Assessing OPENLANE (OPLN) Valuation After Recent Share Price Moves

OPENLANE, Inc. OPLN | 0.00 |

OPENLANE stock snapshot after recent trading moves

OPENLANE (OPLN) has drawn fresh attention after recent trading left the shares at US$28.30, with a 1 day gain of 1.6% but declines over the past week and month.

While the 1 day share price return of 1.6% to US$28.30 comes after a softer 7 day and 30 day patch, the stronger 90 day share price return of 11.6% and 1 year total shareholder return of 37.4% suggest momentum has cooled recently but longer term holders have still seen solid gains.

If OPENLANE has you thinking about what else is moving, this could be a good moment to hunt for other ideas in our screener of 23 top founder-led companies.

With OPENLANE trading around US$28.30, a value score of 1 and an analyst price target near US$32.19, the key question is whether the stock still offers upside or if the market is already pricing in expectations for future growth.

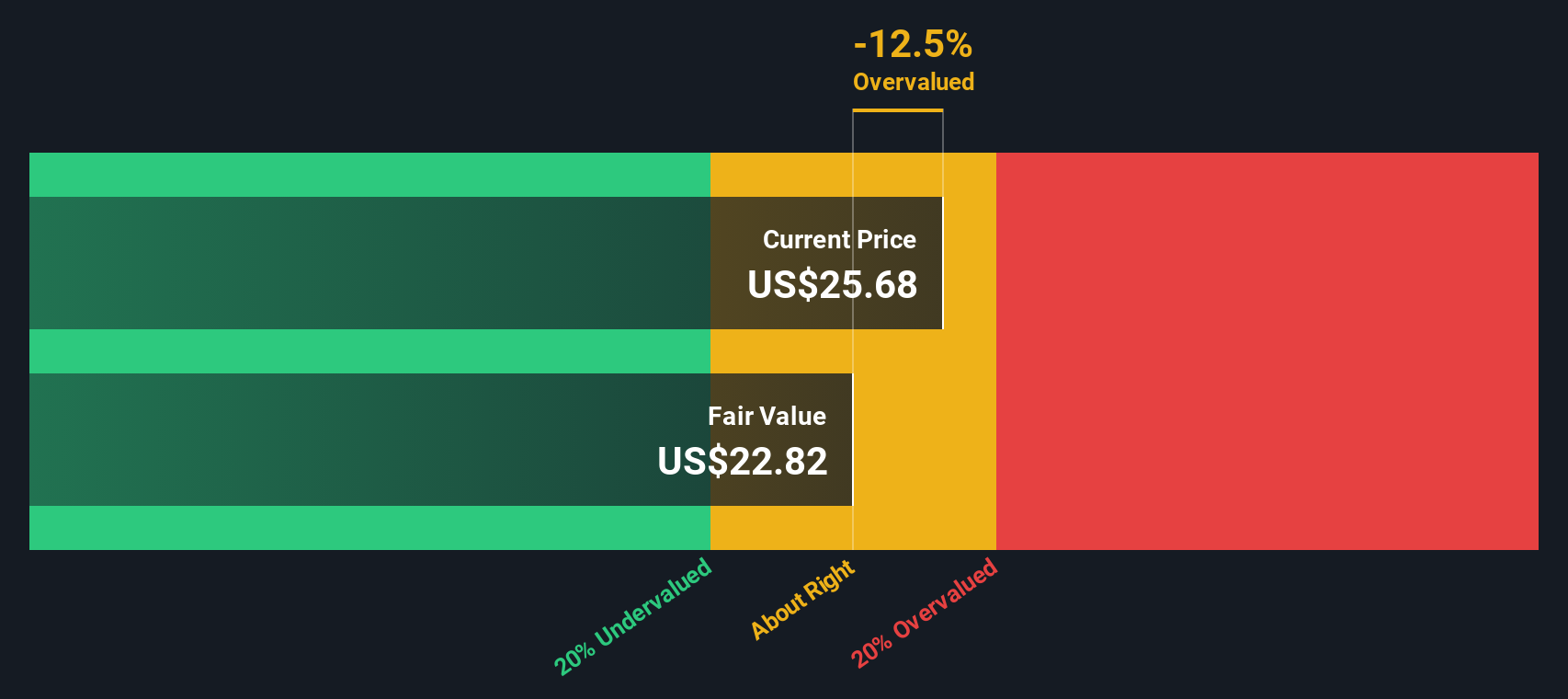

Most Popular Narrative: 12.1% Undervalued

With OPENLANE last closing at $28.30 against a narrative fair value of $32.19, the widely followed view is that the shares sit at a discount and that future execution on growth and margins is central to closing that gap.

The accelerating shift from physical to digital platforms in the wholesale vehicle auction industry, evidenced by OPENLANE's double-digit growth in dealer-to-dealer digital volumes and sustained market share gains, points to continued secular tailwinds for revenue growth as digital adoption remains in its early stages within a large total addressable market.

Ongoing investment in AI-driven products, process automation, and user experience enhancements (e.g., Absolute Sale and advanced inspection technology) is driving higher transaction values and operational efficiencies, which are already resulting in significant margin expansion and are likely to further improve net margins over time.

Curious what kind of revenue glide path and profit margin step up sit behind that fair value, and how low the implied future earnings multiple really goes, the full narrative lays out the exact assumptions and tension points that the current $28.30 price does not fully reflect.

Result: Fair Value of $32.19 (UNDERVALUED)

However, that story can quickly change if competition pressures pricing or if integration and technology projects push expenses higher and squeeze OPENLANE's net margins.

Another View On Valuation

The fair value narrative points to OPENLANE at $32.19 as undervalued, but our DCF model paints a different picture. On that measure, the shares at $28.30 sit above an estimated future cash flow value of $23.01, which suggests less room for error if expectations slip. Which story do you think reflects reality better?

Build Your Own OPENLANE Narrative

If you see the numbers differently or want to challenge these assumptions, you can test your own view in just a few minutes: Do it your way.

A great starting point for your OPENLANE research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If OPENLANE has sharpened your focus, do not stop here. This can be a good time to widen your watchlist with a few more targeted ideas.

- Target steadier compounding by reviewing companies in our 83 resilient stocks with low risk scores that aim to keep risk in check while still offering room for returns.

- Hunt for quality at a reasonable price by scanning our 54 high quality undervalued stocks, built to spotlight stocks the market may be pricing conservatively.

- Strengthen your core holdings by checking companies in the solid balance sheet and fundamentals stocks screener (45 results), where financial resilience sits at the center of the story.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.