas' case, this high P/B suggests investors are attaching considerable value to the company’s wireless and drone platforms, rather than its current equity base or profit profile.

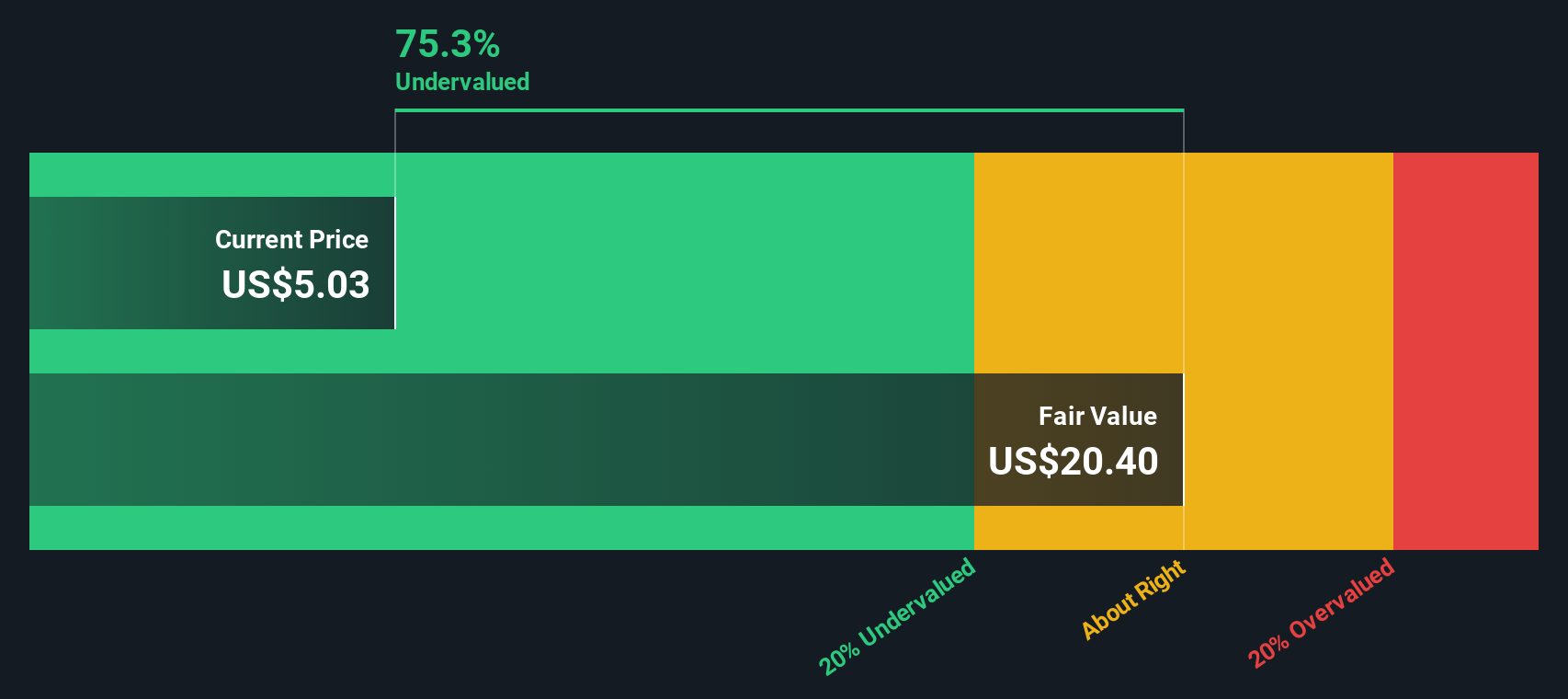

Against both its direct peers at 4.1x and the wider US Communications industry at 2.4x, Ondas' 10.9x P/B stands out as materially richer. This points to the market paying a substantial premium for its growth potential and product set. At the same time, Simply Wall St's DCF work indicates the shares are trading at a 62.4% discount to its estimate of future cash flow value of US$33.35 per share, so there is a clear tension between what the balance sheet multiple implies and what the cash flow model suggests.

Result: Price-to-book of 10.9x (OVERVALUED)

Alongside that P/B discussion, the SWS DCF model estimates a fair value of US$33.35 per share, compared with the last close of US$12.55. This implies the shares trade well below that cash flow based estimate. The DCF model projects Ondas' future cash flows and discounts them back to today using a required rate of return, which is a common way to assess what those future cash flows could be worth in present value terms.

For a company like Ondas that is currently loss making but has revenue forecasts pointing to rapid growth, a DCF framework can be helpful because it focuses on long run cash generation rather than short term earnings. It also helps set a reference point against current market expectations, which, as the high P/B suggests, already build in a lot of optimism around the business model and product adoption.

Result: DCF fair value of US$33.35 (UNDERVALUED)

However, you still need to weigh execution risks in scaling revenue from US$24.75 million and the ongoing net loss of US$47.66 million against the otherwise upbeat story.

Another View: What If The DCF Is Closer To The Mark?

The high 10.9x P/B suggests Ondas is expensive versus peers, but the SWS DCF model points the other way, with an estimated value of US$33.35 per share compared to the current US$12.55 price. If that long term cash flow view proves closer to reality, is today’s pessimism overdone or is the model too optimistic?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Ondas for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 881 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Ondas Narrative

If you reach a different conclusion or simply want to test your own assumptions against the same numbers, you can build a custom view in minutes with Do it your way.

A great starting point for your Ondas research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you are serious about building a stronger portfolio, do not stop at one stock. Use focused stock lists to spot opportunities before they are crowded trades.

- Find potential value by scanning these 881 undervalued stocks based on cash flows that might be pricing in more caution than their projected cash flows imply.

- Capture growth themes early by checking out these 23 AI penny stocks that are tied to expanding demand for artificial intelligence solutions.

- Strengthen your income stream by reviewing these 13 dividend stocks with yields > 3% that already offer yields above 3% on current prices.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.