Assessing Pebblebrook Hotel Trust (PEB) Valuation After Recent Share Price Momentum

Pebblebrook Hotel Trust PEB | 14.11 | +2.47% |

Pebblebrook Hotel Trust (PEB) has drawn fresh attention after its recent share performance, with the stock up about 6% over the past month and roughly 15% in the past 3 months.

That recent 6% 1 month share price return and 15% 3 month share price return sit within a year to date share price gain of about 10%. The 1 year total shareholder return of roughly 5% contrasts with negative total shareholder returns over 3 and 5 years, suggesting that recent momentum follows a tougher longer term stretch.

If Pebblebrook’s move has you thinking about where else capital might work, this could be a good moment to broaden your search with our list of 23 top founder-led companies.

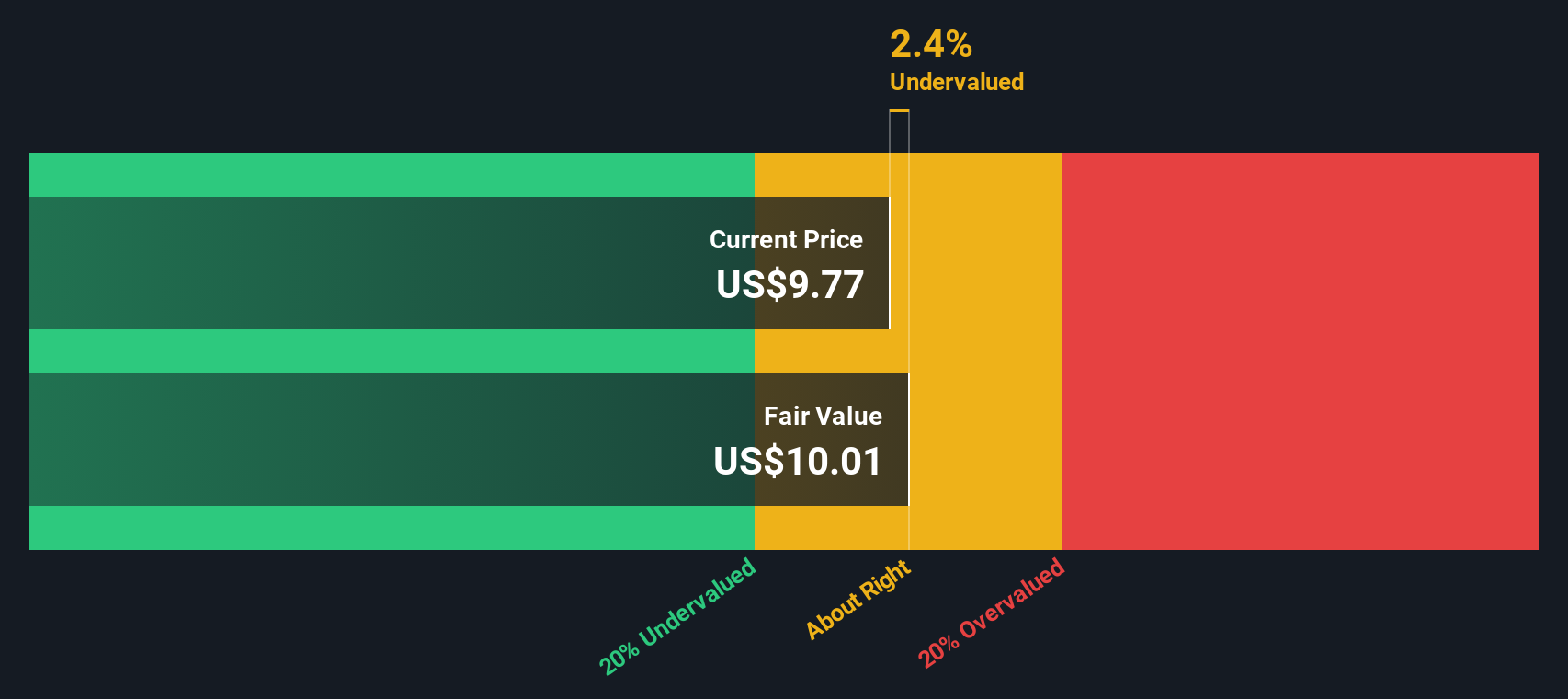

With Pebblebrook trading near its analyst price target and screening as materially discounted on some intrinsic measures despite recent gains, investors may ask whether there is still a buying opportunity here or whether the market is already pricing in future growth.

Most Popular Narrative: 1.3% Overvalued

The most followed narrative sets a fair value of about $12.58 per share, which sits slightly below Pebblebrook’s recent close at $12.75 and frames current expectations for its recovery story.

The ongoing recovery and strengthening of urban hotel demand, particularly in major gateway cities like San Francisco (where occupancy climbed from ~64% to nearly 70% year-over-year and remains well below peak levels), signals robust upside for further RevPAR and revenue growth as global travel and urbanization trends persist and major events return to cities.

Want to see what sits behind that urban demand story? The narrative leans on gradual revenue gains, margin repair, and a future earnings multiple that assumes real staying power. The key inputs are all laid out. The tension between slower growth forecasts and a higher required valuation multiple is where the story really gets interesting.

Result: Fair Value of $12.58 (OVERVALUED)

However, you still need to weigh risks such as Pebblebrook’s heavy focus on urban gateway markets and rising labor and wage pressures that could squeeze margins.

Another Angle on Value

Those narratives point to Pebblebrook as roughly 1.3% overvalued at around $12.58 per share, yet our DCF model paints a different picture, with an estimate of $18.19 per share that suggests the stock is materially undervalued. When two methods disagree this much, which one should be considered more reliable?

Build Your Own Pebblebrook Hotel Trust Narrative

If you are not fully on board with this view or prefer to lean on your own research, you can piece together a fresh Pebblebrook story in just a few minutes, starting with Do it your way.

A great starting point for your Pebblebrook Hotel Trust research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you want Pebblebrook to be just one piece of a stronger portfolio, now is a good time to hunt for other ideas that fit your style.

- Target dependable cash generators by scanning companies with strong fundamentals using our solid balance sheet and fundamentals stocks screener (44 results), so your shortlist starts from financial strength.

- Hunt for potential bargains with our 53 high quality undervalued stocks, built to surface companies that combine quality metrics with prices that may sit below intrinsic estimates.

- Lock in income-focused ideas by reviewing the 13 dividend fortresses, a curated list of higher yielding names for investors who care about consistent payouts.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.