Assessing Red Cat Holdings (RCAT) Valuation After Record Q1 Revenue And New Japanese Army Drone Contract

RED CAT HOLDINGS RCAT | 0.00 |

Red Cat Holdings (RCAT) is in focus after reporting record fiscal Q1 2026 revenue, supported by U.S. Army and NATO deliveries, strong FlightWave Edge 130 and Black Widow demand, and a new Japanese Army Black Widow contract.

The earnings release and recent Japanese Army contract have kept Red Cat on traders’ screens. The share price is up 8.49% in the last day and 22.82% year to date, while the 1-year total shareholder return of 82.93% points to strong momentum over a longer stretch, despite share price returns over the past 30 and 90 days being down 9.05% and 10.86% respectively.

If this kind of defense tech story interests you, it could be a good moment to see what else is moving in the sector and check out 32 robotics and automation stocks

With the stock up sharply over the past year and trading at a steep discount to the latest analyst price target, the key question is whether Red Cat is still undervalued or if markets are already pricing in future growth.

Most Popular Narrative: 33.8% Undervalued

Red Cat's most followed narrative pegs fair value at $17 per share, compared with the last close of $11.25. This frames a sizeable valuation gap for investors to weigh.

Expansion into uncrewed surface vessels through Blue Ops, with planned capacity for 500 to 1,000 vessels per year and unit pricing mentioned between about US$750,000 and US$1.5 million, adds a second major product line that could diversify and scale revenue beyond current drone programs.

Curious what has to happen for that $17 fair value to stack up? The narrative leans on rapid revenue expansion, firmer margins and a rich future earnings multiple.

Result: Fair Value of $17 (UNDERVALUED)

However, there are still clear risks here, especially if defense drone demand underwhelms expectations or if the large Blue Ops and factory buildouts fail to reach efficient scale.

Another View: Rich On Sales, Despite The Discount Story

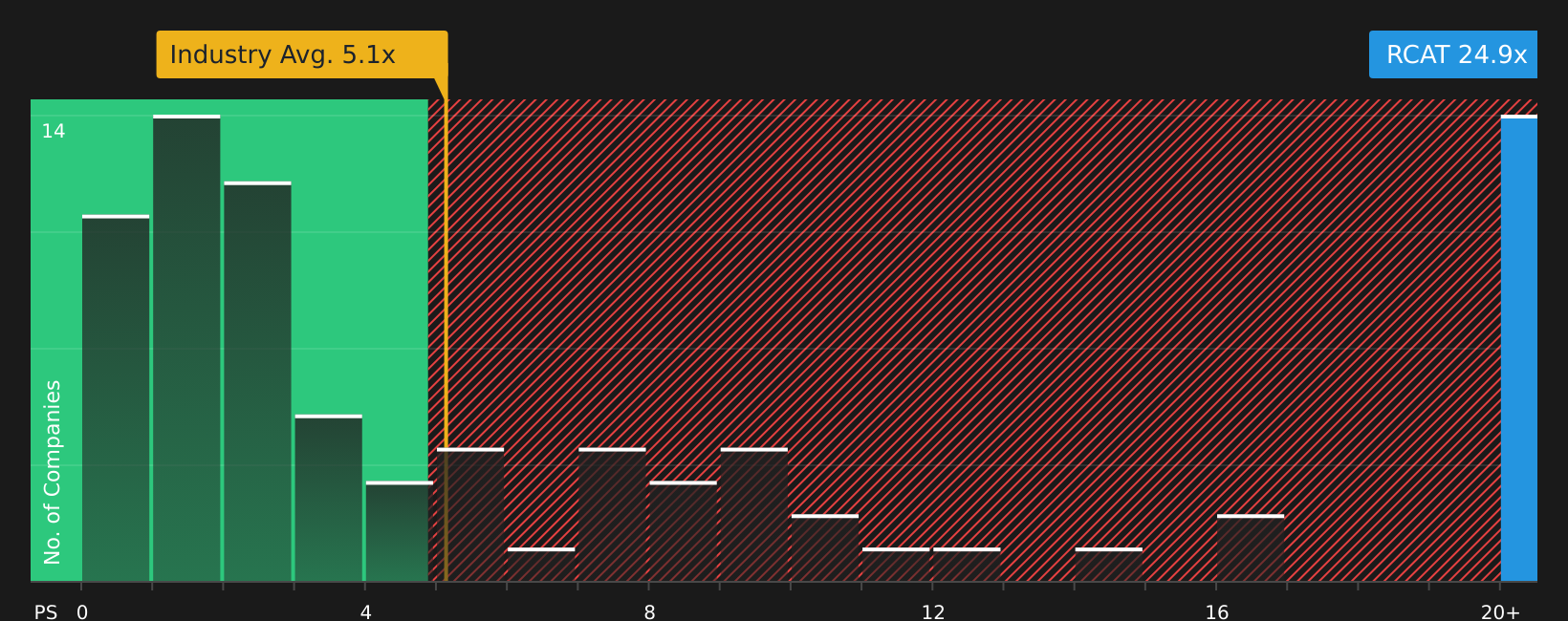

While the popular narrative leans on a 33.8% discount to a $17 fair value, the current P/S of 25.3x looks heavy compared with the fair ratio of 7.3x, the US Aerospace & Defense average of 5.2x and a peer average of 21.5x. That gap points to meaningful valuation risk if sentiment cools.

Investors relying on sales based yardsticks may want to see exactly how this premium stacks up across peers in more detail, starting with See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With mixed signals on valuation and future execution, sentiment here is clearly split, so act promptly, review the details yourself and weigh the 2 key rewards and 4 important warning signs carefully.

Looking for more investment ideas?

If you stop your research here, you risk missing stocks that might fit your goals even better, so take a moment to scan a few focused shortlists.

- Target dependable income by checking out 12 dividend fortresses that aim to combine higher yields with resilience.

- Hunt for potential bargains by reviewing 47 high quality undervalued stocks built around quality fundamentals and pricing.

- Protect your downside by scanning 70 resilient stocks with low risk scores that screen for sturdier balance sheets and lower overall risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.