Assessing Restaurant Brands International’s Valuation After Recent Choppy Share Price Performance

Restaurant Brands International, Inc. QSR | 76.58 | +1.97% |

Why Restaurant Brands International Is On Investors’ Radar

Restaurant Brands International (QSR) has drawn interest after recent share price moves, with the stock showing mixed short term returns while maintaining a positive trend over the past 3 years and 5 years.

Recent trading has been choppy, with a 7 day share price return of 1.41% decline and a 90 day share price return of 1.68% gain. However, the 1 year total shareholder return of 15.62% points to steadier long term momentum supported by dividends.

If QSR has you thinking about where else capital might work for you next, it could be a good time to broaden your search with fast growing stocks with high insider ownership.

With Restaurant Brands International trading at $68.55 and sitting at roughly a 16% discount to both analyst targets and one intrinsic value estimate, the key question is simple: is this a genuine entry point, or is the market already baking in future growth?

Most Popular Narrative: 13% Undervalued

With Restaurant Brands International at $68.55 versus a narrative fair value near $78, the current gap hinges on how its global growth engine plays out.

Rapid international expansion, particularly through the franchise-led model in markets such as China, India, Turkey, Japan, and Brazil, is driving double-digit unit and system-wide sales growth; this directly supports recurring, capital-light revenue streams and higher long-term earnings visibility.

Population growth, urbanization, and rising middle-class consumer bases in emerging markets are expanding RBI's addressable customer base and supporting the return to net restaurant growth (notably at Tim Hortons in Canada and new Firehouse and Popeyes units in fast-growing geographies), structurally underpinning future revenue and profit growth.

Want to see what revenue, earnings, and profit margin path needs to unfold for that $78 handle to make sense? The most followed narrative leans on steady expansion, richer margins, and a valuation multiple that assumes the growth story keeps compounding. Curious which specific long term forecasts are baked into that fair value?

Result: Fair Value of $78.45 (UNDERVALUED)

However, stubborn cost inflation and any stumble in international expansion, such as issues in China or France, could quickly put pressure on the current undervaluation story.

Another Angle On The Valuation

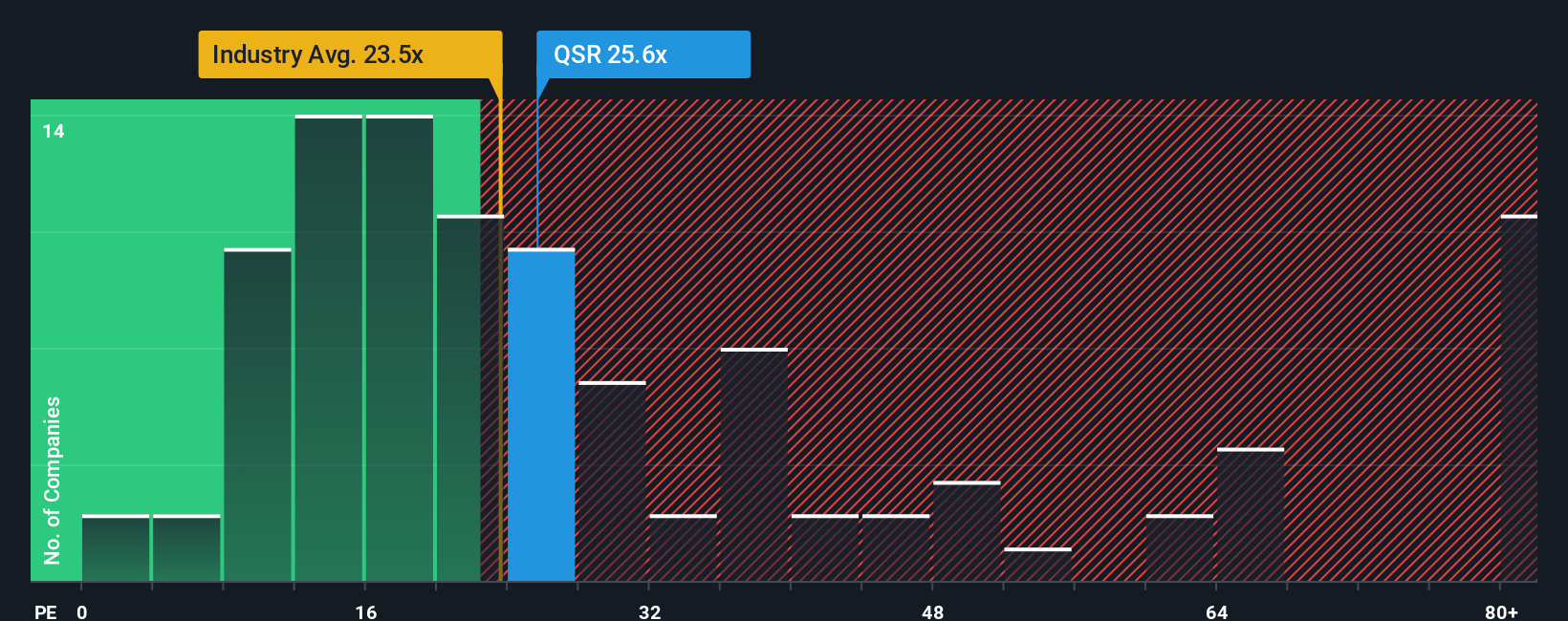

The earlier fair value work points to QSR looking undervalued, but the earnings multiple sends a cooler message. At about 24.2x P/E, QSR trades above the US Hospitality average of 21.4x, yet below its own fair ratio of 28.1x. This combination hints at both support and valuation risk. Which signal do you trust more at today’s price?

Build Your Own Restaurant Brands International Narrative

If these numbers or assumptions do not quite line up with your view, you can stress test the data yourself and shape a narrative that fits your outlook with Do it your way.

A great starting point for your Restaurant Brands International research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you are serious about compounding your wealth, do not stop at one stock idea. Use powerful screeners to surface opportunities you might otherwise miss.

- Spot potential value opportunities early by scanning these 875 undervalued stocks based on cash flows that line up with your return expectations and risk comfort.

- Ride major technology shifts by checking out these 24 AI penny stocks shaping real world applications of artificial intelligence.

- Turn income goals into a focused watchlist by filtering for these 12 dividend stocks with yields > 3% that may suit a yield oriented approach.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.