Assessing Quest Diagnostics (DGX) Valuation As Shares Trade On An 11.44% Year To Date Return

Quest Diagnostics Incorporated DGX | 0.00 |

Why Quest Diagnostics Stock Is On Investors’ Radar

Quest Diagnostics (DGX) is drawing attention after its recent trading performance, with the stock near US$193 and multi year total returns that stand out against its long operating history in diagnostic testing services.

The current share price of US$193.67 sits alongside an 11.44% year-to-date share price return and a 67.50% five-year total shareholder return, suggesting long-term holders have seen far stronger gains than recent traders.

If Quest Diagnostics has you thinking about where else consistent compounding might be hiding, it could be a good time to scan the market using the 20 top founder-led companies

With Quest Diagnostics delivering double digit total returns over one and five years and trading around US$193.67, the real question is whether the current valuation leaves any upside on the table or if the stock already reflects future growth.

Preferred P/E of 21x: Is it justified?

Quest Diagnostics is trading on a P/E of 21x, which sits below both the US Healthcare industry average of 22.9x and a peer average of 33.5x, while the stock last closed at $193.67.

The P/E ratio links the current share price to earnings, so it gives a quick sense of how much the market is paying for each dollar of profit. For a mature healthcare services business with established operations, this is a commonly used yardstick because earnings are a central focus for many investors.

Here, the stock is described as good value compared to peers and the broader industry, and also relative to an estimated fair P/E of 22.9x. This indicates that the current market price is not stretching the earnings profile in comparison with similar healthcare companies, and that the valuation may move closer to that fair ratio if sentiment or fundamentals change.

Result: Price-to-Earnings of 21x (UNDERVALUED)

However, you still need to weigh pressures on healthcare spending and potential changes to testing reimbursement. Both factors could challenge Quest Diagnostics’ current earnings power.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

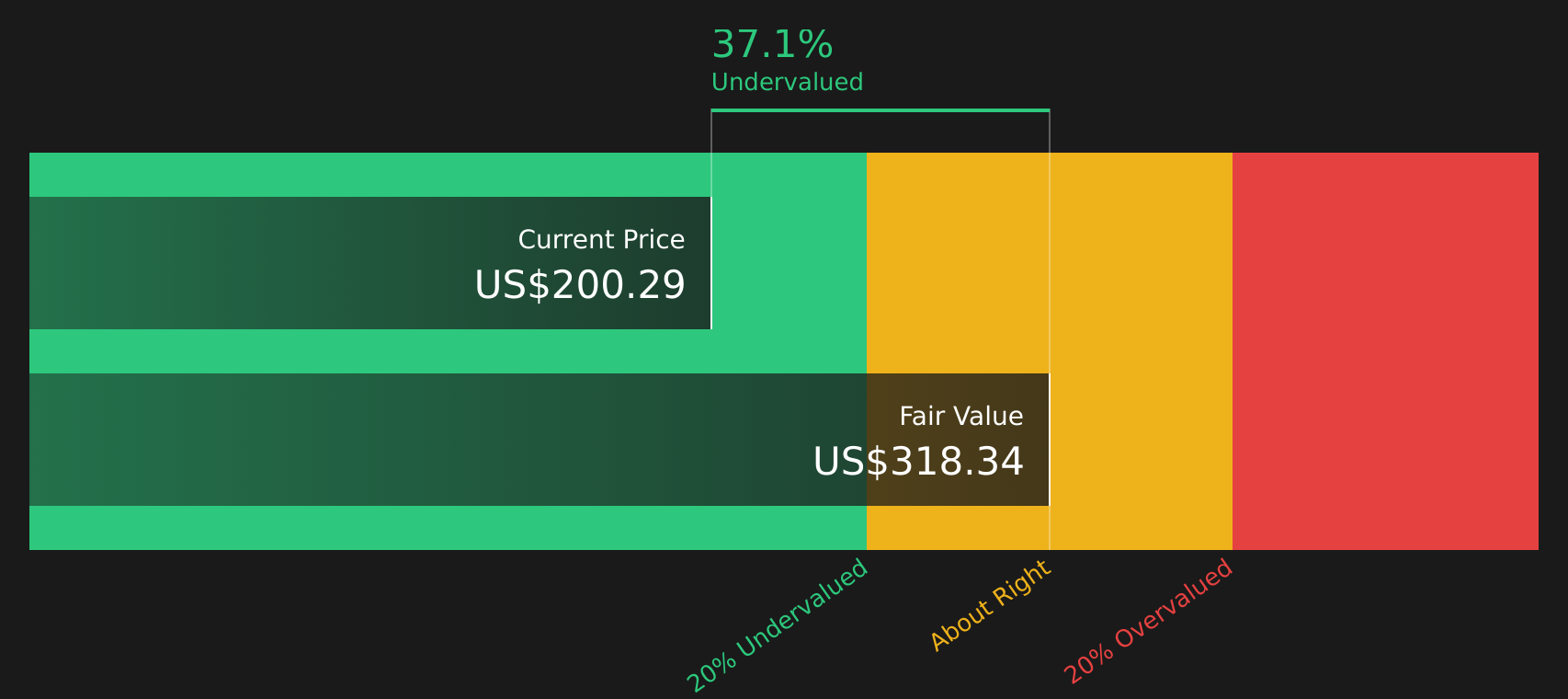

Another View: Cash Flows Paint An Even Cheaper Picture

The P/E of 21x already suggests Quest Diagnostics is not aggressively priced. The SWS DCF model goes further, with an estimated future cash flow value of $318.98 per share versus the current $193.67. That gap implies investors may be applying a heavy discount to future cash flows. The question is whether that discount proves cautious or excessive.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Quest Diagnostics for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With both the valuation signals and the mixed sentiment around Quest Diagnostics in mind, this is a good moment to look at the underlying data yourself, compare the positives and negatives, and square them with your own risk tolerance using the 4 key rewards and 1 important warning sign

Looking for more investment ideas?

If Quest Diagnostics has sharpened your focus, do not stop here. Some of the most interesting opportunities show up when you systematically scan the market.

- Target potential income pillars by reviewing companies in the 10 dividend fortresses and see which ones line up with your cash flow goals.

- Hunt for quality at a discount with the 47 high quality undervalued stocks and compare how these stocks stack up against what you already own.

- Spot lower volatility options using the 63 resilient stocks with low risk scores so you are not missing steadier ideas while everyone chases the headlines.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.