Assessing Shift4 Payments (FOUR) Valuation After Governance Overhaul And TRA Exit

Shift4 Payments FOUR | 42.76 | +0.35% |

Shift4 Payments (FOUR) has overhauled its capital structure by collapsing multiple share classes into a single Class A share and removing super-voting rights, while also exiting substantial future tax receivable agreement obligations.

Despite the governance clean up and TRA exit, recent share price returns have been weak, with a 30 day share price return of 10.48% and a 1 year total shareholder return of 49.72%. This hints that sentiment has cooled even as investors reassess long term cash flow visibility.

If this kind of corporate reset has you thinking about where else ownership and governance matter, it could be a good time to look at our 22 top founder-led companies.

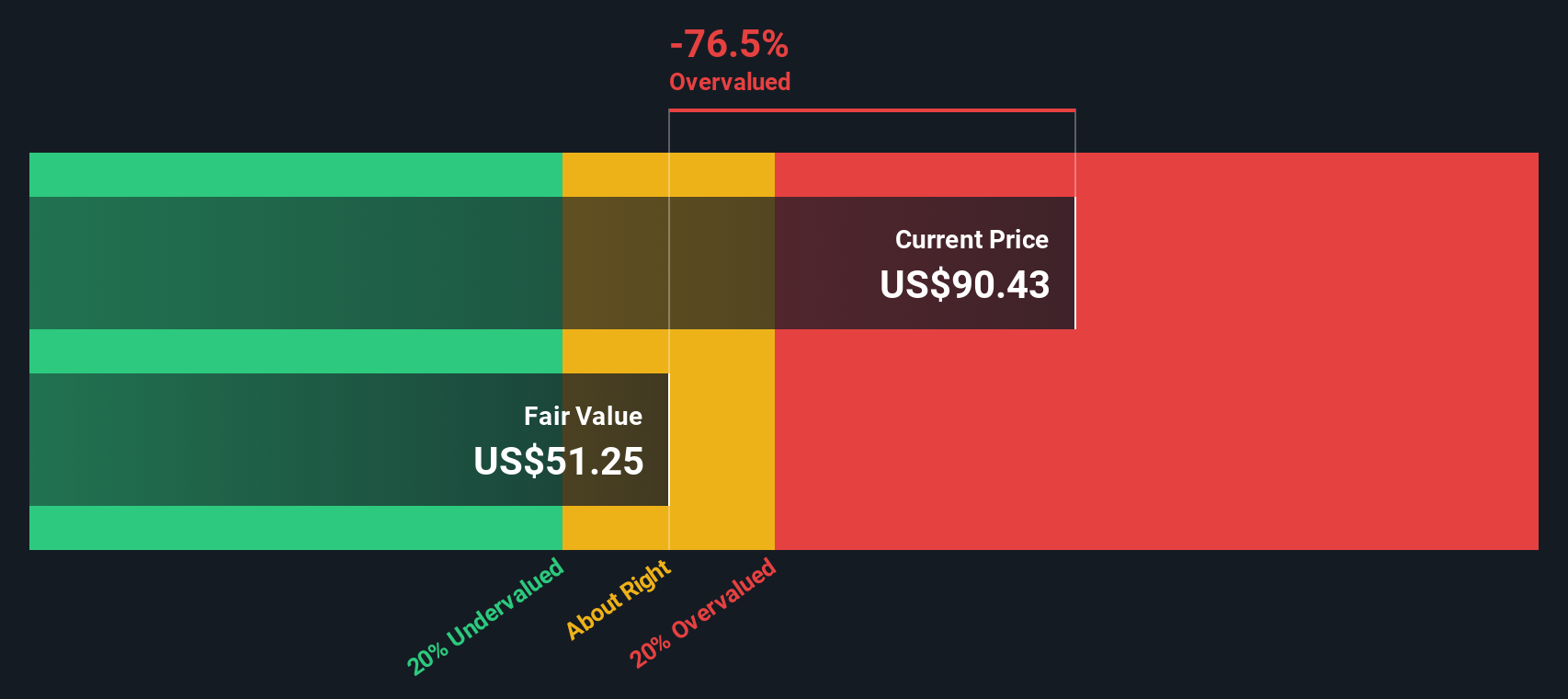

With returns over 1 year and 3 years both negative and the shares trading at US$58.74 against an analyst price target of US$88.83, is Shift4 now mispriced, or is the market already accounting for potential future growth?

Most Popular Narrative: 38.7% Undervalued

Simply Wall St's most followed narrative puts Shift4 Payments' fair value at $95.86 versus the last close of $58.74, and ties that gap to a detailed view of future growth, profitability and required returns using an 8.93% discount rate.

The cross sell opportunity across the combined customer bases of newly acquired companies (for example, bringing Shift4's payment products into Global Blue's luxury retail clients, or introducing Global Blue's DCC product to Shift4 hotels/restaurants) creates a substantial embedded pipeline for incremental revenue and sustained organic growth over multiple years.

Want to see what sits behind that fair value gap? The narrative leans on fast building earnings, firm revenue expectations and a future profit multiple that assumes investors stay confident. Curious which exact growth and margin paths have been baked into those numbers, and how sensitive that valuation is to even small changes in those assumptions? The full story is in the model behind that $95.86.

Result: Fair Value of $95.86 (UNDERVALUED)

However, those long term hopes could be derailed if recent acquisitions prove hard to integrate, or if hospitality and restaurant volumes stay softer than analysts currently assume.

Another Take: DCF Comes Out More Cautious

While the popular narrative points to a fair value of $95.86 and calls the shares undervalued, our DCF model is more restrained. It puts fair value at $55.34, slightly below the current $58.74 price, which suggests limited upside on this view. Which lens do you trust more?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Shift4 Payments for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Shift4 Payments Narrative

If you look at the numbers and come to a different conclusion, or simply prefer to test your own assumptions, you can pull the data together and build your version of the Shift4 story in just a few minutes, then Do it your way.

A great starting point for your Shift4 Payments research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Shift4 has opened your eyes to how much story and structure matter, do not stop here. Widen your lens and test a few more angles.

- Target quality at a discount by checking companies our screener flags as 51 high quality undervalued stocks with strong fundamentals already in place.

- Prioritize resilience and sleep better at night by scanning the 85 resilient stocks with low risk scores that score well on our risk checks.

- Get ahead of the crowd by reviewing our screener containing 24 high quality undiscovered gems where solid numbers have not yet attracted broad attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.