Assessing Plains GP Holdings (PAGP) Valuation After Recent Share Price Swings

Plains GP Holdings LP Class A PAGP | 23.36 23.31 | -0.93% -0.21% Post |

Plains GP Holdings overview

Plains GP Holdings (PAGP) has recently shown mixed short term moves, with a 2.3% decline over the past day contrasting with gains over the past week, month, and past 3 months, putting recent trading in sharper focus for investors.

That 2.3% one day drop sits against a 7.9% 30 day share price return and an 18.2% 90 day share price return, while the 5 year total shareholder return of 249.2% highlights how powerful compounding income and reinvested distributions have been over time.

If this midstream story has you thinking about where energy infrastructure meets future power demand, it could be a good moment to scan 24 power grid technology and infrastructure stocks for new ideas beyond Plains GP Holdings.

With the share price sitting close to analyst targets and an estimated intrinsic value gap still showing, the key question is whether Plains GP Holdings is quietly undervalued or whether the market is already pricing in future growth.

Most Popular Narrative: 80% Undervalued

With Plains GP Holdings closing at $20.71 against a narrative fair value of $20.88, the current price sits just below that modelled estimate while still reflecting a large discount to the longer term cash flow view.

The planned divestiture of the NGL segment and redeployment of ~$3 billion in proceeds into core crude oil operations and bolt-on acquisitions are expected to streamline operations, reduce commodity price exposure, and enhance financial flexibility, supporting growth in core revenue and improved net margins via higher-return investments and potential buybacks.

Curious what kind of revenue path, margin rebuild, and future earnings multiple are baked into that fair value line? The most followed narrative lays out an earnings ramp, a richer P/E than the wider oil and gas group, and a specific discount rate that together do the heavy lifting. The full story connects all three into one valuation roadmap.

Result: Fair Value of $20.88 (UNDERVALUED)

However, this storyline can quickly change if crude volumes soften, or if margin pressure from contract roll offs and higher capital needs weighs on earnings and cash generation.

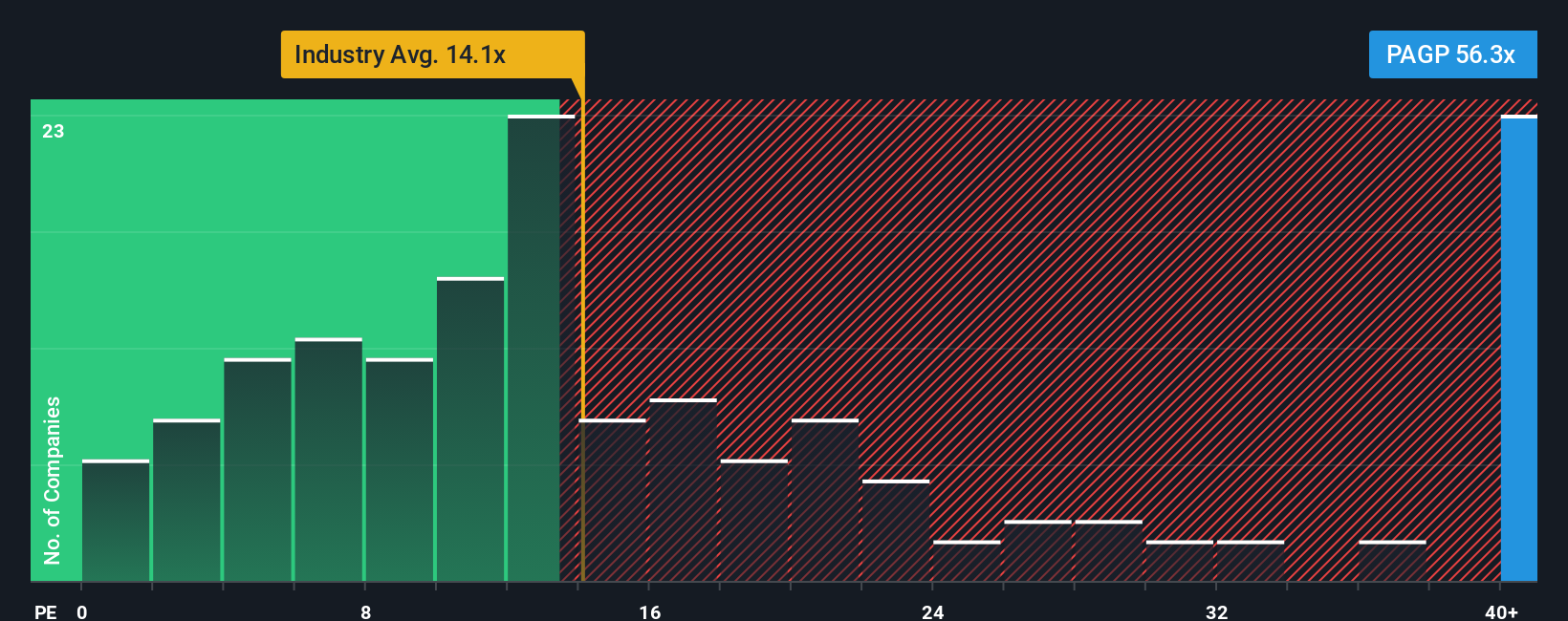

Another View: Earnings Multiple Raises a Caution Flag

That big 80% discount to fair value sits awkwardly beside a very different signal from the current P/E. Plains GP Holdings trades on roughly 66x earnings, while the US Oil and Gas group sits near 14x, peers around 33x, and the fair ratio is 23.6x. In plain terms, the share price already assumes a lot going right, which raises the question of how much margin for error is truly left.

Build Your Own Plains GP Holdings Narrative

If you look at this and think the assumptions do not quite fit your view, you can stress test the same data, adjust the key inputs, and build a version that reflects your own thesis in just a few minutes with Do it your way.

A great starting point for your Plains GP Holdings research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Plains GP Holdings sits on your watchlist, do not stop there. A broader mix of ideas can help you balance risk, income, and growth potential.

- Target potential value opportunities by checking companies that screen well on cash flows and balance sheets through 53 high quality undervalued stocks so you do not overlook candidates on sale.

- Strengthen your income game by scanning reliable payers in 14 dividend fortresses and see which names could help anchor your portfolio with regular cash returns.

- Prioritise resilience by reviewing companies with lower risk profiles using 86 resilient stocks with low risk scores before the rest of the market starts paying closer attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.