Assessing Oracle Shares After U.S. TikTok Deal Sparks Doubts About True Value

Oracle Corporation ORCL | 145.73 | -0.94% |

Trying to figure out what to do with Oracle stock right now? You’re definitely not the only one, especially with how lively the price action has been lately. If you’ve been watching your portfolio (or considering adding a tech blue chip), Oracle has probably caught your eye with its blend of old-school enterprise credibility and new-world momentum. The big story: despite bouts of recent turbulence, including headline-grabbing developments around its high-profile involvement with the U.S. TikTok deal and cyberattack investigations, Oracle’s shares are looking unusually resilient and undeniably strong this year.

Just look at recent moves. The stock is up a whopping 22.9% over the past month and over 1.2% in the last week alone. Year-to-date gains now tip the scale at an astonishing 72.3%, with an eye-popping 398.3% return over five years. That is hardly the profile of a company people are worried about. Some of the action can be traced to shifting perceptions of the company’s risk and opportunity. TikTok deal headlines have hinted at both increased uncertainty and potential upside for Oracle’s cloud ambitions.

But momentum on its own isn’t enough if you’re focused on where the stock stands compared to its underlying worth. Based on six key valuation checks, Oracle scored just a 1, meaning it currently appears undervalued in only one area. Not the strongest value signal, but there’s more than one way to judge if a stock is worth buying.

Let’s dig into how different valuation methods stack up for Oracle and, most importantly, explore a framework for understanding company value that’s even more insightful than simply running the numbers.

Oracle scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Oracle Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model aims to estimate what a company is truly worth by projecting its future cash flows and then discounting those amounts back to their value today. In Oracle’s case, this approach uses management’s and analysts’ forecasts for Free Cash Flow (FCF) over the next several years, translating Oracle’s future ability to generate cash into an estimate of fair value right now.

Currently, Oracle reports an annual Free Cash Flow of $5.84 Billion. Analyst projections predict that by fiscal 2030, annual FCF could reach as high as $17.75 Billion. It is important to note that estimates beyond 2028 are extrapolated by Simply Wall St and are not taken directly from analyst forecasts. The process factors in some years of negative cash flow growth, notably in 2026 and 2027, and then expects strong positive swings into the next decade.

