Assessing Onto Innovation (ONTO) Valuation After SPIE PRISM Award Recognition For 4Di InSpec SR

Onto Innovation ONTO | 215.53 | +1.80% |

Onto Innovation (ONTO) just picked up the 2026 SPIE PRISM Award for its 4Di InSpec SR Surface Roughness Gauge, drawing attention to its metrology tools as investors look ahead to the February 19 earnings release.

The award news lands as Onto Innovation’s share price sits at US$202.05, with a 30 day share price return of 21.81% and a 90 day share price return of 53.41%. However, the 1 year total shareholder return is slightly negative while the 5 year total shareholder return is very large. This suggests that recent momentum has picked up after a weaker patch for long term holders.

If this kind of chip equipment story is on your radar, it might be a good time to see what else is moving in high growth tech and AI stocks.

With the stock at US$202.05 after a strong 3 month run and trading only about 3% below the average analyst target, plus a very large 5 year return, is there still a mispricing here, or is future growth already baked in?

Most Popular Narrative: 18% Overvalued

Onto Innovation’s most followed narrative pegs fair value at $172 per share versus the current $202.05, which raises questions about how optimistic the recent rally has become.

The pending Semilab acquisition will immediately expand Onto's product portfolio into electrical surface metrology and materials analysis, capabilities specifically in demand as industry transitions to exotic materials and heterogeneous integration, enabling both direct revenue accretion (~$130M annualized) and gross/operating margin uplift, further increasing earnings per share by 10%+ in the first year post-deal.

Curious what kind of revenue run rate, margin profile and future P/E the narrative needs to make $172 add up on a discounted basis? The full story lays out a detailed growth path, rising profitability, and a richer earnings multiple that has to hold together for this valuation to stack up.

Result: Fair Value of $172 (OVERVALUED)

However, there are still clear swing factors here, including any delay in AI packaging or advanced node spend, as well as potential bumps integrating the Semilab acquisition.

Another View: Earnings Power Versus The Current Price

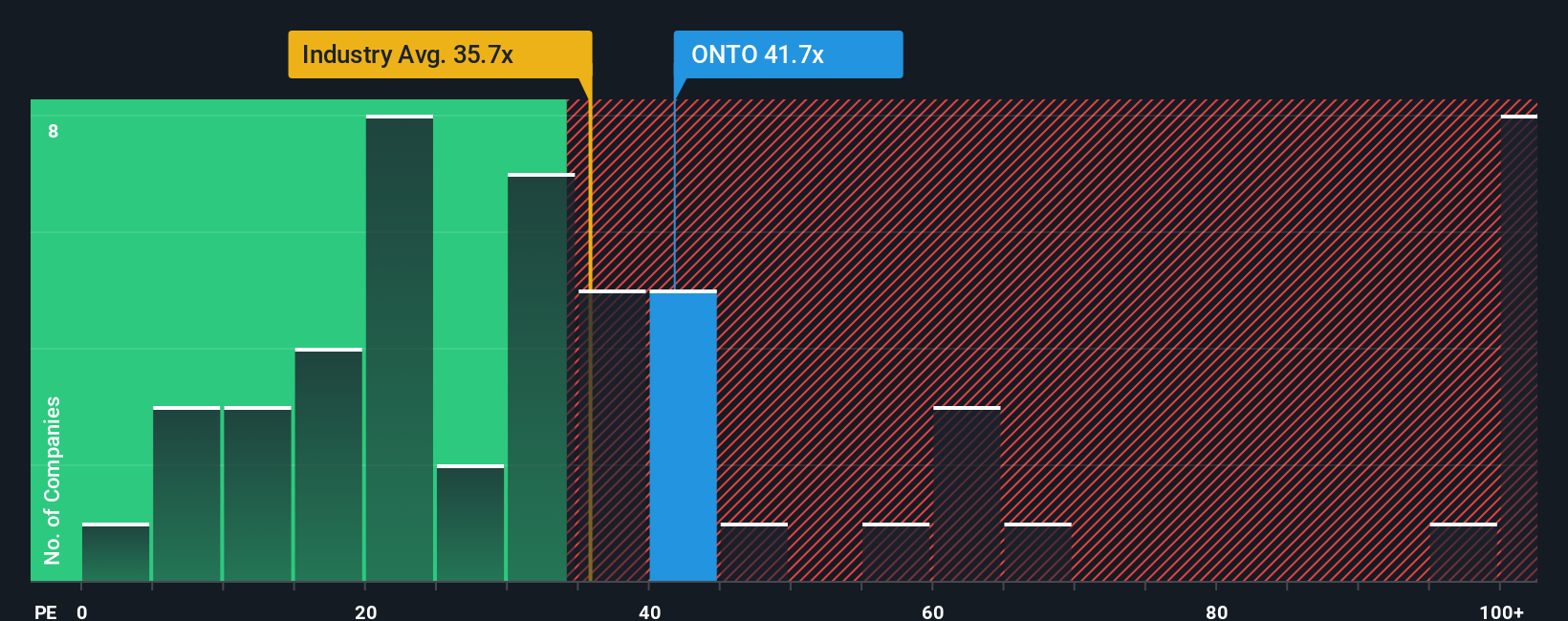

While the narrative-driven fair value sits at $172 per share and flags Onto Innovation as overvalued, the current P/E of 57.3x brings a different tension into focus. That is higher than the US Semiconductor industry at 41.9x and above the 46.5x fair ratio our work points to, so the multiple could have room to compress if expectations cool.

Build Your Own Onto Innovation Narrative

If you are not fully on board with this view or prefer to stress test the numbers yourself, you can build a custom thesis in just a few minutes using Do it your way.

A good starting point is our analysis highlighting 1 key reward investors are optimistic about regarding Onto Innovation.

Looking for more investment ideas?

If you stop with just one stock, you could miss some of the most interesting setups on the market. Take a few minutes to scan wider opportunities.

- Spot potential turnarounds by checking out these 3527 penny stocks with strong financials that already back their story with stronger financials.

- Explore AI-related opportunities by focusing on these 24 AI penny stocks that tie real businesses to current enthusiasm.

- Look for potentially mispriced cash generators using these 875 undervalued stocks based on cash flows and see which companies the screens flag as priced below their cash flow potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.