Assessing Scotts Miracle-Gro (SMG) Valuation As Miracle-Gro Expands Indoor Gardening Product Line

Scotts Miracle-Gro Company Class A SMG | 63.88 | +4.70% |

Scotts Miracle-Gro (SMG) is back in focus after its Miracle-Gro brand rolled out a refreshed indoor product lineup, expanding soils, plant foods and pest solutions tied to growing interest in indoor gardening and self-care.

The refreshed Miracle-Gro indoor range lands at a time when Scotts Miracle-Gro’s short term momentum is picking up, with a 30 day share price return of 9.46% and a year to date share price return of 13.07%, set against a 5 year total shareholder return of a 66.51% decline.

If this indoor gardening push has you thinking more broadly about where growth stories can come from, it could be a good moment to check out 22 top founder-led companies as another way to surface potential ideas.

With shares up 15.1% over 90 days but still showing a 66.51% total return decline over five years, and trading at a 7.2% discount to one intrinsic value estimate, is there genuine upside here, or is the market already baking in future growth?

Most Popular Narrative: 6% Undervalued

Scotts Miracle-Gro’s most followed valuation story pegs fair value at $71.5 versus the last close at $67.2, pointing to modest upside built on profitability improvement and cash generation.

Significant ongoing investments in supply chain technology, automation, and process efficiencies are unlocking ~$75 million in cost savings for fiscal '25 and another ~$75 million planned for '26/'27. These savings directly support gross margin recovery (aiming for 35%+), boost EBITDA, and improve long-term net margins.

Curious how a relatively cautious revenue outlook can still back a higher fair value than today’s price? The narrative leans heavily on margin rebuild, earnings power, and a future earnings multiple that has to compress meaningfully over time. The exact mix of growth, profitability and discount rate doing the heavy lifting might surprise you.

Result: Fair Value of $71.5 (UNDERVALUED)

However, this hinges on several things going right, and weather driven demand swings or tighter environmental rules could quickly challenge those margin and earnings assumptions.

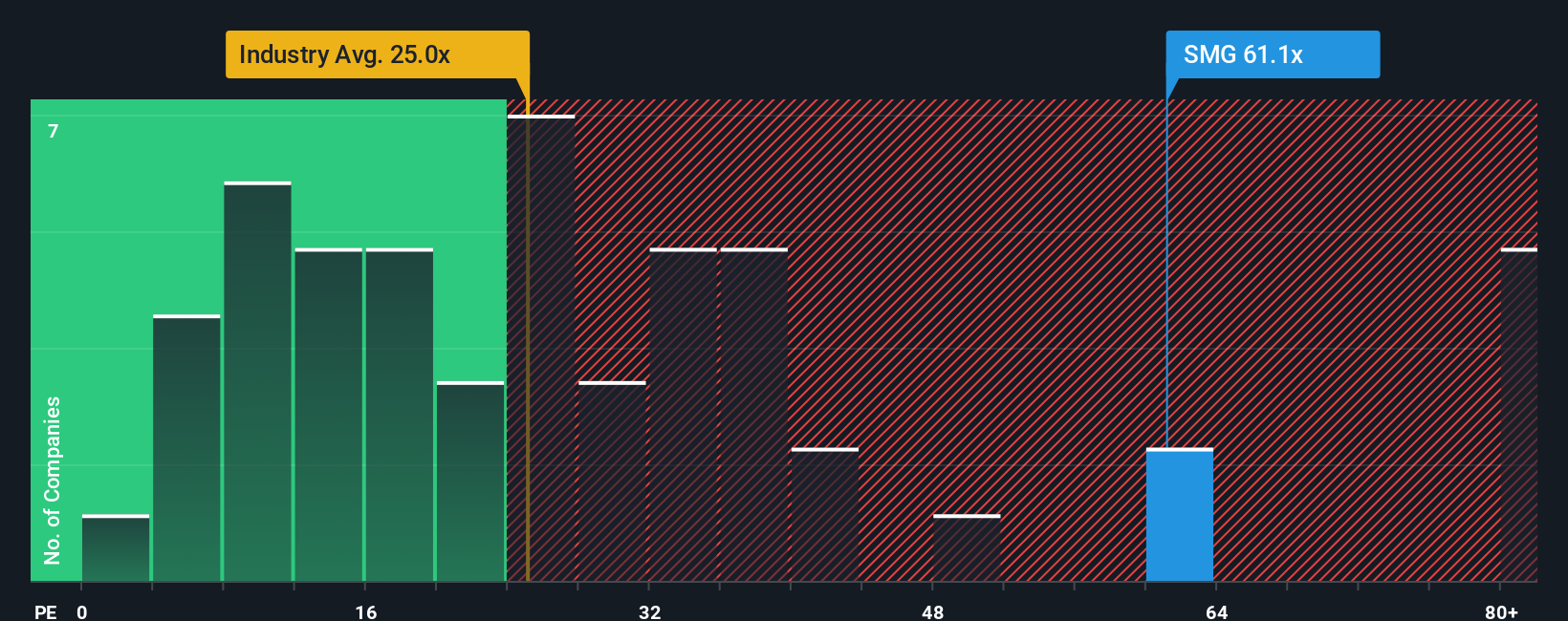

Another Angle: P/E Ratios Send A Different Signal

While the narrative suggests Scotts Miracle-Gro is modestly undervalued, the P/E story is less generous. At 23.9x, the current P/E is above the 23.2x fair ratio and well above the 12.1x peer average, even though it sits below the 26.6x US Chemicals industry average. That gap points to some valuation risk, so you have to ask whether the earnings outlook really justifies paying up.

Build Your Own Scotts Miracle-Gro Narrative

If you look at the numbers and come to a different conclusion, or just prefer to trust your own work, you can build a tailored view around your assumptions in just a few minutes: Do it your way

A great starting point for your Scotts Miracle-Gro research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Scotts Miracle-Gro is on your radar but you want a wider watchlist, now is the time to scan for fresh opportunities before the crowd catches up.

- Target stability with income potential by checking out 13 dividend fortresses that could add reliable cash flow to your portfolio.

- Hunt for quality at a sensible entry point by reviewing 51 high quality undervalued stocks that line up strong fundamentals with pricing that still looks reasonable.

- Spot resilient candidates that may help smooth portfolio swings by scanning 85 resilient stocks with low risk scores before the market pays closer attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.