Assessing Procter & Gamble (PG) Valuation After Q2 Results And Major Brand Marketing Push

Procter & Gamble Company PG | 143.41 | -0.67% |

Procter & Gamble (PG) is back in focus after Q2 results, fresh product launches such as Old Spice’s Spice Alchemist collection, and heavy brand promotion around Super Bowl LX and the Milano Cortina 2026 Games.

The recent marketing push around Super Bowl LX and Milano Cortina 2026 lines up with a strong run in the shares, with a 30 day share price return of 13.37% and an 11.86% year to date share price gain. The 1 year total shareholder return of a 3.5% decline contrasts with 3 year and 5 year total shareholder returns of 24.94% and 40.21%, suggesting near term momentum has picked up after a softer year.

If this consumer brands story has caught your eye, it could be a good moment to broaden your watchlist and check out 22 top founder-led companies as potential long term compounders.

With PG shares up double digits over the past month and trading at about a 6% gap to the average analyst price target, the key question now is simple: is there still value on the table, or is the market already pricing in future growth?

Most Popular Narrative: 31% Overvalued

According to the most widely followed narrative on Procter & Gamble, the current share price of $158.61 sits well above an assessed fair value of $121.06, creating a sizable valuation gap that hinges on how you see growth and cash generation playing out over time.

Procter & Gamble, despite being within a very competitive industry, still has some competitive advantages, shown in its higher operating margin above the ~20% mark and the Morning Star Wide Moat. Also, the fact that the ROIC is double the Cost of Capital means its capital allocation is being well managed. Its solid Moodys Debt Rating, along with the Low Uncertainty Morningstar rating, maintains the company as a stable and reliable investment if the opportunity arises.

Want to see how a wide moat, strong returns on capital and a measured growth outlook combine to reach that fair value? The key assumptions behind the revenue runway, margin profile and payout path might surprise you. Curious which inputs really move the model and which barely matter to the final number? The full narrative lays out that framework in detail.

Result: Fair Value of $121.06 (OVERVALUED)

However, this storyline could be challenged if revenue growth around 3% and earnings expansion closer to 5% do not support current multiples, or if discount rate assumptions shift meaningfully.

Another View: Fair Ratio Points To A Tighter Margin Of Safety

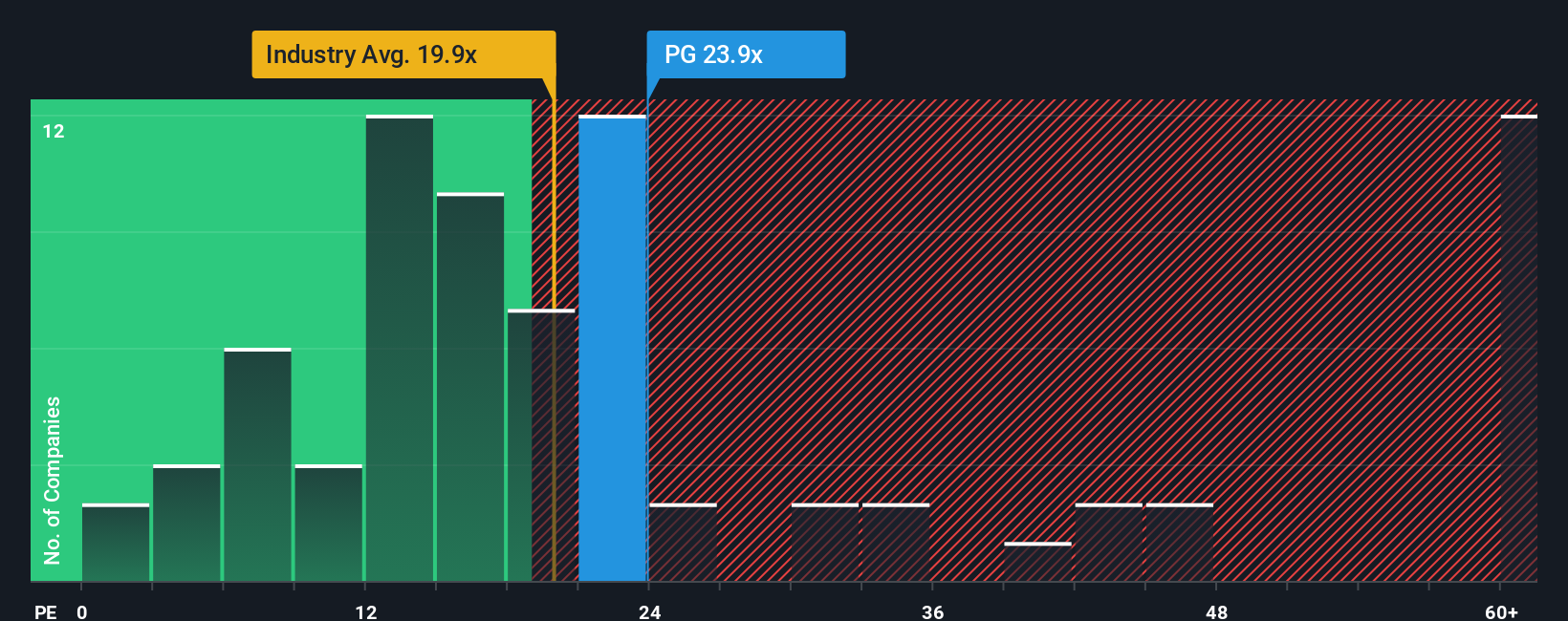

That 31% overvalued narrative sits awkwardly next to our P/E fair ratio work, which suggests PG is good value. The current P/E is 22.8x versus a fair ratio of 23.8x, while the Global Household Products group sits lower at 17.6x and close peers cluster higher around 27.2x.

In plain terms, the shares are priced at a premium to the broader industry, but at a discount to similar large peers and only slightly below where the fair ratio suggests the P/E could settle. For you, the tension is simple: is this a slim margin of safety or a reasonable price for quality?

Build Your Own Procter & Gamble Narrative

If you look at the numbers and come to a different conclusion, or simply prefer to kick the tires yourself, you can build a personal thesis in just a few minutes, starting with Do it your way.

A great starting point for your Procter & Gamble research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If PG has you rethinking your watchlist, this is the moment to widen your scope and line up a few fresh candidates for deeper research.

- Start with quality first by checking out companies in our solid balance sheet and fundamentals stocks screener (46 results), where financial strength takes center stage before you even look at growth stories.

- Hunt for value by scanning 55 high quality undervalued stocks, which highlights businesses that our models flag as offering strong fundamentals relative to their current prices.

- Prioritize resilience and sleep a little easier by reviewing 81 resilient stocks with low risk scores, built to surface companies with lower risk scores that may better fit a cautious playbook.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.