Assessing Rambus (RMBS) Valuation As AI And DDR5 Demand Drive Strong Business Momentum

Rambus Inc. RMBS | 93.03 | +3.42% |

Rambus (RMBS) is seeing business momentum pick up as demand for memory and AI focused chips climbs, supported by new DDR5 and AI accelerator products for data centers and broadly positive analyst coverage.

Recent trading has reflected this AI driven story, with a 22.95% 1 month share price return and a 16.55% year to date share price return contributing to a 92.43% 1 year total shareholder return.

If Rambus's AI and data center exposure has caught your eye, it could be a useful prompt to scan other high growth tech and AI names using high growth tech and AI stocks.

After a 1 year total return of 92.43% and a last close of US$115.71, which is near an average analyst price target of US$120, the key question now is whether Rambus still offers upside or if the market is already pricing in future growth.

Most Popular Narrative: 3.6% Undervalued

Rambus's most followed narrative pegs fair value at $120, slightly above the last close of $115.71, which lines up with the current analyst target.

The analysts have a consensus price target of $81.875 for Rambus based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $91.0, and the most bearish reporting a price target of just $73.0.

Curious how this narrative now supports a higher $120 fair value instead? Earnings, revenue expectations and profit margins all play a part, along with a premium future P/E multiple. Want to see how those moving pieces fit together to back that number?

Result: Fair Value of $120 (UNDERVALUED)

However, this story can change quickly if Rambus's heavy reliance on DDR5 demand, new companion chips, or MRDIMM timing does not play out as analysts expect.

Another View: Rich P/E Signals Higher Expectations

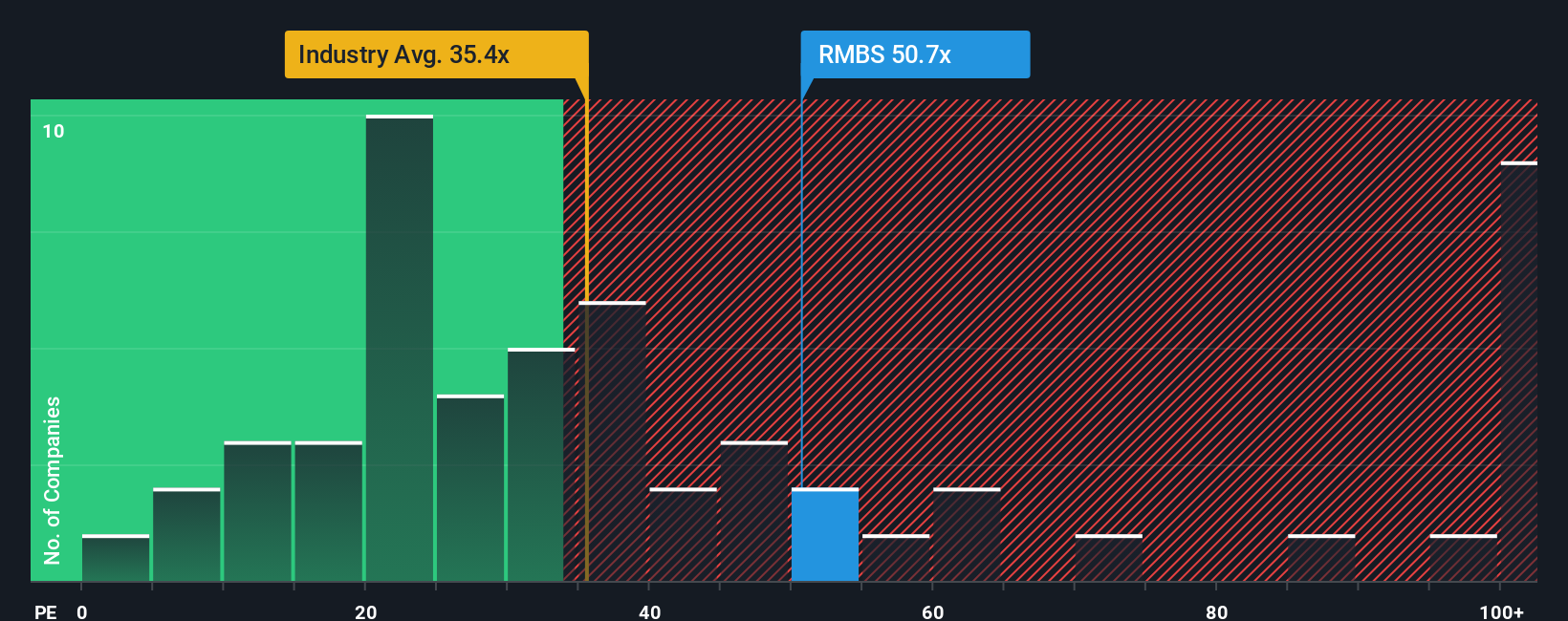

The AI narrative points to a fair value of $120, yet Rambus is trading on a P/E of 54.4x, well above the US Semiconductor industry at 41.1x and its own fair ratio of 38.3x. That gap suggests investors are paying up for growth. How comfortable are you with that extra valuation risk?

Build Your Own Rambus Narrative

If you look at the numbers and come to a different conclusion, or simply prefer to test your own assumptions, you can build a fresh Rambus view in just a few minutes with Do it your way.

A great starting point for your Rambus research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Ready to widen your list of ideas?

If Rambus has sharpened your interest in AI and future focused themes, do not stop here. Broaden your watchlist with a few targeted idea sets.

- Spot potential value opportunities early by scanning these 879 undervalued stocks based on cash flows that may offer more attractive pricing based on cash flows.

- Consider AI-related momentum in a broader way by reviewing these 24 AI penny stocks capturing companies tied to artificial intelligence trends.

- Add a different growth angle by checking out these 19 cryptocurrency and blockchain stocks linked to cryptocurrency and blockchain themes.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.