Assessing Snowflake (SNOW) Valuation After $200 Million OpenAI Partnership And New AI Product Launches

Snowflake SNOW | 151.85 | -0.83% |

Snowflake (SNOW) is back in focus after a multi year, $200 million partnership with OpenAI and a series of AI product launches, including Cortex Code and new semantic automation tools for enterprise customers.

The flurry of AI product launches and the OpenAI deal come against a weak recent trading backdrop, with a 30 day share price return of 33.18% decline and a 1 year total shareholder return of 15.91% loss, suggesting current momentum is fading despite growing attention on Snowflake’s AI push.

If Snowflake’s AI announcements have you thinking more broadly about where data and automation could create value, this is a good moment to look across high growth tech and AI stocks for other potential candidates.

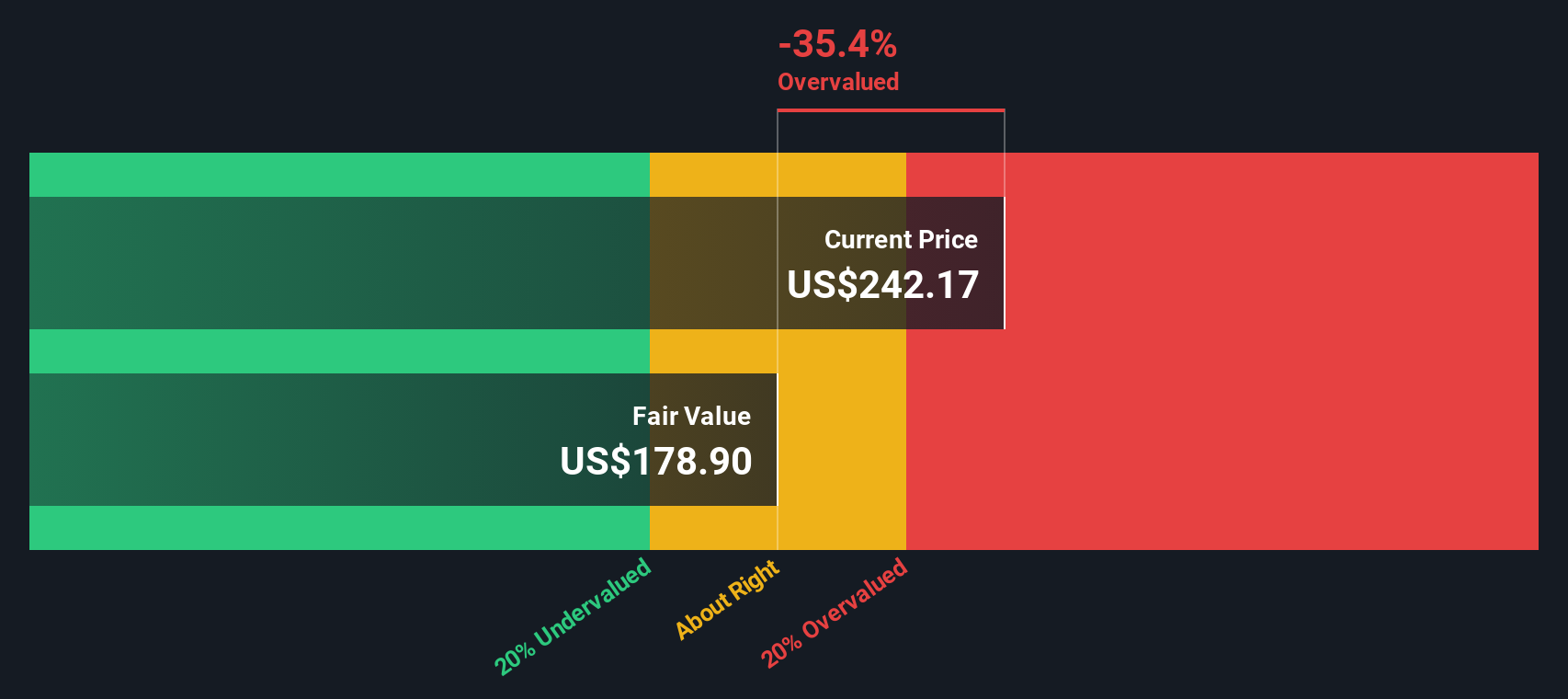

With Snowflake shares down 27.69% year to date and 15.91% over the past year, yet trading at an estimated 22.83% intrinsic discount, you have to ask: is this AI data cloud story on sale, or is the market already baking in the next leg of growth?

Most Popular Narrative: 98.8% Overvalued

Snowflake last closed at $156.71, while the most followed narrative, according to Brogers, places fair value at $78.83, creating a wide gap between story and screen price.

Snowflake represents a bet on two major trends: the continued migration of data to the cloud and the integration of AI into business operations. The company has established a strong position in cloud data warehousing and is making strategic moves to capture AI-driven growth.

Curious how a company with rising revenue, ongoing losses and rich future profit assumptions ends up with a fair value roughly half today’s price? The full narrative lays out the growth path, margin shift and valuation multiple that have to line up for that number to make sense.

Result: Fair Value of $78.83 (OVERVALUED)

However, this story can break if Snowflake struggles to turn its data scale into profits, or if rivals like Databricks capture more AI data budgets.

Another Take on Value

That user narrative points to a fair value of $78.83, which implies Snowflake is 98.8% overvalued. Yet on our numbers, Snowflake at $156.71 trades about 15.6% below the SWS DCF model estimate of future cash flow value. When two methods disagree this much, which story do you trust?

Build Your Own Snowflake Narrative

If that fair value story does not sit right with you, or you prefer to test the numbers yourself, you can build a fresh view in minutes, starting with Do it your way.

A great starting point for your Snowflake research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Snowflake is on your radar, do not stop there. The next set of ideas you shortlist today could shape how your portfolio looks a year from now.

- Scan for potential mispricings by reviewing these 861 undervalued stocks based on cash flows that align with your view on cash flow driven opportunities.

- Zero in on the AI theme by checking out these 30 AI penny stocks that link data, automation and machine learning in different ways to Snowflake.

- Balance growth and income by considering these 11 dividend stocks with yields > 3% that might complement higher risk AI names in your watchlist.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.