Assessing SoundHound AI (SOUN) Valuation After New Voice AI Wins And Rising Investor Interest

SoundHound AI SOUN | 6.97 7.05 | +1.90% +1.15% Pre |

Why SoundHound AI is back on investors’ radar

SoundHound AI (SOUN) is drawing fresh attention after renewing and expanding its relationship with Five Guys, where its voice AI agents have already handled well over a million customer interactions across hundreds of restaurant locations.

At a share price of US$8.56, SoundHound AI has seen a 16.5% 1 day share price return. However, its 30 day and year to date share price returns remain weak, alongside a 45.1% 1 year total shareholder return decline, while the 3 year total shareholder return is a little over double.

If this Five Guys news has you thinking more broadly about voice and automation, it could be worth scanning our screener of 57 profitable AI stocks that aren't just burning cash as potential next ideas.

With the shares still well below their 1 year high and analysts’ average price target sitting at US$16.31 versus a last close of US$8.56, you have to ask: is there a genuine opportunity here, or is the market already pricing in future growth?

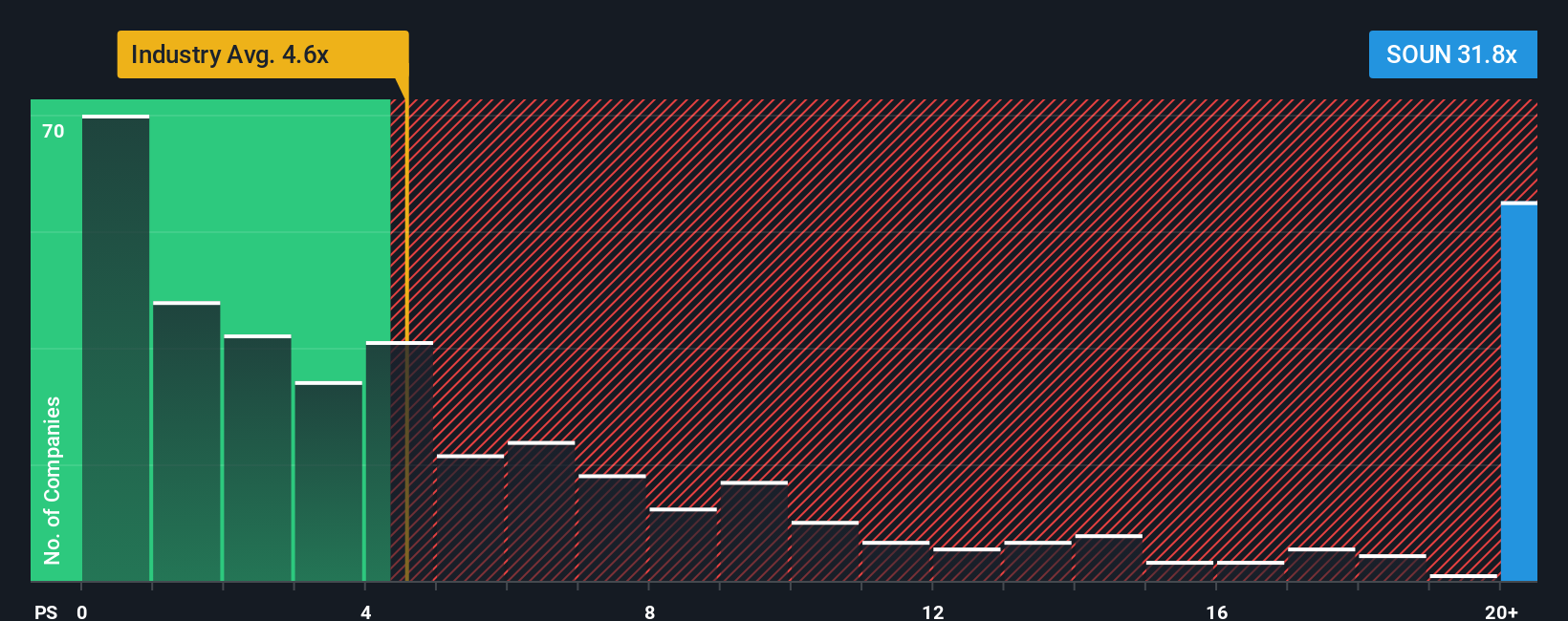

Most Popular Narrative: 70% Undervalued

StjepanK’s widely followed narrative puts SoundHound AI’s fair value at $28.58 per share, well above the last close of $8.56, and builds a detailed case around long term revenue potential.

SoundHound started as a Stanford dorm-based project between a few aspiring academics in 2004. At that time, hardly anyone thought about voice AI. However, over more than two decades, the team accumulated diverse experience with this technology, building a moat of over 280 patents that set it apart from competitors. These patents cover a wide range, including speech recognition, natural language understanding, and voice search.

Curious how that moat turns into a much higher share price estimate? The narrative leans on aggressive revenue expansion, improving margins, and a sizeable terminal valuation multiple. The exact mix of growth and profitability assumptions is where the story really gets interesting.

Result: Fair Value of $28.58 (UNDERVALUED)

However, the story hinges on big assumptions, and declining gross margins along with ongoing stock dilution could both chip away at that optimistic fair value case.

Another Take: Market Pricing Looks Rich

StjepanK’s $28.58 fair value leans on long term growth and margin gains, but the current P/S of 20.8x tells a very different story. That is much higher than both peers at 14.9x and the fair ratio of 5.3x, which points to meaningful valuation risk if expectations cool.

Build Your Own SoundHound AI Narrative

If you look at these numbers and come to a different conclusion, or just prefer your own process, you can build a custom view in minutes: Do it your way.

A great starting point for your SoundHound AI research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If SoundHound AI has sparked your interest, do not stop here; broaden your watchlist with other focused ideas that could sharpen your overall portfolio thinking.

- Target potential value candidates by scanning our list of 53 high quality undervalued stocks that pair solid fundamentals with attractive pricing on key metrics.

- Strengthen your income stream by reviewing 14 dividend fortresses, where yields above 5% are backed by resilient payout histories.

- Reduce portfolio stress by checking 85 resilient stocks with low risk scores, highlighting companies with lower risk scores that may help smooth out volatility.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.