Assessing RLX Technology (NYSE:RLX) Valuation After Improved Operations Under High Debt Concerns

RLX Technology, Inc. Sponsored ADR RLX | 2.19 | 0.00% |

Why RLX Technology Is Back on Investors’ Radar

RLX Technology (RLX) has come into focus after shifting to positive operating performance while still carrying what many see as high debt and leverage, a mix that naturally draws attention from risk aware investors.

At a share price of $2.39, RLX Technology’s 7.17% 1 month share price return and 3.02% year to date share price return contrast with a far weaker 5 year total shareholder return of an 89.48% decline. This suggests that recent momentum is building after a very difficult longer period.

If this shift in sentiment has you looking beyond a single name, it could be a good moment to check out 23 top founder-led companies as potential new ideas for your watchlist.

With annual revenue of CN¥3,272.659 and net income of CN¥764.281, alongside an indicated intrinsic discount of 74.25%, the key question is whether RLX is genuinely undervalued or if the market already prices in future growth.

Most Popular Narrative: 21.5% Undervalued

The most followed narrative puts RLX Technology’s fair value at $3.04, comfortably above the recent $2.39 share price, and anchors that view in a specific roadmap for revenue, margins, and valuation multiples.

The ongoing global shift from traditional cigarettes to reduced-risk products, such as e-vapor and oral nicotine, is growing the overall nicotine alternatives market; RLX's leadership and early move into multi-category offerings position it to capture expanding consumer demand, supporting strong long-term revenue growth.

Rising international health consciousness and regulatory efforts against smoking are accelerating consumer adoption of smokeless and electronic delivery systems; RLX's international expansion and compliance-focused portfolio are poised to benefit from increased user base and higher penetration, likely driving revenue and earnings growth through new market access.

Want to see what is behind that fair value gap? The narrative leans heavily on fast compounding revenue, shifting profit margins, and a future earnings multiple that assumes investors still pay up for growth. Curious which specific assumptions have to hold for that $3.04 figure to make sense, and how much earnings power is being pencilled in over the next few years?

Result: Fair Value of $3.04 (UNDERVALUED)

However, the story could break if China’s large illegal e-vapor market keeps pressuring prices, or if tighter regulation increases compliance costs and squeezes margins.

Another Angle on Valuation

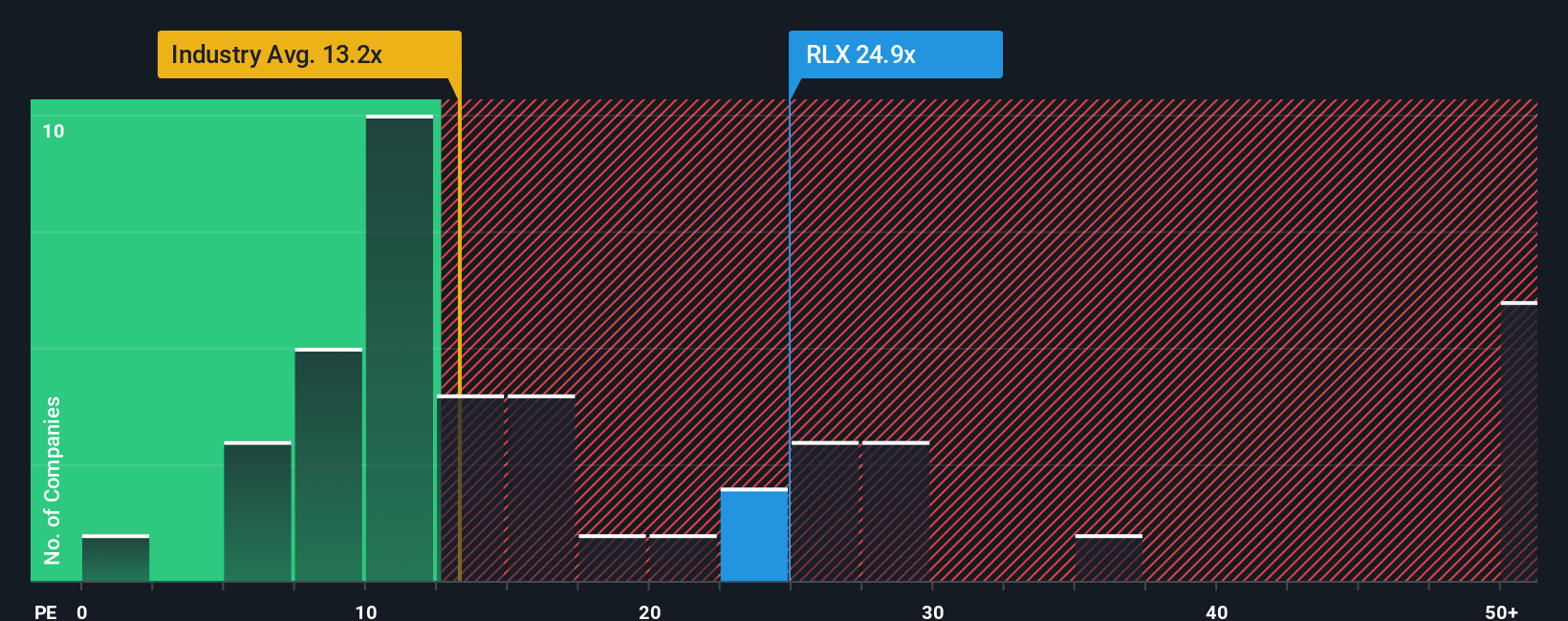

The narrative says RLX Technology looks undervalued, but its current P/E of 26.3x tells a tougher story. That is higher than the global tobacco average of 14.7x and also above its own fair ratio of 21.8x, even though it sits below the peer average of 35.2x. In practice, you are paying a premium that the wider industry does not, so the question is whether that premium feels earned to you.

Build Your Own RLX Technology Narrative

If you see the numbers differently, or prefer to test your own assumptions against the data, you can build a custom thesis in minutes by starting with Do it your way.

A great starting point for your RLX Technology research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If you are serious about building a stronger portfolio, do not stop at a single stock. Use focused screeners to surface ideas you might otherwise miss.

- Spot potential mispricings early by checking companies that appear cheap on quality metrics with 51 high quality undervalued stocks before others catch on.

- Aim for staying power in tougher markets by searching for companies with strong finances using our solid balance sheet and fundamentals stocks screener (45 results).

- Hunt for off the radar opportunities by scanning our screener containing 24 high quality undiscovered gems that combine fundamentals with lower market attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.