Assessing Seagate Technology Holdings (STX) Valuation After Robust Q2 Earnings And Fresh Revenue Guidance

Seagate Technology Holdings PLC STX | 0.00 |

Seagate Technology Holdings (STX) is back in focus after reporting second quarter results that detail sales of US$2,825 million and net income of US$593 million, alongside fresh revenue guidance for the coming quarter.

At a share price of US$425.00, Seagate has seen short term softness, with a 1 day share price return of 1.01% decline and a 7 day share price return of 1.84% decline. However, recent earnings, dividend affirmation and the new shelf registration sit against a sharp 39.8% 30 day and 47.6% 90 day share price return, and a very large 1 year total shareholder return, suggesting strong momentum that investors are now reassessing in light of fresh guidance and capital plans.

If this earnings update has you looking beyond a single name, it could be a good time to see which other storage and data hardware players are screening well in our 33 AI infrastructure stocks.

With Seagate trading at US$425.00 alongside solid recent earnings, a long running buyback program and fresh shelf capacity, is the current valuation still leaving upside on the table, or is the market already pricing in future growth?

Most Popular Narrative: 43.1% Overvalued

Against the last close at $425.00, the most followed narrative pegs Seagate’s fair value at about $297 per share, creating a wide gap investors will want to understand.

Analysts have nudged their fair value estimate for Seagate Technology Holdings higher to approximately $297 per share from about $289, citing sustained HDD pricing power, structurally stronger nearline demand tied to AI infrastructure, and a higher expected earnings multiple supported by disciplined capacity additions and accelerating HAMR adoption.

Curious what earnings path and margin profile could justify that $297 figure, especially with AI data growth and HAMR rollout in the mix? The narrative leans on specific revenue assumptions, profitability levels and a particular future earnings multiple that together pull the value well below today’s price, but you only see how it all fits once you read it in full.

Result: Fair Value of $297 (OVERVALUED)

However, that story could change quickly if trade policy shifts alter customer orders, or if SSD and QLC NAND pressure HDD demand more than analysts currently expect.

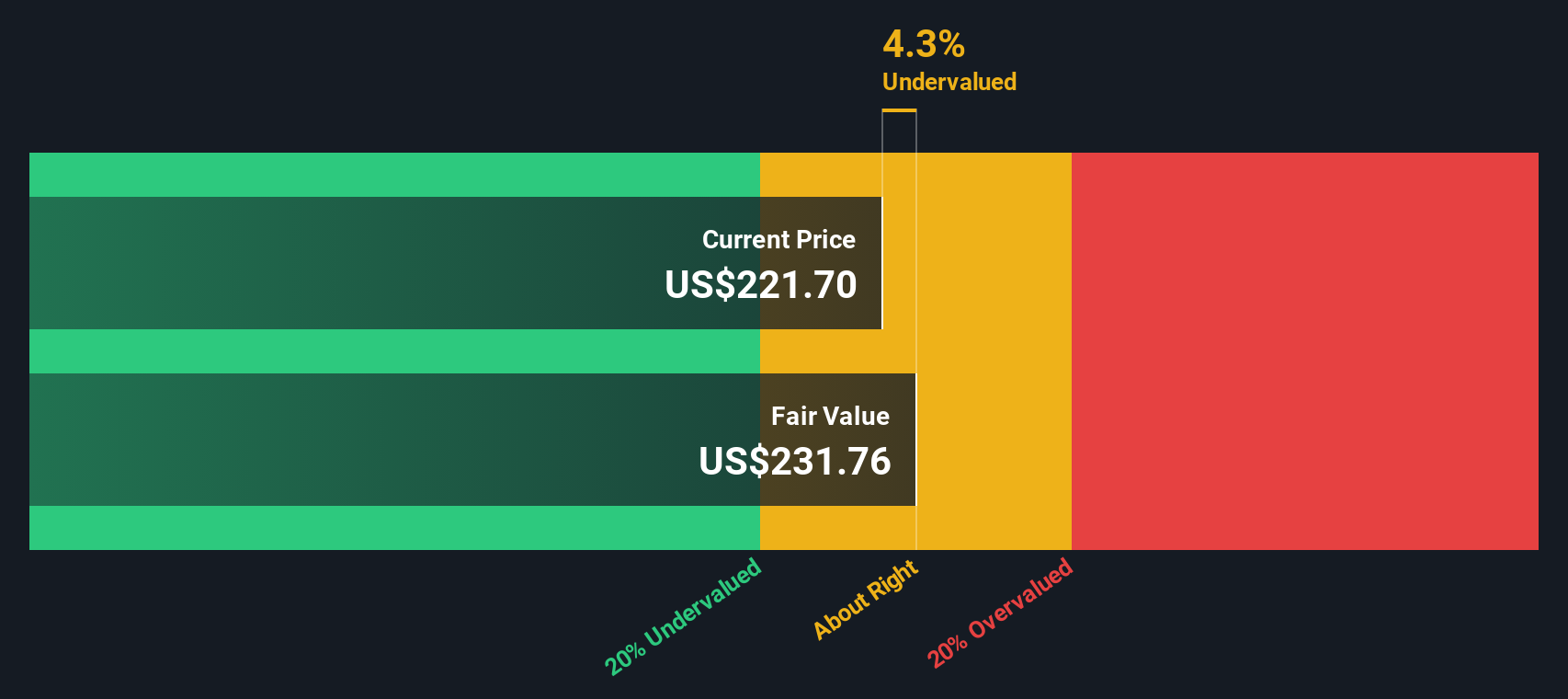

Another Lens on Value: SWS DCF Model

The narrative based on fair value at $297 suggests Seagate is 43.1% overvalued at $425, but our DCF model points in the opposite direction. Using projected cash flows, it indicates fair value around $613 per share, which implies Seagate is trading at a 30.7% discount. Which story appears more compelling?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Seagate Technology Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 52 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Seagate Technology Holdings Narrative

If you see the numbers differently or prefer to work from your own assumptions, you can build a personalised Seagate view in just a few minutes: Do it your way.

A great starting point for your Seagate Technology Holdings research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Seagate has sharpened your focus on quality, now is a smart moment to widen the net and line up a few more ideas on your watchlist.

- Capture potential mispricing by scanning our list of 52 high quality undervalued stocks that pair quality fundamentals with prices some investors may be overlooking.

- Strengthen your income stream by checking out 14 dividend fortresses that prioritize substantial yields alongside resilience.

- Sleep a little easier by reviewing 82 resilient stocks with low risk scores that score well on stability and lower overall risk.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.