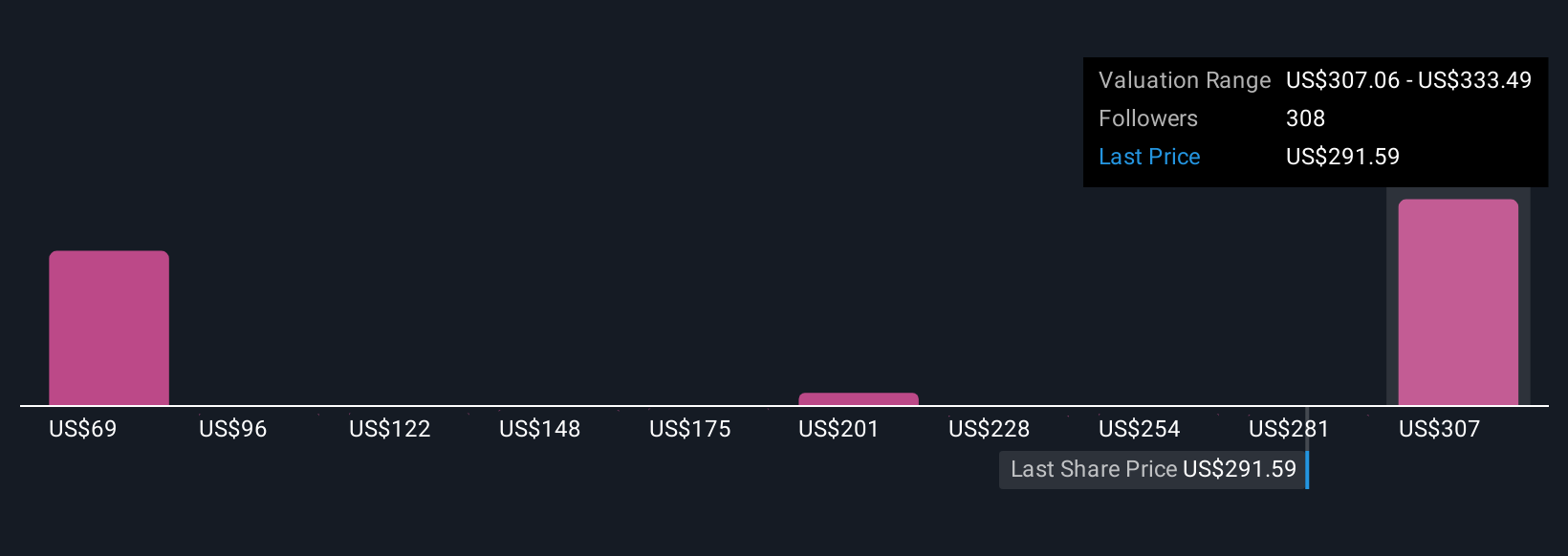

After crunching these numbers and discounting each year’s FCF appropriately, the DCF model arrives at an intrinsic fair value for Oracle shares of $69.19. Compared to the company’s current share price, the DCF valuation suggests that Oracle is trading at a 313.5% premium, indicating it is significantly overvalued on this metric.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Oracle may be overvalued by 313.5%. Find undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Oracle Price vs Earnings (PE)

The Price-to-Earnings (PE) ratio is a favorite metric when assessing profitable companies like Oracle because it lets investors quickly gauge how much the market is paying for each dollar of earnings. Generally, the higher the growth expectations or the lower the perceived risk, the higher the “normal” or “fair” PE ratio for a stock should be. Conversely, when risks are elevated or growth prospects diminish, that “fair” number drops.

Oracle’s current PE ratio sits at 65.36x, which is notably higher than the Software industry average of 35.73x and also above the peer average of 76.97x. This premium could be the market rewarding Oracle for its size, stability, or future earnings growth, but it is certainly not cheap by traditional metrics.

This is where Simply Wall St’s “Fair Ratio” comes in, a proprietary benchmark that takes into account not just Oracle’s industry and profit margins but also factors like its market cap, growth forecasts, and company-specific risks. Unlike simple industry or peer comparisons, the Fair Ratio offers a more tailored, nuanced view of valuation health for each company.

For Oracle, the Fair Ratio is calculated at 61.08x, which is very close to its current PE of 65.36x. With such a slim margin, Oracle is trading at a price that is just about right relative to its unique profile and sector dynamics.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Oracle Narrative

Earlier we mentioned there's an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is your unique, big-picture story about a company, where you lay out what you believe about Oracle's future, from revenue growth to profit margins, and how these expectations add up to a fair value all your own. Narratives connect a company’s business reality and competitive landscape to your personal financial forecast, and then to a price you’d be willing to pay. They are simple, intuitive, and available for everyone to use on Simply Wall St’s Community page, where millions of investors share and compare their views.

With Narratives, you can see how your estimates stack up by comparing your calculated Fair Value for Oracle with today’s share price, helping you decide when the stock is attractively priced or overvalued. Plus, as news or earnings come out, your Narrative updates automatically, so your decision-making stays relevant. For example, one investor’s Narrative might project Oracle becoming a dominant AI cloud leader, supporting a Fair Value as high as $333.50, while another might anticipate slower growth and assign a Fair Value closer to $212.00. Narratives empower you to invest with more conviction, clarity, and control, rooted in your own story, not just someone else’s numbers.

For Oracle, we’ll make it really easy for you with previews of two leading Oracle Narratives:

- 🐂 Oracle Bull Case

Analyst Fair Value: $333.49

Undervalued by: -14.2%

Projected Revenue Growth: 29.9%

- Explosive demand for AI workloads and Oracle’s secure enterprise AI offerings are driving rapid cloud adoption and strong revenue growth.

- Accelerated migration of existing database customers to Oracle cloud enhances revenue stability and margin expansion due to unique, differentiated platform features.

- Risks include dependency on major AI customers and aggressive CapEx. Analysts believe Oracle is fairly valued with potential upside if growth assumptions prove correct.

- 🐻 Oracle Bear Case

Narrative Fair Value: $212.00

Overvalued by: 35.0%

Projected Revenue Growth: 14.4%

- Oracle’s cloud and AI initiatives offer growth opportunities, but competition from AWS, Azure, and Google remains intense and puts pressure on margins.

- Execution risks and Oracle’s leveraged balance sheet could pose challenges scaling OCI and expanding in the AI market.

- Despite headwinds, Oracle’s focus on regulated industries and hybrid solutions supports resilience. Success relies on sustained innovation and effective risk management.

Do you think there's more to the story for Oracle? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.