Assessing Plains GP Holdings (PAGP) Valuation After Recent Share Price Strength

Plains GP Holdings LP Class A PAGP | 24.06 | +1.43% |

Why Plains GP Holdings (PAGP) is on investors’ radar

Plains GP Holdings (PAGP) has caught attention after a strong past 3 months, with the stock showing a month-long gain as well and meaningful multi year total returns that invite closer scrutiny.

At a share price of US$20.42, Plains GP Holdings has recently seen a 30 day share price return of 8.5% and a 90 day share price return of 15.6%. Its 5 year total shareholder return of 233.9% points to a much stronger long term outcome than the last year’s 3% total shareholder return, suggesting momentum has been building recently after a quieter stretch.

If PAGP’s move has you looking across energy infrastructure, it can be useful to compare against other parts of the market using tools like fast growing stocks with high insider ownership to spot fresh ideas.

With Plains GP Holdings trading near analyst price targets and sitting on very strong 3 and 5 year returns, the key question now is whether the market is fully valuing that progress or if there is still a buying opportunity pricing in future growth.

Most Popular Narrative: 2.2% Undervalued

With Plains GP Holdings last closing at $20.42 versus a narrative fair value of $20.88, the gap is small but it still raises questions about what the underlying forecasts are assuming.

The analysts have a consensus price target of $21.458 for Plains GP Holdings based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $26.0, and the most bearish reporting a price target of just $17.5.

Curious what kind of earnings jump, margin shift and future P/E level support that fair value? The narrative ties all three together in a tight set of assumptions.

Result: Fair Value of $20.88 (UNDERVALUED)

However, there is still real risk that weaker Permian volumes or tougher contract renewals could pressure margins and undercut the earnings power embedded in this narrative.

Another Take on Valuation

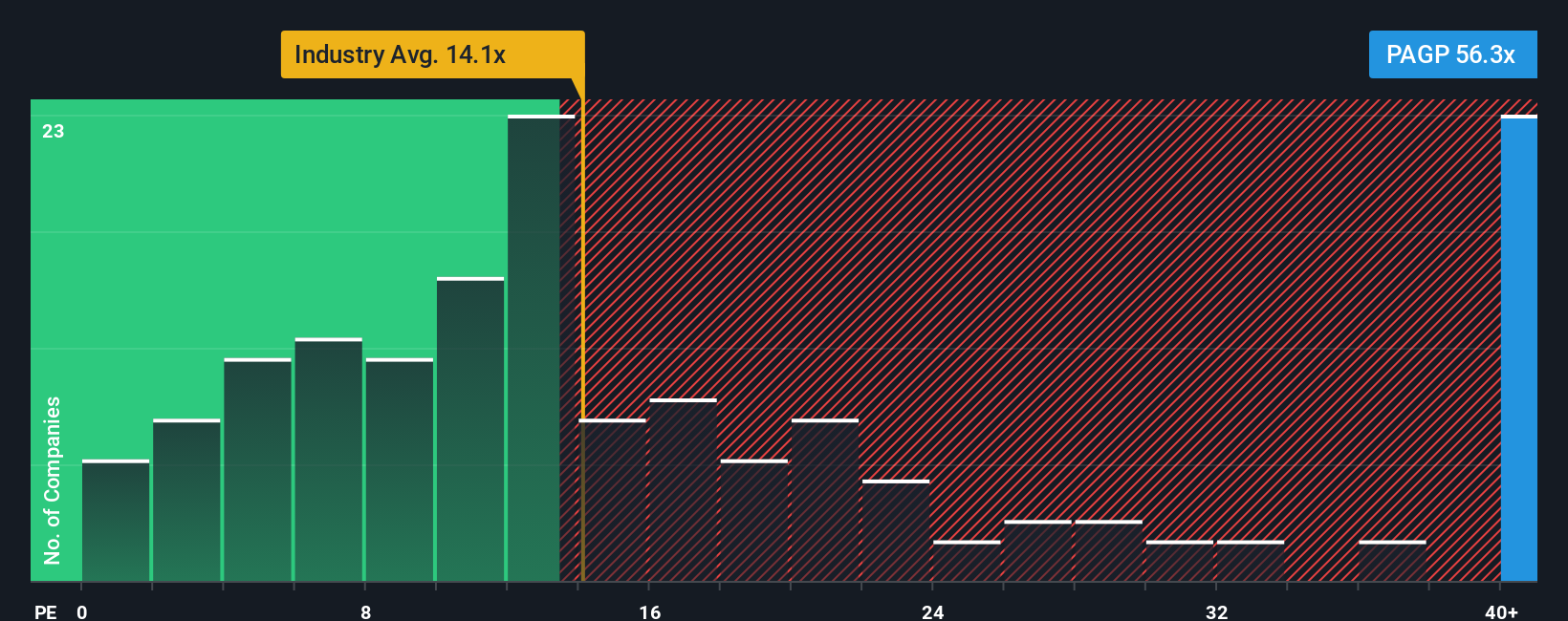

The narrative fair value suggests Plains GP Holdings is only about 2.2% undervalued, but the earnings multiple tells a very different story. PAGP trades on a P/E of 65.2x versus 13.6x for the US Oil and Gas industry, 31x for peers, and a fair ratio of 22.7x.

That gap implies the market is paying a hefty premium for current earnings. This could indicate either a rich price for a pipeline operator or confidence that future profit growth will justify it. Which side of that trade do you feel more comfortable with?

Build Your Own Plains GP Holdings Narrative

If you look at these numbers and reach a different conclusion, or simply prefer to test your own assumptions, you can build a personalised view in just a few minutes with Do it your way.

A great starting point for your Plains GP Holdings research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you are weighing up Plains GP Holdings, it is worth lining it up against fresh ideas so you are not relying on a single opportunity.

- Zero in on potential value candidates by scanning these 886 undervalued stocks based on cash flows that stand out on cash flow based metrics.

- Tap into growth themes by checking out these 23 AI penny stocks that are tied to artificial intelligence trends across different industries.

- Build a cash flow focused watchlist by reviewing these 13 dividend stocks with yields > 3% that offer yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.