Assessing Ouster (OUST) Valuation After Strong Revenue Growth And Return To Profitability

Ouster, Inc. OUST | 24.44 | +4.36% |

Why Ouster’s latest earnings matter for investors

Ouster (OUST) reported fourth quarter revenue of US$62.18 million and net income of US$3.99 million, compared with US$30.09 million revenue and a net loss of US$23.74 million a year earlier.

Basic earnings per share from continuing operations came in at US$0.07, with diluted EPS at US$0.06, versus a basic and diluted loss of US$0.48 per share in the prior year period.

The earnings beat and the recently closed StereoLabs acquisition appear to be feeding into the story investors are watching. The latest 1-day and 7-day share price returns of 6.86% and 12.13% contrast with weaker year to date share price performance and a very large 1 year total shareholder return. However, this still leaves the 5 year total shareholder return deeply negative, suggesting momentum has improved in the short term but remains mixed over a longer horizon.

If Ouster’s move into Physical AI has caught your attention, you might also want to see which other robotics and automation names are gaining interest through our 30 robotics and automation stocks.

With the share price still down 13.35% year to date, yet carrying what brokers see as very large upside to their US$39.50 target and a high intrinsic discount flag, is Ouster on sale or is the market already baking in future growth?

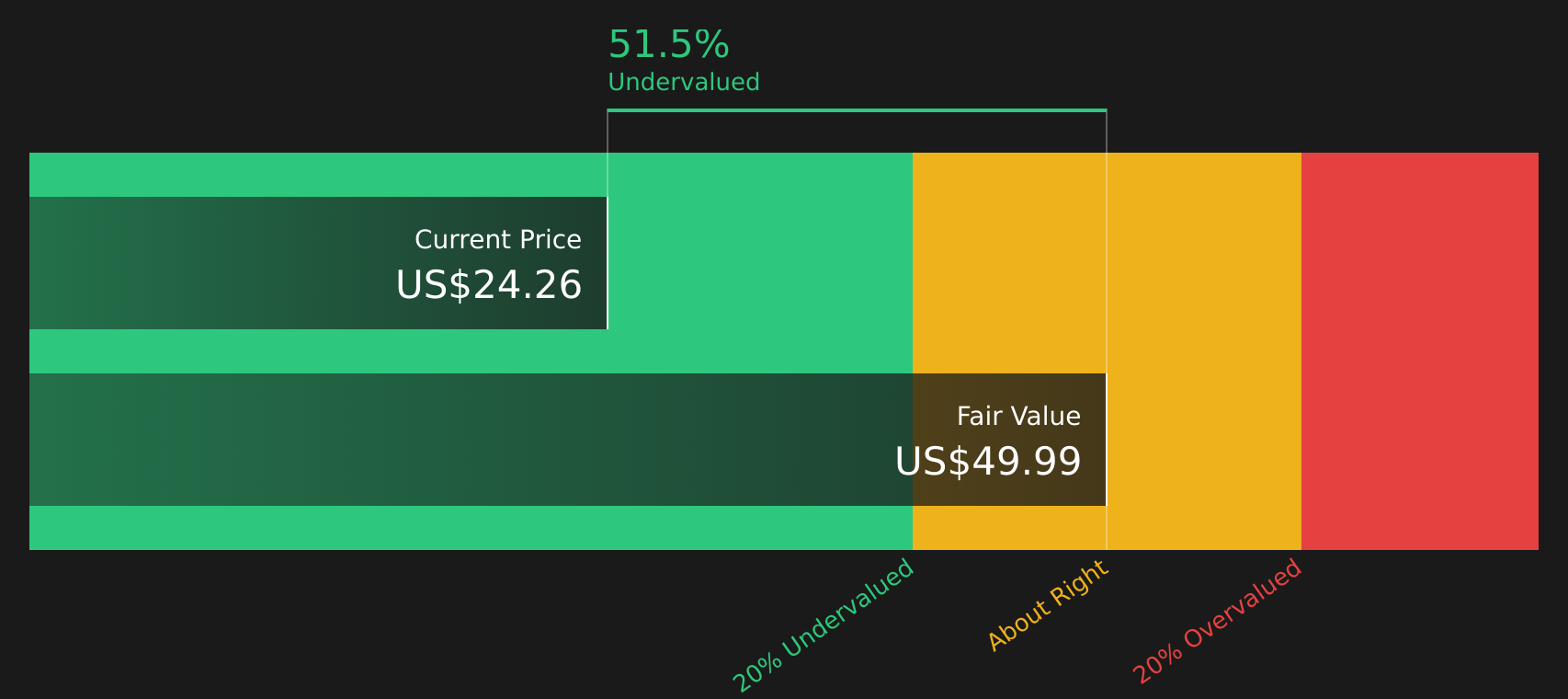

Most Popular Narrative: 48.7% Undervalued

Ouster’s most followed narrative pegs fair value at US$39.50 versus a last close of US$20.25, framing a wide gap that hinges on future execution in its core lidar and software markets.

Ouster is tapping into the massive Intelligent Transportation Systems (ITS) market with their Blue City traffic management solution, which could drive significant revenue growth as they expand deployments across the US, Europe, and Asia. This is expected to positively impact revenue.

Curious what sits behind that near 50% gap to fair value? The narrative leans heavily on rapid revenue expansion, a rising software mix, and a much richer profit profile. Want to see how those ingredients combine into a future earnings path and valuation multiple that backs a US$39.50 view?

Result: Fair Value of $39.50 (UNDERVALUED)

However, the whole thesis can wobble if lidar adoption in industrial and smart infrastructure markets is slower than expected, or if aggressive rivals pressure pricing and margins.

Another Angle on Ouster’s Valuation

The main story so far leans on a fair value of US$39.50 that points to Ouster looking undervalued. The SWS DCF model tells a similar story, with our future cash flow value at US$42.53 versus a share price of US$20.25. That gap suggests potential upside, but also raises the question of how much execution risk you are comfortable with.

Next Steps

If the mix of enthusiasm and caution here feels familiar, that is the point. You should act quickly, review the numbers, and weigh both sides through 3 key rewards and 4 important warning signs.

Looking for more investment ideas?

If Ouster has sharpened your interest, do not stop here. Put that momentum to work by scanning for other ideas that fit your style and risk comfort.

- Target reliable compounding by reviewing 13 dividend fortresses, where income focused investors can spot yield opportunities backed by solid payout records.

- Hunt for potential mispricings through 45 high quality undervalued stocks, built to surface companies that our model flags as offering value relative to their fundamentals.

- Prioritize peace of mind with 76 resilient stocks with low risk scores, highlighting businesses that score well on our internal risk metrics so you can focus your research where it counts.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.