Assessing Ouster (OUST) Valuation After ARGUS Counter‑Drone Collaboration And Recent Share Price Surge

Ouster, Inc. OUST | 0.00 |

Ouster (OUST) is back on investor radars after its digital lidar was selected for ARGUS Interception’s A1-Falke net-based interceptor drones, a move that ties the company more closely to counter-drone and public safety applications.

Ouster’s recent ARGUS agreement comes on the heels of partnerships with Gecko Robotics and Fujifilm around its Rev8 digital lidar. This drumbeat of news has coincided with a 30 day share price return of 62% and a one year total shareholder return of about 2.6x, suggesting momentum has been strong even with a 1 day share price pullback of 4.3%.

If this kind of lidar and robotics activity has your attention, it could be a good moment to see what else is moving in automation and sensor technology through our 35 robotics and automation stocks.

With the stock up 62% over the past month, trading just above the average analyst price target yet still showing an estimated 9% intrinsic discount, investors have to ask whether there is meaningful upside remaining or whether the market is already pricing in future growth.

Most Popular Narrative: 6.7% Overvalued

With Ouster last closing at $42.33 versus a most followed fair value estimate of about $39.67, the current price sits modestly above that narrative view while still baking in robust growth and margin assumptions.

Ouster's focus on software attached bookings, which increased by over 60% in 2024, indicates future growth in high margin software solutions, likely resulting in improved net margins compared to hardware only sales.

There is a detailed playbook behind this valuation. It leans heavily on rapid top line expansion, margin uplift, and a future profit multiple that assumes meaningful scale. Curious which specific growth and profitability milestones need to line up to support that fair value.

Result: Fair Value of $39.67 (OVERVALUED)

However, this hinges on Ouster defending its turf against lidar competitors while managing variable gross margins that could unsettle earnings and challenge the current growth narrative.

Another View: Cash Flows Point a Different Way

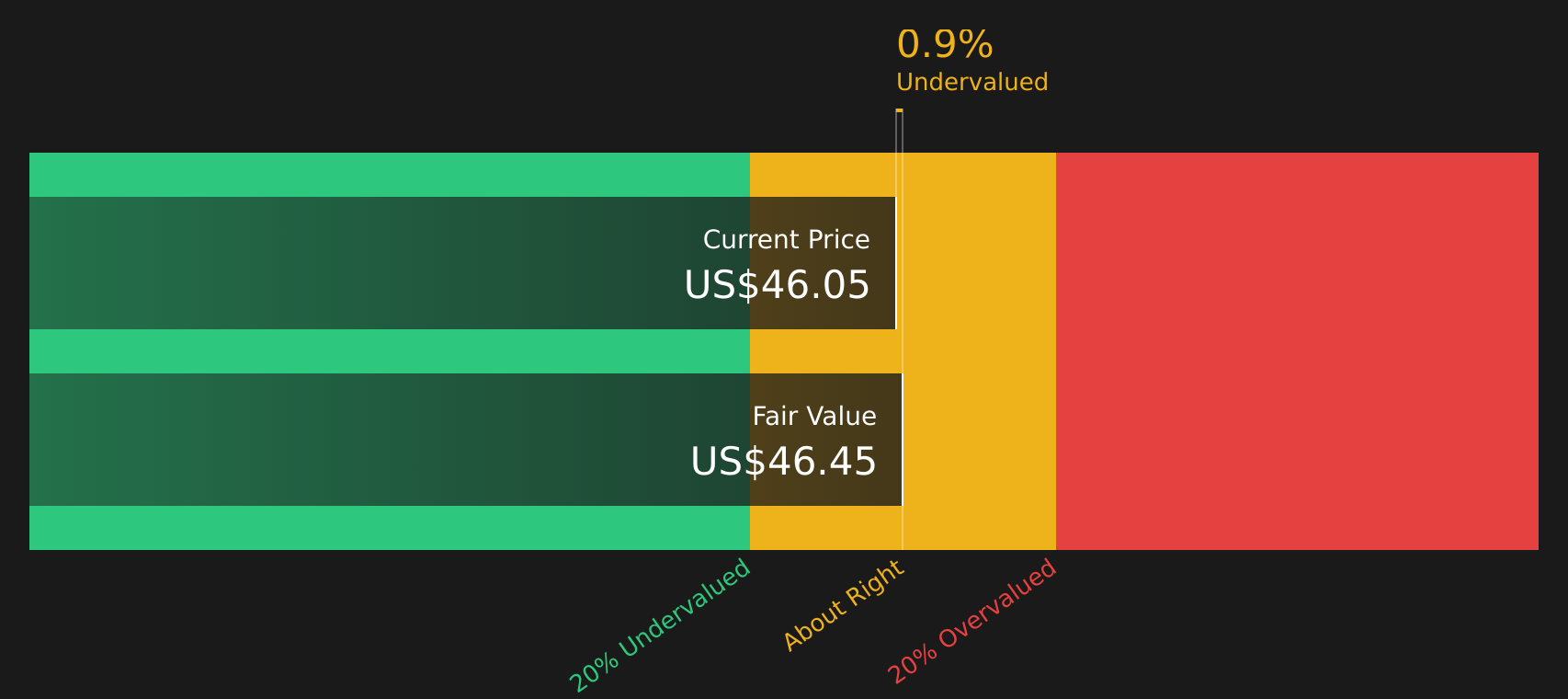

While the most followed narrative frames Ouster as about 6.7% overvalued against a $39.67 fair value, our DCF model points to a different message. On that cash flow view, the stock at $42.33 sits roughly 9.2% below a fair value estimate of about $46.62. The question, then, is which signal should carry more weight for investors.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Ouster for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Mixed signals so far. If that contrast between opportunity and concern stands out to you, now is the time to weigh the 3 key rewards and 2 important warning signs.

Looking for more investment ideas?

If Ouster has sparked your interest, do not stop here. Broaden your watchlist now so you are not chasing the crowd after the next move appears.

- Target potential value opportunities before they feel crowded by checking out 46 high quality undervalued stocks that combine solid fundamentals with attractive pricing signals.

- Strengthen the income side of your portfolio by reviewing 10 dividend fortresses that focus on higher yields with an emphasis on resilience.

- Prioritise capital preservation without sitting on the sidelines by scanning 64 resilient stocks with low risk scores built around more resilient financial and risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.