Assessing Silicon Labs (SLAB) Valuation After CES 2026 IoT And Security Showcases

Silicon Laboratories Inc. SLAB | 209.13 | +0.68% |

Why CES 2026 and security leadership matter for Silicon Laboratories (SLAB)

Silicon Laboratories (SLAB) is in focus after using CES 2026 to spotlight its IoT product portfolio and the new Simplicity SDK for Zephyr, while also appointing Ian N. Dawson as Chief Information Security Officer.

The CES showcase puts the company’s role in secure, scalable and energy efficient connected devices front and center, and the CISO hire highlights how management is treating cybersecurity, IP protection and long term product resilience as core parts of the investment story.

Those CES announcements come at a time when momentum in the stock has been picking up, with a 30 day share price return of 10.78% and a year to date share price return of 12.98%. The 1 year total shareholder return of 8.31% contrasts with a broadly flat 3 year total shareholder return of 0.64%, suggesting that recent enthusiasm is building on a more muted longer run.

If you are looking beyond Silicon Laboratories and want to see what else is happening across connected tech, it could be worth scanning high growth tech and AI stocks as a next step.

With CES buzz, a new CISO and recent share price gains, Silicon Laboratories now sits close to the average analyst price target. Is there still mispricing here, or is the market already baking in future growth?

Most Popular Narrative: 1% Undervalued

With Silicon Laboratories last closing at US$149.05 against a most popular narrative fair value of about US$150.44, the current pricing sits almost on top of that estimate, which hinges on specific growth, margin and valuation assumptions running out to 2028.

Ongoing rollout of new, highly integrated, energy efficient wireless platforms (Series 2 and Series 3) positions Silicon Labs to capture increased market share and supports higher ASPs, which is likely to drive top line growth and gross margin improvement.

Want to see why revenue, margins and a future earnings multiple all need to line up so precisely here? The core story relies on strong top line growth, a swing from losses to profits and a valuation multiple that sits far above typical industry levels. Curious how those ingredients combine to back into this fair value?

Result: Fair Value of $150.44 (ABOUT RIGHT)

However, there are still real pressure points here, including tougher wireless IoT competition and the risk that large device makers increasingly design chips in house.

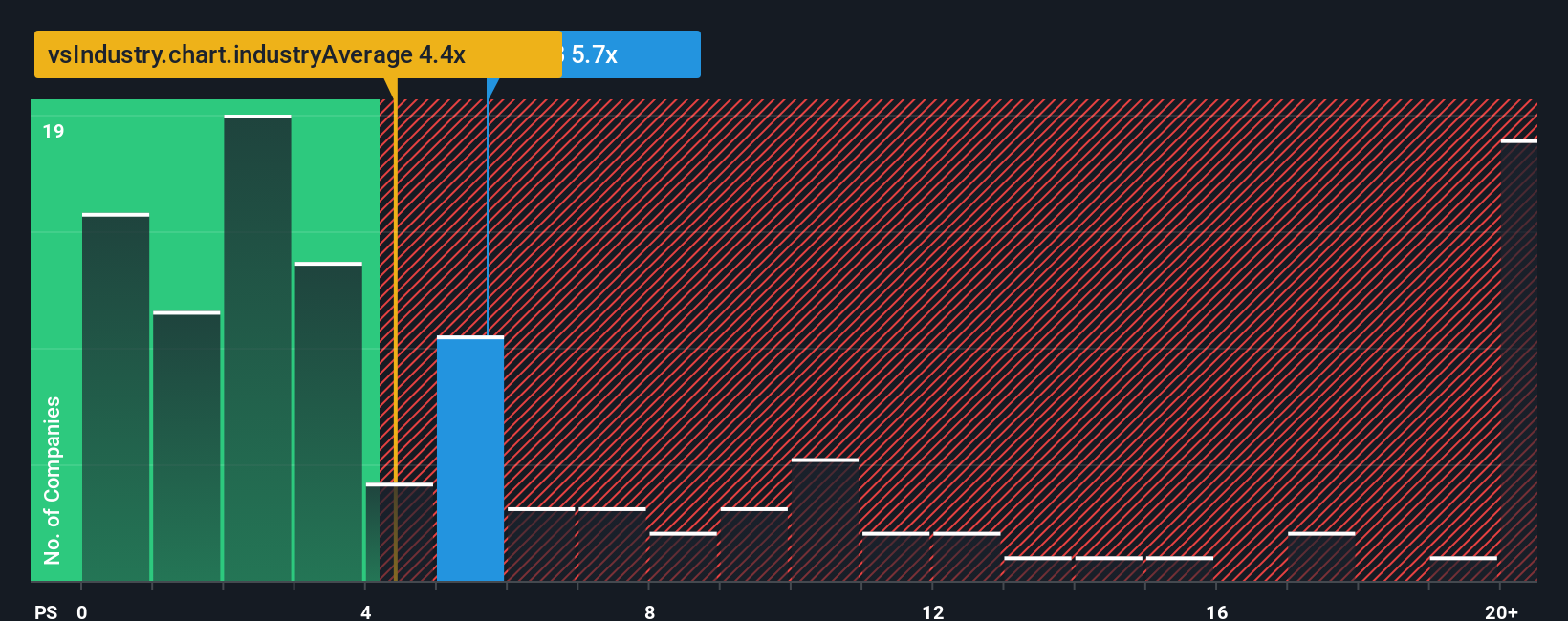

Another View: What the P/S Ratio Is Saying

The analyst narrative points to a fair value close to where Silicon Laboratories trades today, but the market is telling a different story. On a P/S of 6.6x versus peers at 4.3x and a fair ratio of 5.2x, the shares look expensive. Is recent optimism already priced in?

Build Your Own Silicon Laboratories Narrative

If you see the numbers differently or prefer to stress test the assumptions yourself, you can spin up your own version in minutes: Do it your way.

A good starting point is our analysis highlighting 1 key reward investors are optimistic about regarding Silicon Laboratories.

Looking for more investment ideas?

If Silicon Laboratories has caught your interest, do not stop here; use this momentum to broaden your watchlist and pressure test your thinking across different types of opportunities.

- Target potential mispricing by scanning these 886 undervalued stocks based on cash flows that may offer more attractive entry points than what you see in widely followed names.

- Tap into the AI trend with these 25 AI penny stocks that connect real business models to this theme instead of relying only on headlines.

- Hunt for higher income potential through these 12 dividend stocks with yields > 3% that might complement growth focused positions in your portfolio.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.