Assessing Rambus (RMBS) Valuation After CFO Transition And New Board Appointment

Rambus Inc. RMBS | 120.02 120.25 | -1.40% +0.19% Pre |

Rambus (RMBS) is in the spotlight after a cluster of leadership updates, including the planned resignation of CFO Desmond Lynch, the appointment of interim CFO John Allen, reaffirmed guidance, and the addition of semiconductor veteran Victor Peng to its board.

The recent 6.42% 1 day share price return, taking Rambus to US$101.95, sits against a relatively modest 2.69% year to date share price return and a much stronger 61.93% total shareholder return over the past year. This suggests momentum has recently picked up after a solid multi year run that includes a 130.60% three year and very large five year total shareholder return.

If leadership changes and AI related board experience have caught your eye, this could be a good moment to scan 34 AI infrastructure stocks as a way to spot other potential semiconductor infrastructure ideas.

With Rambus posting US$707.63 million in annual revenue, US$230.46 million in net income, and trading at US$101.95, the key question is simple: are you looking at an undervalued AI infrastructure enabler or a stock where the market is already pricing in future growth?

Most Popular Narrative: 13.5% Undervalued

At a last close of $101.95 versus a narrative fair value of $117.88, Rambus is framed as undervalued, with that view hinging on long term AI and data center demand assumptions.

Ongoing rapid growth in AI and data center workloads is accelerating the industry's need for high-speed memory interfaces and connectivity, driving demand for Rambus's DDR5, HBM4, and PCIe 7.0 solutions. This positions the company for sustained top-line revenue growth as new design wins and customer qualifications convert into production orders.

Curious what has to happen in AI infrastructure for that fair value to hold up? Revenue ramps, margin assumptions, and a punchy future earnings multiple are doing the heavy lifting here, and the full narrative spells out those moving parts in detail.

Result: Fair Value of $117.88 (UNDERVALUED)

However, there is still meaningful risk if DDR5 driven demand, MRDIMM adoption, or newer companion chips ramp more slowly than analysts currently expect.

Another Way To Look At Valuation

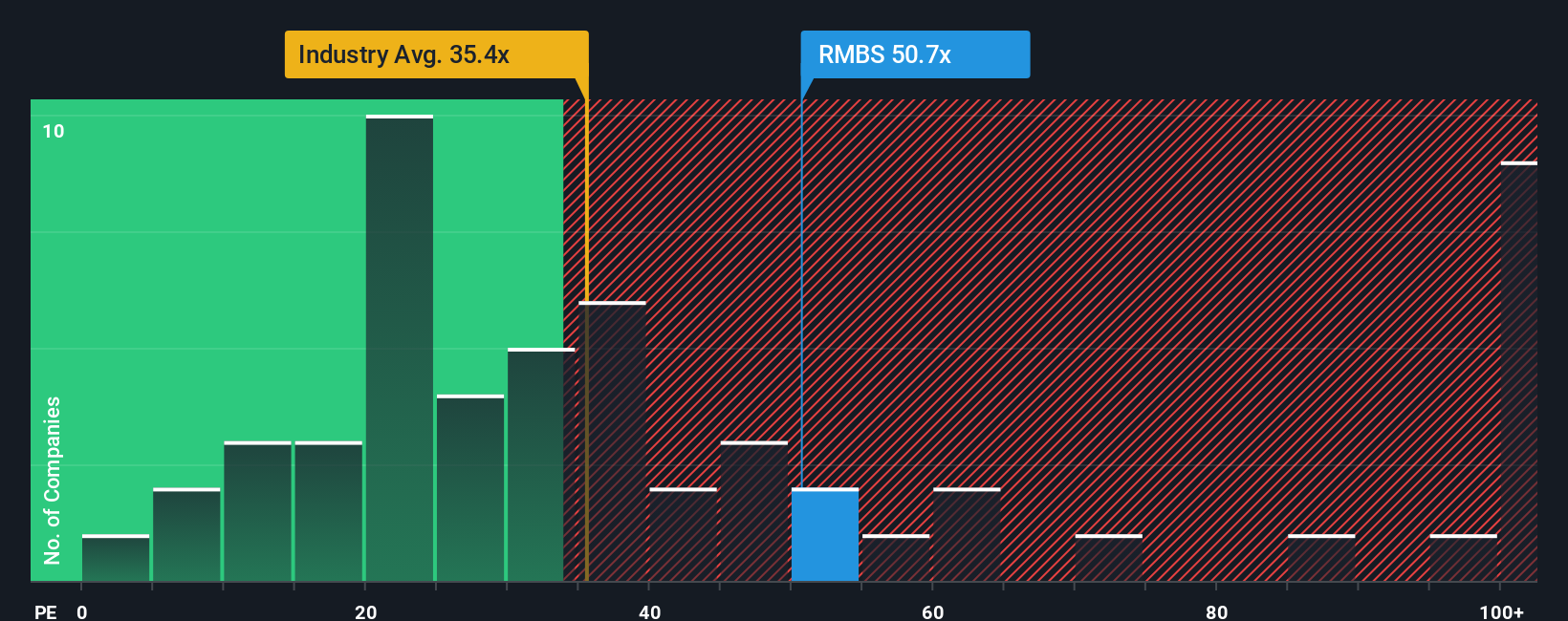

The popular AI narrative paints Rambus as 13.5% undervalued, but the picture changes when you look at the P/E. At 47.6x earnings, the stock trades above the US Semiconductor industry at 43.2x and above a fair ratio of 42.4x, which points to valuation risk if expectations cool.

That gap versus both peers at 54.7x and the 42.4x fair ratio leaves you weighing how much optimism is already in the price, and how comfortable you are if sentiment or earnings forecasts shift from here.

Build Your Own Rambus Narrative

If you see the numbers differently or want to stress test your own assumptions, you can quickly build a custom Rambus story yourself, then Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Rambus.

Looking for more investment ideas?

If Rambus has sharpened your thinking, do not stop here. Use a wider set of ideas to pressure test your next move with real numbers behind them.

- Spot potential bargains early by scanning our screener containing 23 high quality undiscovered gems that pair strong fundamentals with limited market attention.

- Prioritise resilience by checking companies in the 85 resilient stocks with low risk scores where business quality and risk scores aim to keep surprises in check.

- Focus on financial strength by reviewing the solid balance sheet and fundamentals stocks screener (44 results) so you are not caught off guard by hidden leverage or weak liquidity.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.