Assessing SQM (NYSE:SQM) Valuation As Low Cost Lithium Position And EV Demand Support Momentum

Sociedad Quimica y Minera de Chile S.A. Sponsored ADR Pfd Series B SQM | 83.21 | +1.70% |

Recent commentary around Sociedad Química y Minera de Chile (NYSE:SQM) has focused on its role as a low cost lithium producer, supported by strong electric vehicle demand, rising specialty plant nutrition volumes, and favorable pricing conditions.

At a latest share price of US$70.91, Sociedad Química y Minera de Chile has seen a 29.99% 90 day share price return and an 83.56% 1 year total shareholder return. This suggests momentum has picked up recently as investors weigh stronger lithium and specialty plant nutrition demand against earlier volatility.

If this lithium story has your attention, it could be a good time to widen the lens and look at 8 top copper producer stocks as another way to find materials names tied to electrification trends.

With the shares up 83.56% over the past year and trading only about 4% below the latest analyst price target, the key question is whether SQM still offers value or if the market is already pricing in future growth.

Most Popular Narrative: 4% Undervalued

With Sociedad Química y Minera de Chile last closing at $70.91 against a most followed fair value estimate of $74.00, the current setup reflects only a modest valuation gap that hinges heavily on how its lithium and specialty chemicals story plays out.

Analysts have lifted their fair value estimate for Sociedad Química y Minera de Chile to US$74.00 from US$61.44, reflecting updated views on higher revenue growth assumptions, a lower discount rate, a higher future P/E multiple, and recent research that points to firmer lithium pricing and renewed sector interest, despite at least one more cautious broker stance.

Curious what supports that higher fair value? The narrative leans on faster top line growth, wider margins and a richer future earnings multiple. The exact mix matters. The full breakdown shows how those pieces are combined into a single number that sits just above today’s share price.

Result: Fair Value of $74 (UNDERVALUED)

However, this depends on lithium prices remaining supportive and on SQM successfully executing capital intensive projects such as Salar Futuro and the Codelco partnership without cost overruns or delays.

Another View: Earnings Multiple Sends A Different Signal

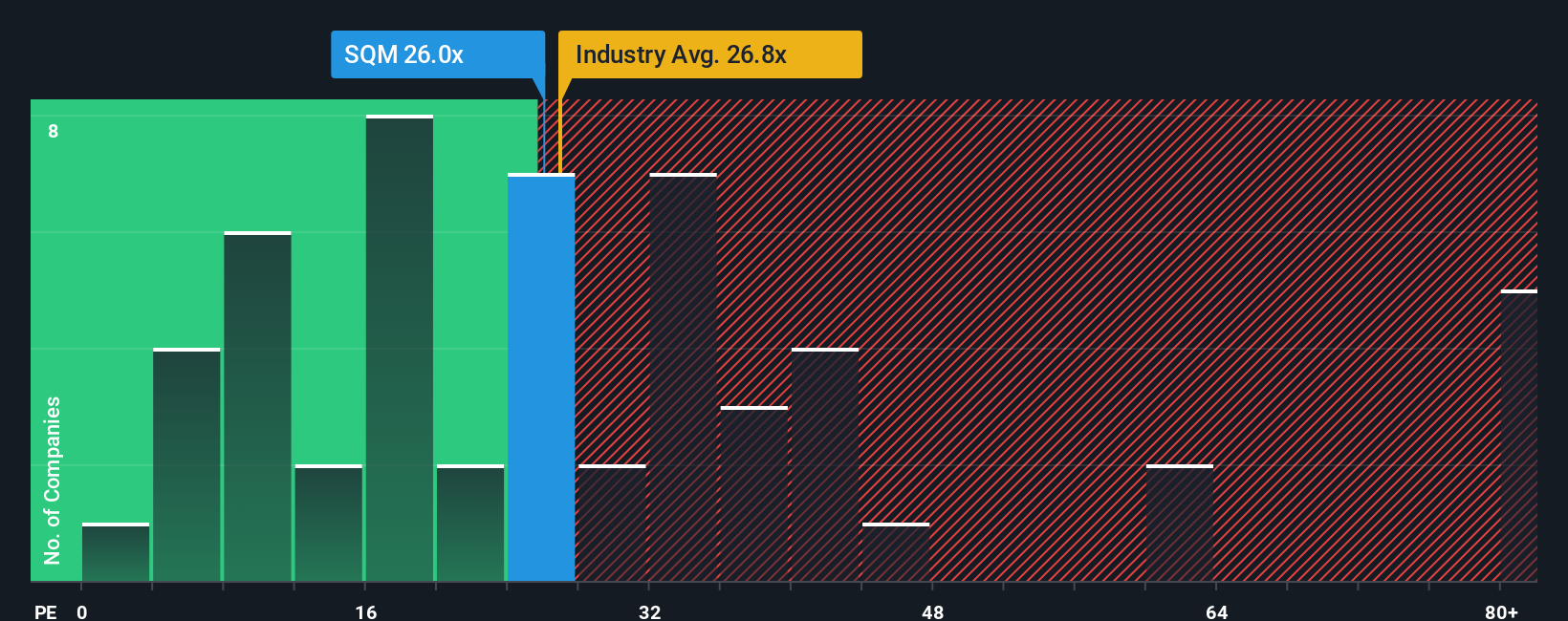

While our fair value estimate sits around $74, the current P/E of 38.2x tells a different story. That is richer than both the US Chemicals industry at 26.9x and peers at 28.4x, and also above the fair ratio of 31.2x that the market could move toward over time.

If earnings or sentiment cool, that P/E gap could compress quickly. The question for you is whether the current premium feels like an opportunity worth paying for or a valuation risk you would rather avoid.

Build Your Own Sociedad Química y Minera de Chile Narrative

If you see the story differently or want to stress test these assumptions with your own inputs, you can rebuild the whole picture yourself in just a few minutes, then Do it your way.

A great starting point for your Sociedad Química y Minera de Chile research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you are serious about building a stronger portfolio, do not stop at a single stock story. Widen your search and compare different types of opportunities.

- Target potential mispricings by scanning a focused list of 56 high quality undervalued stocks that combine quality fundamentals with appealing valuations.

- Strengthen your income stream by reviewing 13 dividend fortresses that aim to pair higher yields with resilience.

- Prioritize resilience by checking 86 resilient stocks with low risk scores that score well on stability and downside protection.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.