Assessing Powell Industries (POWL) Valuation After Data Center Megaproject Wins And Backlog Growth

Powell Industries, Inc. POWL | 230.94 227.14 | +0.06% -1.64% Pre |

Powell Industries (POWL) just completed a three-for-one stock split, following a bylaw amendment that lifted authorized common shares to 90 million, keeping investors focused on liquidity and access rather than headline price.

The stock split comes after a powerful run, with a 90 day share price return of 81.82% and an 85.58% year to date share price return. The 1 year total shareholder return is very large, signaling strong momentum tied to data center and electrification themes.

If this kind of momentum has your attention, it could be a good time to see what else is moving in power infrastructure and grid technology via the 30 power grid technology and infrastructure stocks

With Powell Industries trading around $218 a share after such a strong run, the key question now is simple: is the stock still offering value or is the market already pricing in years of future growth?

Most Popular Narrative: 19% Undervalued

Powell Industries last closed at $218.07, while the most followed narrative places fair value at $269.26, framing the recent surge against a richer long term story.

The market may be pricing in sustained outsized revenue growth and backlog conversion driven by robust order activity in electric utility, data center, and offshore energy infrastructure sectors benefiting from the accelerating buildout of electrification and grid modernization, resulting in potentially over optimistic top line expectations. Expectations appear elevated for durable gross margin improvement on the basis of recent project execution, pricing power, and product mix, although management noted a significant portion of recent margin gains were one time project closeouts that may not recur, raising the risk of margin normalization and earnings disappointment.

Curious how a company with tempered margin assumptions still lands above the current price? Revenue growth, earnings power, and a richer future multiple quietly do the heavy lifting.

Result: Fair Value of $269.26 (UNDERVALUED)

However, elevated expectations for sustained high margins and smooth integration of acquisitions like Remsdaq could unwind quickly if the project mix shifts or execution stumbles.

Another View: Rich Multiple Signals Caution

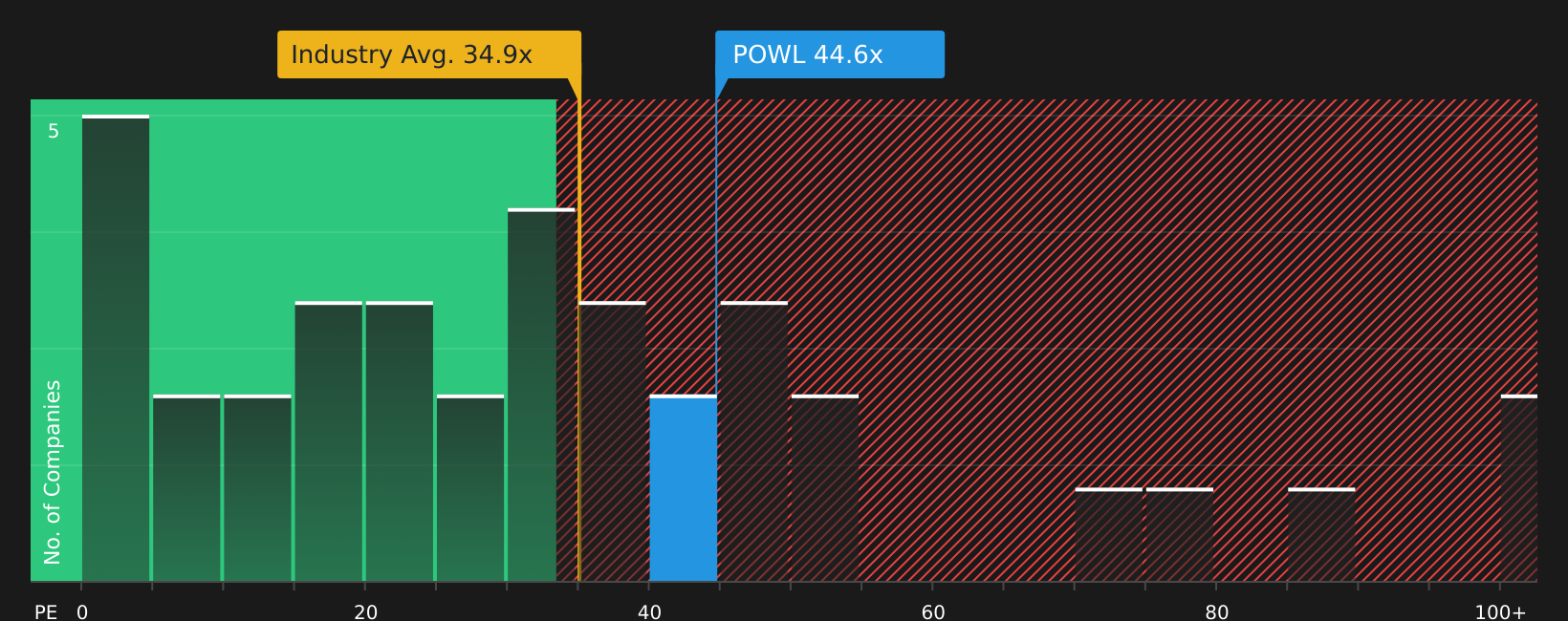

While the narrative fair value points to Powell Industries as 19% undervalued at $269.26, the current P/E of 42.4x tells a different story. It sits well above the estimated fair ratio of 29.9x and above the US Electrical industry average of 32.4x, even though it is below a 70.9x peer average. That gap suggests sentiment is already paying up for quality, so the key question is how much room is really left if expectations cool?

Next Steps

Mixed signals so far, right? With strong recent returns but a mix of risks and rewards in the background, it makes sense to move quickly and check the details for yourself. Start with the 2 key rewards and 1 important warning sign.

Looking for more investment ideas?

If Powell Industries is on your radar, do not stop here. The real edge comes from lining it up against other strong ideas before you commit.

- Target value with focus by scanning for companies that look attractively priced with quality fundamentals through the 64 high quality undervalued stocks.

- Strengthen your income stream by zeroing in on companies offering reliable payouts via the 12 dividend fortresses.

- Sleep easier at night by comparing Powell Industries to companies screened as having resilient profiles using the 72 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.