Assessing Pool Corporation (POOL) Valuation After CEO Transition To John B. Watwood

Pool Corporation POOL | 0.00 |

Pool (POOL) has drawn fresh attention after announcing a leadership transition, with John B. Watwood set to take over as President and CEO on May 4, 2026, succeeding Peter D. Arvan.

At a share price of $175.35, Pool’s recent leadership announcement comes after a period where the 30 day share price return declined 23% and the 1 year total shareholder return declined 44%. This points to fading momentum ahead of the CEO transition.

If this leadership change has you reassessing your watchlist, it could be a good moment to broaden your search and check out 18 top founder-led companies

With Pool’s stock down sharply over 1 and 5 years, but trading at a reported 41% discount to one intrinsic estimate and 49% below one analyst price target, should you view this as potential undervaluation or assume the market is already accounting for future growth in the current price?

Most Popular Narrative: 34.2% Undervalued

Pool's most followed valuation narrative places fair value at about $266 per share, well above the last close of $175.35, which frames the current discount as significant in that model.

Expansion of private label offerings (especially chemicals), alongside supply chain and digital platform investments (e.g., POOL360), are driving margin enhancing product mix and operational efficiencies, supporting gross and net margin improvement over time. Increased adoption of e-commerce channels (POOL360 up to 17% of sales) and new location openings in dense pool markets are enabling customer retention, service differentiation, and efficient market penetration, strengthening competitive positioning and enhancing future earnings potential.

Want to see what kind of earnings base and profit margins that narrative is banking on, and how that stacks up against the implied valuation multiple? The full narrative spells out the growth path and profitability profile that need to line up for that fair value to make sense.

Result: Fair Value of $266 (UNDERVALUED)

However, that story can unravel if housing turnover stays weak and Pool’s heavy focus on North America leaves earnings more exposed to prolonged domestic softness.

Another View: P/E Sends a Different Signal

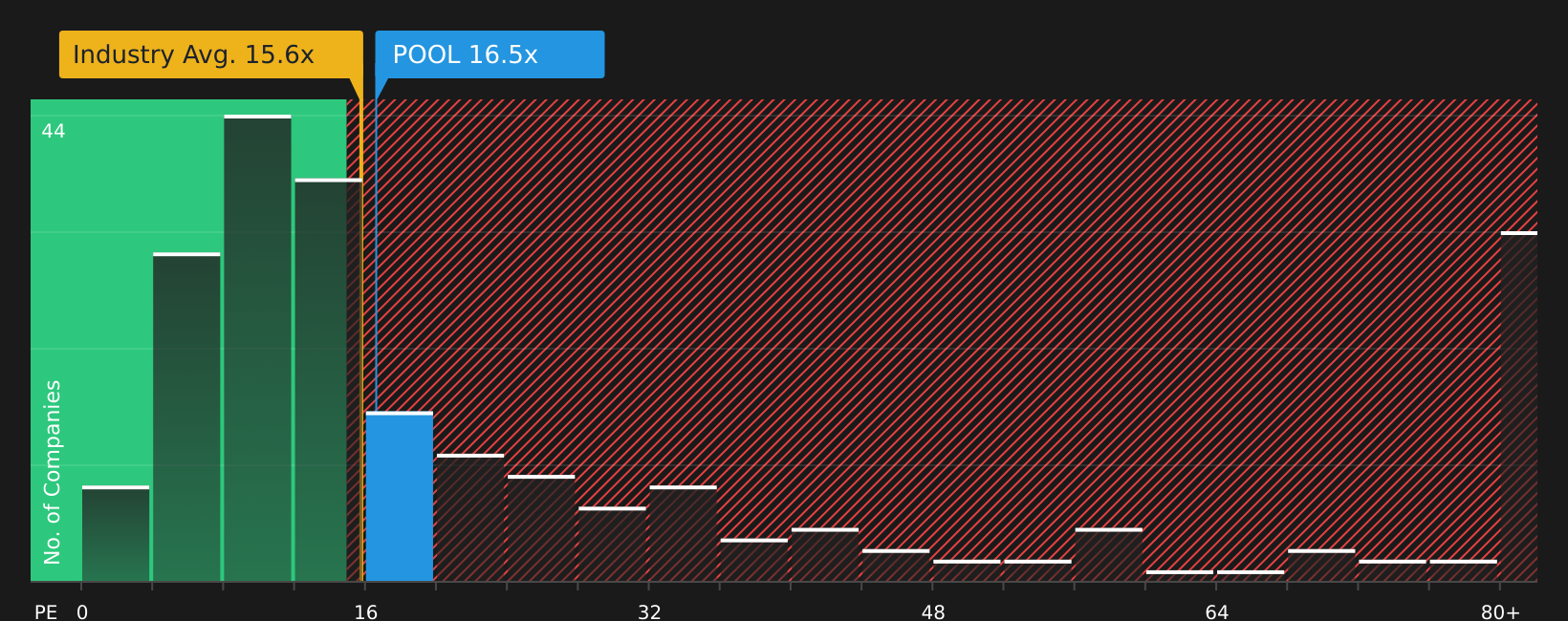

While the narrative and intrinsic estimates point to undervaluation, Pool’s current P/E of 15.8x looks full compared with a peer average of 12.5x and a fair ratio of 15x. If the market shifts closer to those lower benchmarks, how comfortable are you with the downside this could imply?

Next Steps

If this mix of pressure and potential has you torn, move quickly to review the full picture of risks and upsides with 4 key rewards and 1 important warning sign

Looking for more investment ideas?

If Pool is already on your radar, do not stop there. Broadening your opportunity set now could make a real difference to your long term returns.

- Target resilience by checking out companies with stronger financial footing through the solid balance sheet and fundamentals stocks screener (45 results).

- Zero in on potential mispricings by scanning the 51 high quality undervalued stocks before the crowd catches on.

- Get ahead of the market by reviewing the screener containing 21 high quality undiscovered gems that most investors are not watching yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.