Assessing Sandisk (SNDK) Valuation As AI-Driven NAND Demand And SSD Price Increases Take Hold

Sandisk Corporation SNDK | 0.00 |

Sandisk (SNDK) is back in the spotlight as AI driven demand for NAND flash runs into tight supply, with the company lifting prices on high capacity enterprise SSDs while analyst upgrades continue to accumulate.

Those price hikes and analyst upgrades come after a powerful run in the stock. The 30 day share price return is about 100% and the 90 day share price return is close to 200%. Year to date momentum remains strong off a US$413.62 last close. This indicates that recent gains have been concentrated in the short term rather than spread evenly across the year.

If Sandisk’s rally has you looking beyond a single name, this could be a useful moment to scan other storage and chip beneficiaries in high growth tech and AI stocks for fresh ideas.

So with Sandisk trading around US$413.62 after a very sharp recent run, are you looking at a stock that still offers mispriced upside, or is the market already baking in several years of future growth?

Price to Sales of 7.8x: Is it justified?

On roughly US$7.8b of revenue, Sandisk trades on a P/S of 7.8x, which is well above both peers and broader US tech at the last close of US$413.62.

The P/S ratio compares the company’s market value to its revenue, so at 7.8x investors are paying several times Sandisk’s annual sales for exposure to its NAND flash and storage business.

That might reflect expectations around forecast earnings growth of 57.18% per year and revenue growth of 17.3% per year, even though the company currently reports a net loss of US$1.74b and remains unprofitable.

Against that backdrop, the US tech industry sits on a P/S of 1.9x and Sandisk’s peer group averages 4.1x. The estimated fair P/S ratio for the company is 3.9x, which is roughly half the current multiple and a level the market could move towards if sentiment cools.

Result: Price-to-sales of 7.8x (OVERVALUED)

However, there are clear pressure points here, including Sandisk’s US$1.74b net loss, and a share price that currently sits above the average analyst target.

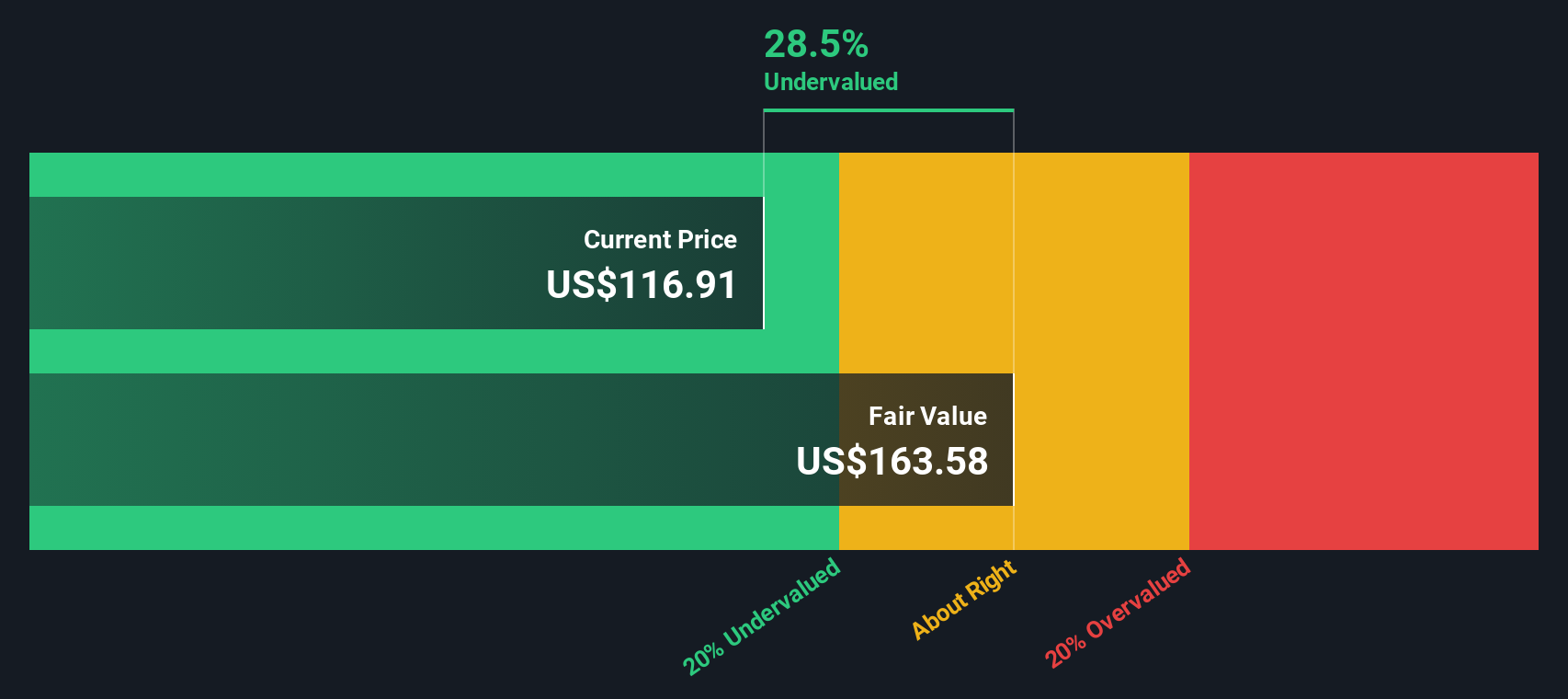

Another view on value

Our SWS DCF model points to a fair value of about US$404.71 per share, which is slightly below the current US$413.62 price. That is a much milder gap than the P/S signal, so it raises a simple question: is the real risk here valuation, or execution?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Sandisk for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 871 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Sandisk Narrative

If you look at the numbers and come to a different conclusion, or simply prefer building your own view from scratch, you can put together a custom Sandisk thesis in just a few minutes with Do it your way.

A great starting point for your Sandisk research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Sandisk has sharpened your interest, do not stop there. Broaden your watchlist now so you are not late to the next opportunity.

- Spot potential income payers early by scanning these 12 dividend stocks with yields > 3%, which could help anchor a more income focused portfolio.

- Hunt for growth stories by checking out these 24 AI penny stocks that tie into long term automation and machine learning themes.

- Stay ahead of emerging trends by tracking these 80 cryptocurrency and blockchain stocks linked to blockchain, tokenization and digital asset infrastructure.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.