Assessing Oracle’s Valuation as Contrasting Narratives Challenge the Outlook for ORCL

Oracle Corporation ORCL | 0.00 |

What Oracle’s latest figures mean for investors

Oracle (ORCL) is back in focus after recent trading put the stock around $205.81, with returns over the past month and past 3 months contrasting with longer term performance and raising fresh questions about valuation and growth durability.

Recent trading has been choppy, with the share price falling 15.9% over the past week after a strong 26.2% 3 month share price return, while the 1 year total shareholder return of 17.1% keeps longer term momentum intact.

If Oracle’s moves have you reassessing your tech exposure, it could be worth scanning other AI focused stocks using the Simply Wall St screener to uncover 49 AI infrastructure stocks.

With revenue of US$64.1b, net income of US$16.2b and analysts seeing around a 24% gap between the current price and their target, is Oracle offering a genuine entry point, or is the market already pricing in future growth?

Most Popular Narrative: 71.6% Overvalued

Compared with Oracle’s last close at $205.81, the most followed narrative pegs fair value nearer $119.97, which is a materially lower starting point for any valuation debate.

Oracle currently generates roughly US$52B in annual revenue and about US$10–11B in net income. If the company can sustain roughly 8–10% revenue growth, total revenue could reach around US$80B within the next five years.

Curious what bridges today’s price to that lower fair value line. The narrative leans heavily on revenue expansion, firm margins, and a future earnings multiple that does a lot of heavy lifting.

Result: Fair Value of $119.97 (OVERVALUED)

However, this hinges on Oracle executing in AI infrastructure while competing with AWS, Microsoft and Alphabet, and on AI demand remaining strong enough to support those assumptions.

Another view on Oracle’s value

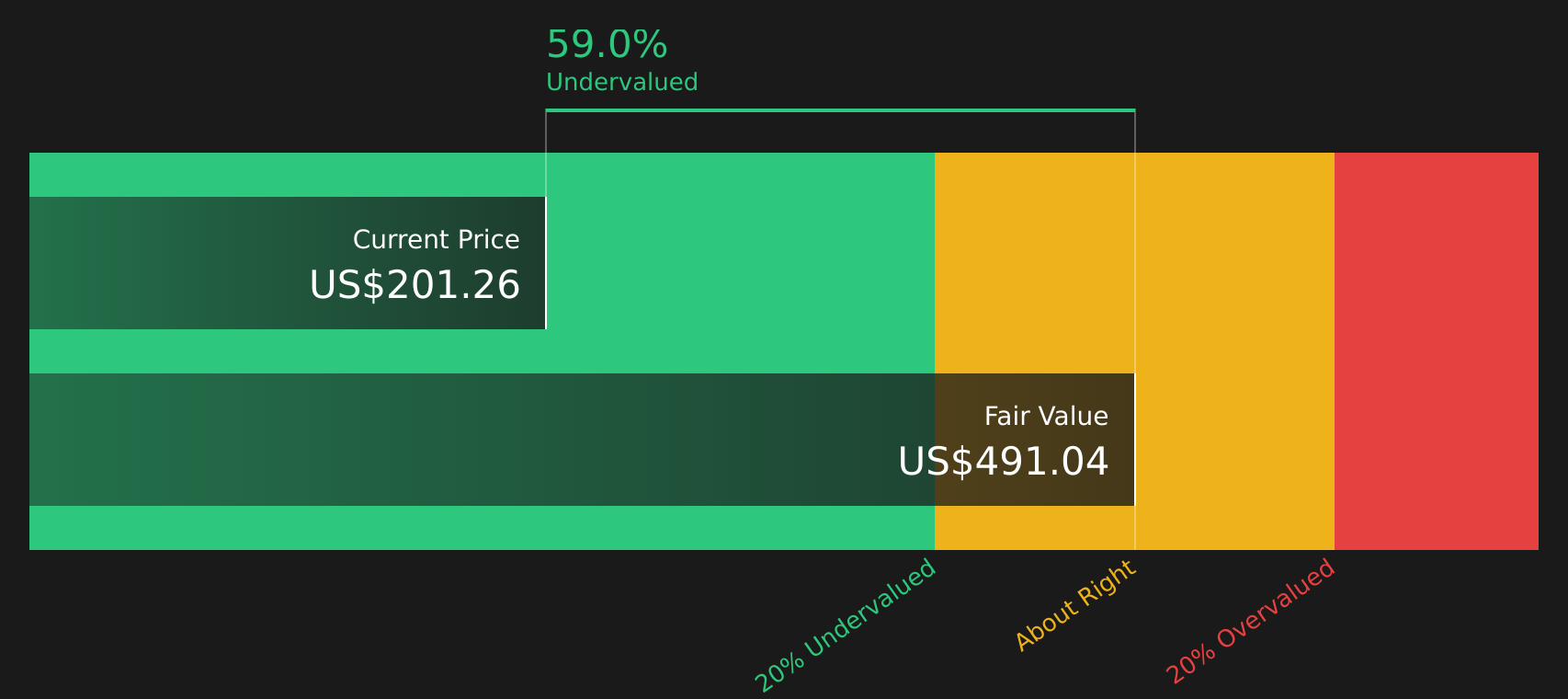

The user narrative describes Oracle as 71.6% overvalued at a fair value of $119.97, while Simply Wall St’s DCF model suggests the opposite, indicating the stock is trading 58.1% below an estimated future cash flow value of $491.07. When two methods disagree this sharply, which one do you consider more reliable, and for what reasons?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Oracle for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Mixed signals on value and execution can be frustrating, so move quickly, review the data for yourself, and weigh the 3 key rewards and 2 important warning signs.

Looking for more investment ideas?

If Oracle has sharpened your thinking, do not stop there. Broaden your watchlist with a few focused stock ideas that fit different portfolio goals.

- Hunt for potential bargains by scanning companies that look attractively valued on fundamentals with the Simply Wall St screener for 46 high quality undervalued stocks.

- Strengthen your income stream by reviewing companies that aim to combine yield with resilience through the screener of 9 dividend fortresses.

- Prioritise resilience by focusing on companies with solid finances and lower risk profiles using the screener of 63 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.