Assessing Rivian (RIVN) Valuation After R2 Launch Uber Robotaxi Deal And Volkswagen Investment

Rivian Automotive RIVN | 0.00 |

Rivian Automotive (RIVN) is back in focus after the official launch and first customer deliveries of its R2 electric SUV, supported by fresh tie ups with Uber and Volkswagen that broaden its reach.

Even after the R2 launch, fresh partnerships with Uber and Volkswagen, and a safety review into rear suspension toe links, the stock remains volatile. It has a 1 month share price return of 10.62% but a year to date share price decline of 18.96%, while the 1 year total shareholder return is 9.24%, hinting at momentum that has been uneven across timeframes.

If this kind of EV story has your attention, it can be useful to widen the lens and scan other electrification plays through our 34 power grid technology and infrastructure stocks

So with RIVN up 10.62% over the past month but still down 18.96% year to date, and trading at a 15% discount to the average analyst target with a reported 48% intrinsic discount, is there still a buying opportunity here, or is future growth already priced in?

Most Popular Narrative: 13.4% Undervalued

Rivian Automotive’s most followed valuation framework puts fair value at $18.15 per share versus the last close at $15.73. This frames the stock as trading below that narrative fair value while investors weigh execution risks and sector sentiment.

The launch of the R2 platform represents a step-change improvement in Rivian's cost structure, with management securing supplier contracts and component sourcing that reduce bill of materials by nearly 50% versus R1, significantly lowering per-unit costs, this operational overhaul is expected to improve gross margins and path to profitability as scale is achieved.

It raises the question of what kind of revenue ramp and margin shift would need to sit behind that cost reset for the numbers to add up. The most followed narrative leans on brisk top line growth, a gradual move toward positive earnings, and a future profit multiple more often seen in higher growth sectors. Readers may want to see exactly how those assumptions stack together and what discount rate is used to pull that $18.15 figure back into today’s dollars.

Result: Fair Value of $18.15 (UNDERVALUED)

However, this depends on keeping cash burn and capital needs in check, and on R2 demand meeting expectations in a crowded midsize SUV EV segment.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another View: Revenue Multiple Sends a Different Signal

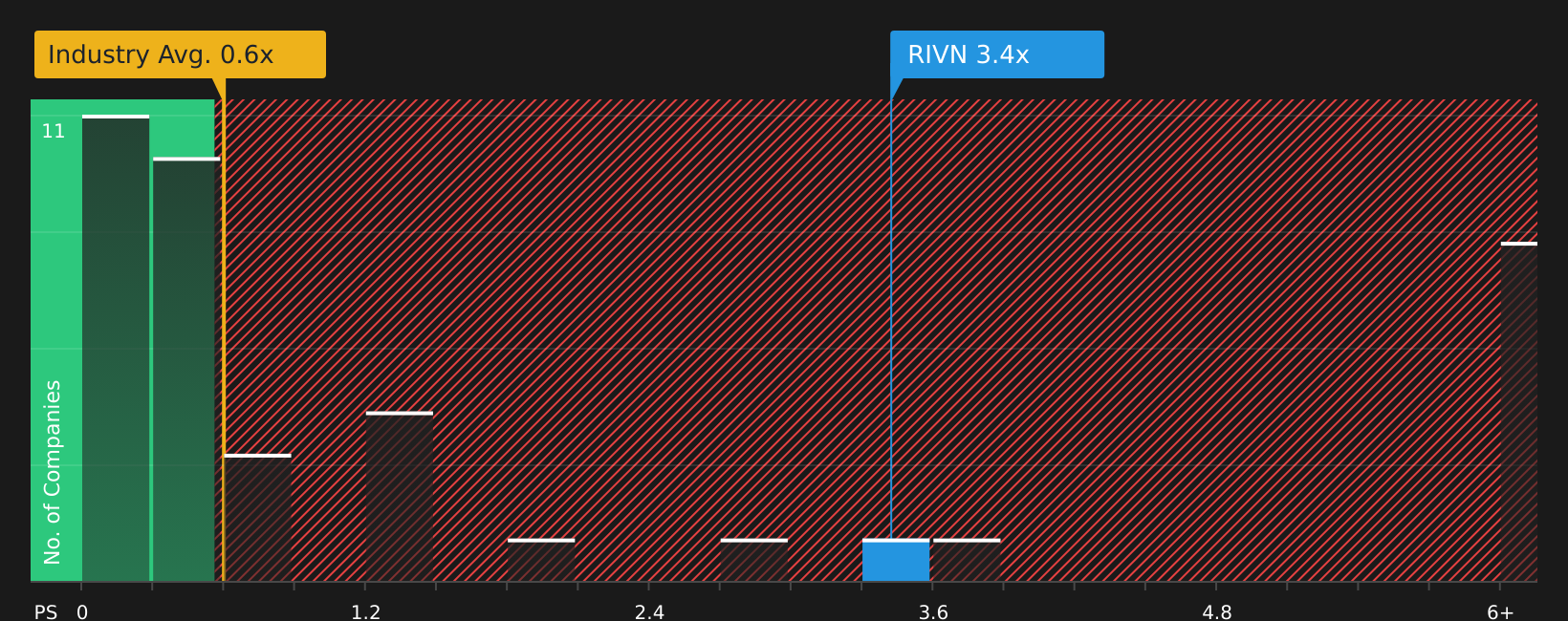

While the analyst narrative frames RIVN as 13.4% undervalued versus an $18.15 fair value, the revenue multiple paints a tougher picture. The stock trades on a P/S of 3.6x, compared with 0.6x for the US Auto industry and 0.9x for peers, and above an estimated fair ratio of 1.9x. That gap suggests investors are already paying a premium for future growth that is not yet profitable. How comfortable are you with that trade off?

Next Steps

With mixed signals on value and expectations, it helps to move fast, look at the underlying data, and decide where you stand. To see how the positives and concerns balance out, review the 2 key rewards and 1 important warning sign

Looking for more investment ideas?

If RIVN has sharpened your focus, do not stop here. Broaden your watchlist now or you risk missing other opportunities sitting in plain sight.

- Spot potential mispricings early by scanning 46 high quality undervalued stocks that combine solid fundamentals with room for sentiment to catch up.

- Secure more predictable cash flows by reviewing companies in the 9 dividend fortresses that may help anchor your portfolio with regular income.

- Strengthen your downside protection by checking the 63 resilient stocks with low risk scores that screen for resilient balance sheets and steadier risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.