Assessing Permian Resources (PR) Valuation After Earnings Beat And Ownership Realignment

Permian Resources Corporation Class A PR | 21.18 | +2.82% |

Board change adds context to recent performance

Permian Resources (PR) drew fresh attention after director Robert J. Anderson notified the company of his retirement from the Board, effective January 21, 2026. The announcement has prompted investors to reassess recent developments and stock performance.

At a share price of $15.74, Permian Resources has had a 7 day share price return of 6.64% and a 90 day share price return of 26.83%. Its 1 year and 5 year total shareholder returns of 13.99% and around 4.3x respectively suggest momentum has been building over time, supported recently by an earnings beat and a corporate reorganization that aligned management ownership with public investors ahead of the planned board change.

If you are looking beyond energy for your next idea, this could be a good moment to widen the search and check out fast growing stocks with high insider ownership.

With the shares at $15.74, a value score of 4, annual revenue of about $5.2b and net income of roughly $812m, the key question is simple: is Permian Resources undervalued here or is the market already pricing in future growth?

Most Popular Narrative: 12.8% Undervalued

Compared with the last close at $15.74, the most followed narrative points to a fair value of about $18.05, built on detailed revenue, margin and discount rate assumptions.

The strengthened balance sheet, abundant liquidity, and newly achieved investment-grade credit rating provide Permian Resources with financial flexibility to deploy capital opportunistically during periods of market dislocation, supporting continued buybacks, disciplined M&A, and stable or growing shareholder returns (EPS and long-term FCF/share).

Want to see what is behind that valuation uplift, beyond headline production numbers and buybacks? The narrative leans heavily on projected revenue growth, slightly higher margins, and a future earnings multiple that still sits below the sector yardstick. Curious how those moving parts combine into that fair value figure and what discount rate is doing the heavy lifting? The full breakdown joins those threads together for you.

Result: Fair Value of $18.05 (UNDERVALUED)

However, the story can change quickly if commodity prices weaken or if tighter environmental rules lift costs and limit how far those earnings forecasts can stretch.

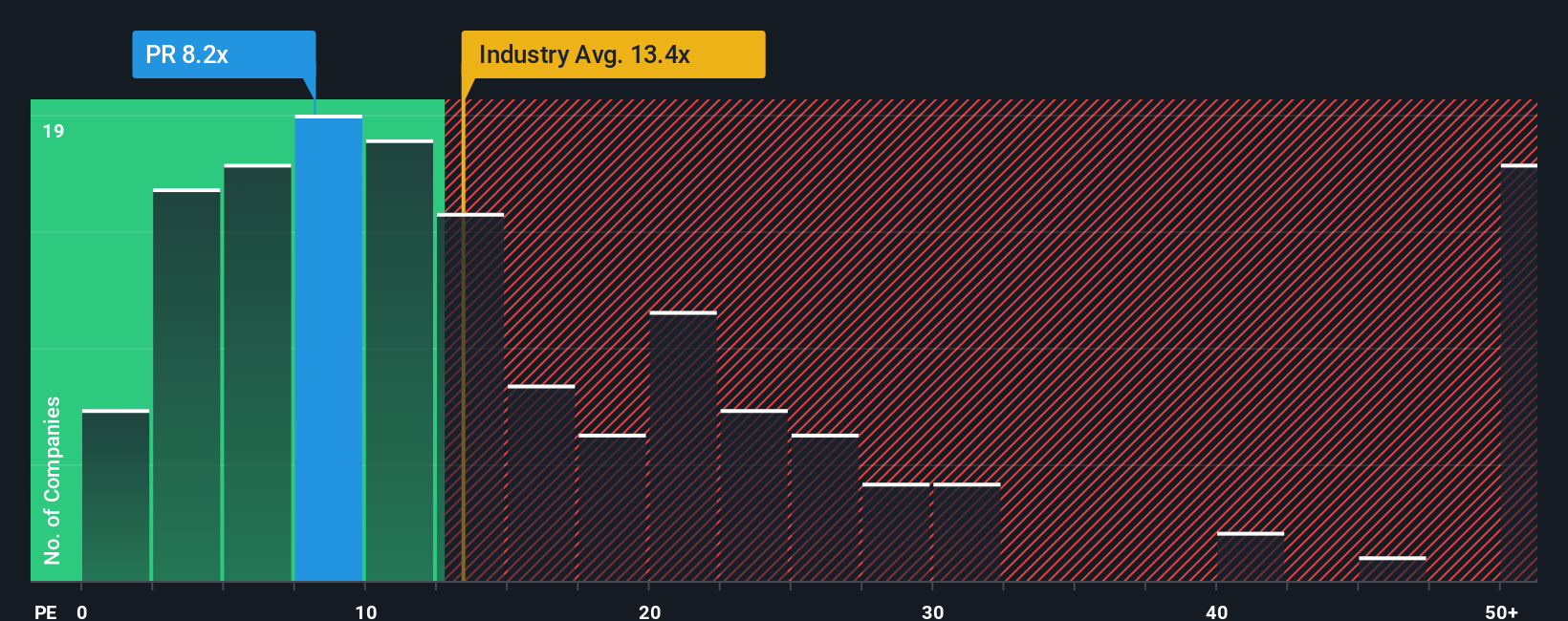

Another View: Market Multiple Sends Mixed Signals

While the most followed narrative sees Permian Resources as undervalued at $15.74 versus a fair value of about $18.05, the current P/E of 14.4x tells a more cautious story when you look at what the market is already paying for similar earnings.

The 14.4x P/E is slightly higher than the US Oil and Gas industry average of 13.7x, so the market is paying a premium to the sector. However, it still sits well below peers at 19.4x and under the 19.8x fair ratio that our models suggest the market could move toward. Does that gap point to additional upside, or does it instead reflect additional risk if sentiment cools?

Build Your Own Permian Resources Narrative

If you are not fully aligned with these viewpoints, or simply prefer to test the numbers yourself, you can build a tailored view in minutes with Do it your way.

A great starting point for your Permian Resources research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you stop with just one stock, you risk missing other opportunities entirely. You can use the Simply Wall St Screener to line up your next few ideas today.

- Spot potential value opportunities quickly by checking out these 872 undervalued stocks based on cash flows that match your preferred mix of fundamentals and price.

- Explore digital asset-related opportunities by scanning these 18 cryptocurrency and blockchain stocks tied to blockchain, payments, and broader crypto adoption.

- Build a cash flow focused watchlist with these 13 dividend stocks with yields > 3% that offer yields above 3% and consistent income potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.