Assessing Procter & Gamble (PG) Valuation After Mixed Share Price Performance And Conflicting Fair Value Views

Procter & Gamble Company PG | 0.00 |

Why Procter & Gamble (PG) is Back on Investors’ Radar

Procter & Gamble (PG) stock is drawing fresh attention after a recent stretch of mixed returns, including a gain over the past month alongside a decline over the past 3 months and the past year.

PG’s recent 3.4% one month share price return contrasts with an 8.2% three month share price decline and a 5.3% one year total shareholder return loss. This suggests that momentum has faded after earlier strength.

If you are considering where else consumer staples style resilience might show up in the market, this is a good moment to broaden your search with 18 top founder-led companies

With PG trading at $146.06, sitting at a 12.1% discount to the average analyst price target and a 21.3% gap to one estimate of intrinsic value, you have to ask: is this a genuine opening, or is the market already baking in future growth?

Most Popular Narrative: 20.7% Overvalued

Compared with PG’s last close at $146.06, the most followed narrative pegs fair value at $121.06, using an 8.32% discount rate as the yardstick.

Procter & Gamble, despite operating in a very competitive industry, still has some competitive advantages, shown in its higher operating margin above the ~20% mark and the Morning Star Wide Moat. Also, the fact that the ROIC is double the Cost of Capital means its capital allocation is being well managed.

It may seem counterintuitive that a wide moat, premium margins and disciplined capital allocation can still coincide with an overvaluation call at today’s price. The narrative leans heavily on measured revenue growth, modest earnings expansion and a specific dividend path to reach its fair value. The tension between quality metrics and these tempered growth assumptions is what really drives that $121.06 figure.

Result: Fair Value of $121.06 (OVERVALUED)

However, this overvaluation case could be challenged if revenue or profitability trends differ materially from the assumptions used, or if investor appetite for premium consumer staples shifts.

Another Angle on Valuation

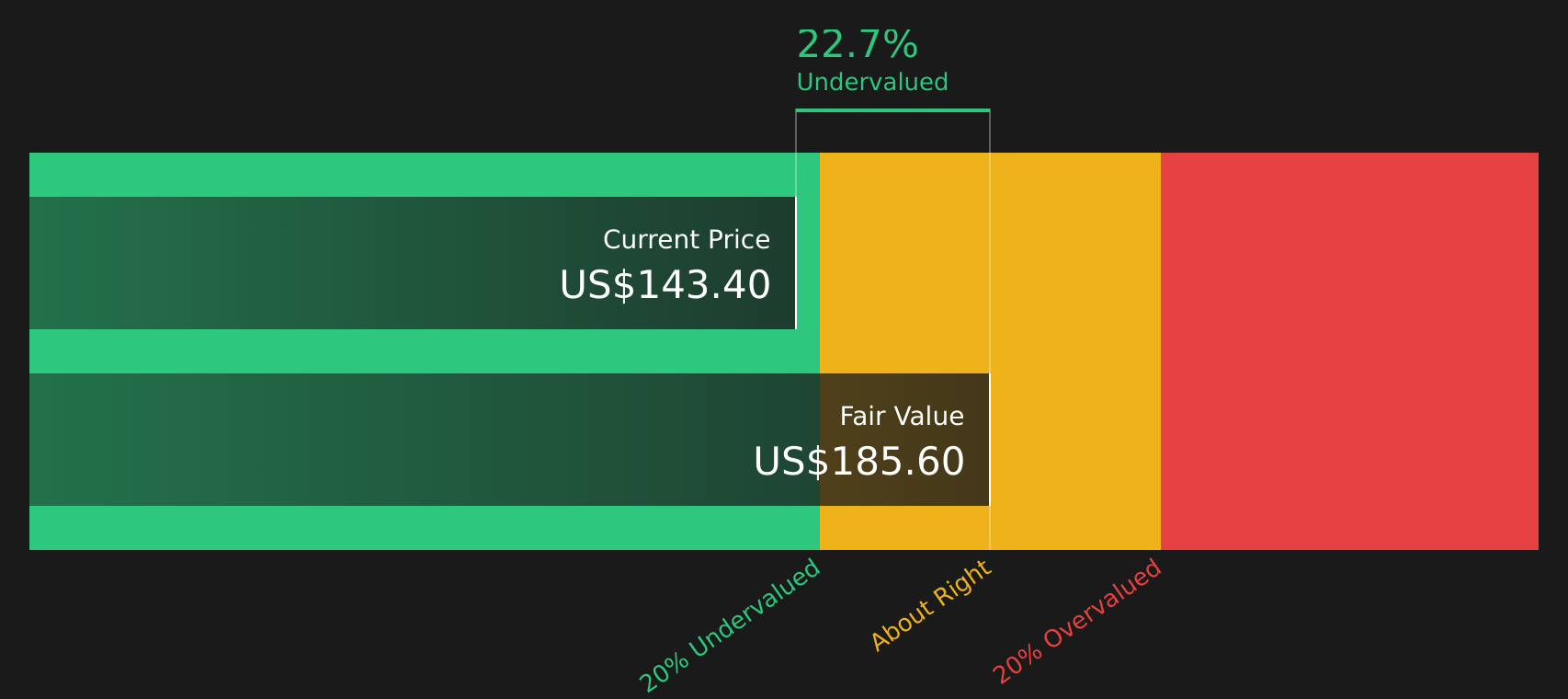

The most followed narrative points to PG trading about 20.7% above its $121.06 fair value estimate, yet our DCF model paints a very different picture. On those assumptions, PG at $146.06 screens as undervalued compared with an estimated future cash flow value of $185.60, raising the question of which set of inputs you trust more.

For a closer look at how different growth, margin and discount rate assumptions affect that cash flow based estimate, and how sensitive the outcome is to small tweaks, Look into how the SWS DCF model arrives at its fair value.

Next Steps

Conflicted by the mix of caution and optimism in this story? Take a moment to check the data for yourself and weigh the 4 key rewards and 2 important warning signs

Looking for more investment ideas?

If you only stop at PG, you could miss other opportunities that fit your style. Take a few minutes to scan the wider market with targeted stock lists.

- Spot potential value opportunities early by running your own filter across 51 high quality undervalued stocks that combine quality fundamentals with pricing that may look appealing.

- Prioritise resilience and sleep easier at night by focusing on 72 resilient stocks with low risk scores designed for investors who care about steadier profiles.

- Cast a wider net across companies with strong foundations using the solid balance sheet and fundamentals stocks screener (44 results) to see which ones meet your quality bar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.