Assessing Sable Offshore (SOC) Valuation After Defense Production Act Scrutiny And Refinancing Uncertainty

Sable Offshore SOC | 0.00 |

Lawmakers have formally questioned Sable Offshore (SOC) over its use of the Defense Production Act to restart oil production off the Santa Barbara coast. This has raised investor concerns around future hydrocarbon transport, sales, and refinancing plans.

The stock has sold off sharply in the short term, with a 1-day share price decline of 9.53% and a 7-day drop of 16.38% as the Defense Production Act scrutiny and pipeline uncertainty weighed on sentiment. The 1-year total shareholder return is down 50% despite positive 3 and 5-year total shareholder returns.

If this kind of regulatory shake-up has you reassessing your energy exposure, it may be a good moment to look at other producers through our 33 elite gold producer stocks

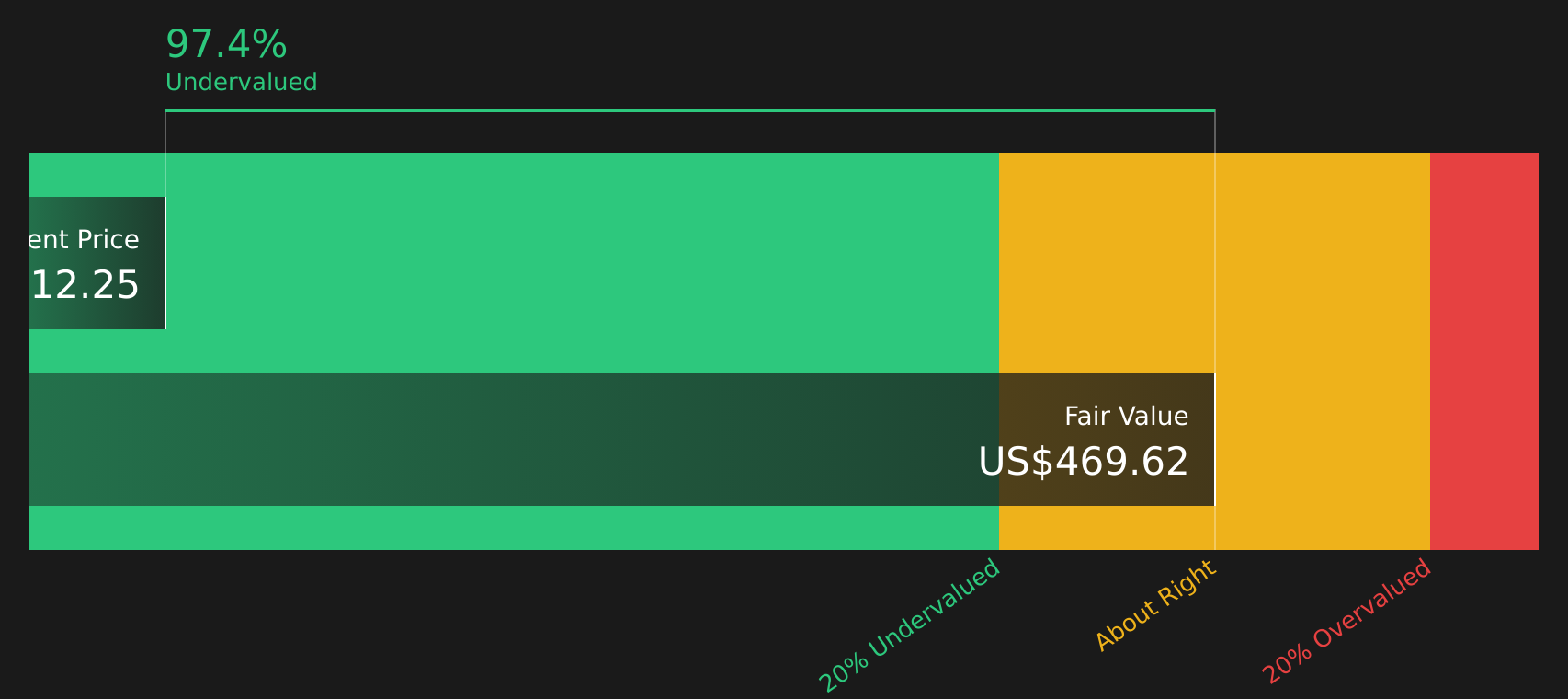

With Sable Offshore trading at $12.25 and sitting at what looks like a steep discount to a $27.00 analyst target and a reported intrinsic value gap, you have to ask: is this a reset opportunity, or is the market already bracing for weaker growth?

Preferred Price-to-Book of 4.5x: Is it justified?

On simple valuation checks, Sable Offshore screens as cheap versus a selected peer set but expensive versus the wider US Oil and Gas industry, which sends a mixed signal at $12.25.

The key lens here is the P/B ratio, which compares the stock price to the accounting book value of equity. For Sable Offshore, that ratio sits at 4.5x. Against a peer group average of 41.5x it looks low, suggesting the market is assigning a smaller premium to its asset base than to some direct comparables. That sits alongside statements that the stock is trading at 97.4% below one internal fair value estimate and below an SWS DCF model cash flow value of $469.62 per share.

However, compared with the broader US Oil and Gas industry P/B average of 1.6x, Sable Offshore’s 4.5x looks punchy. That gap implies investors are paying a higher price for each dollar of book value than they are for the sector overall. This may reflect expectations tied to its offshore California assets, forecast revenue growth and the use of higher risk funding sources such as external borrowing. If those factors do not play out as hoped, the premium to the sector could compress.

Result: Price-to-book of 4.5x (OVERVALUED)

However, regulatory scrutiny of the Defense Production Act use, along with the company’s reported net loss of $497.644 million, could quickly change how that premium is viewed.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another View: SWS DCF Signals Deep Undervaluation

Price to book paints Sable Offshore as expensive next to the wider US Oil and Gas sector, but the SWS DCF model tells a very different story. At $12.25 versus an estimated future cash flow value of $469.62 per share, the implied discount is extremely large. Is the model too optimistic, or is sentiment too pessimistic?

For a closer look at how that cash flow estimate is built, and to judge the assumptions for yourself, Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Sable Offshore for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 49 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment clearly split between deep value signals and clear governance concerns, it makes sense to move quickly and test the data yourself, then weigh up 2 key rewards and 5 important warning signs

Looking for more investment ideas?

If Sable Offshore has sharpened your focus, do not stop here. Widen your watchlist with other stocks that match clear, data driven criteria.

- Target potential upside with companies that combine quality metrics and discounted valuations through our 49 high quality undervalued stocks.

- Lock in steadier cashflows by reviewing income focused opportunities using the 9 dividend fortresses.

- Prioritise resilience by scanning companies with stronger finances via the 64 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.