Assessing Stanley Black & Decker (SWK) Valuation After New Dewalt Powershift Launch At World Of Concrete

Stanley Black & Decker, Inc. SWK | 68.64 | -3.55% |

Product launch at World of Concrete puts focus on SWK’s tools business

Stanley Black & Decker (SWK) is attracting fresh attention after its DEWALT brand unveiled new POWERSHIFT concrete tools at the 2026 World of Concrete Trade Show, highlighting battery tech, safety features, and jobsite productivity.

The DEWALT POWERSHIFT launch comes at a time when momentum in Stanley Black & Decker’s shares has been picking up. The 30 day share price return is 15.93% and the 90 day gain is 24.39%. The 1 year total shareholder return of 5.20% contrasts with a 5 year total shareholder return decline of 43.77%.

If product launches like POWERSHIFT have you considering where tools demand could appear next, it may be worth scanning aerospace and defense stocks for other industrial names tied to large scale projects.

With SWK shares up about 24% over 90 days and trading only slightly below an average analyst target near US$83 to US$88, alongside a modelled intrinsic value implying a larger discount, you have to ask: is there still genuine upside here, or has the market already priced in what comes next?

Most Popular Narrative: 1.2% Undervalued

With Stanley Black & Decker’s shares last closing at US$84.40 and the most followed fair value estimate sitting just above US$85, the current setup hinges on how much weight you put on its long term margin and cash flow story.

The multi-year supply chain transformation nearing its final phase is delivering substantial recurring cost reductions, improved operational flexibility, and resilience to trade/tariff shocks; management expects these initiatives to drive gross margin back to 35%+ by late 2026, supporting sustained improvements in net margins and earnings.

Curious what kind of revenue path, margin rebuild, and future earnings multiple need to line up to support that fair value math? The full narrative lays out a detailed earnings bridge, a specific profit margin destination, and the valuation multiple that ties those assumptions back to today’s price.

Result: Fair Value of $85.44 (ABOUT RIGHT)

However, you still have to reckon with flat to slightly weaker sales guidance and pressure on pricing power if DIY demand and big box retail channels remain soft.

Another View: What The P/E Ratio Is Telling You

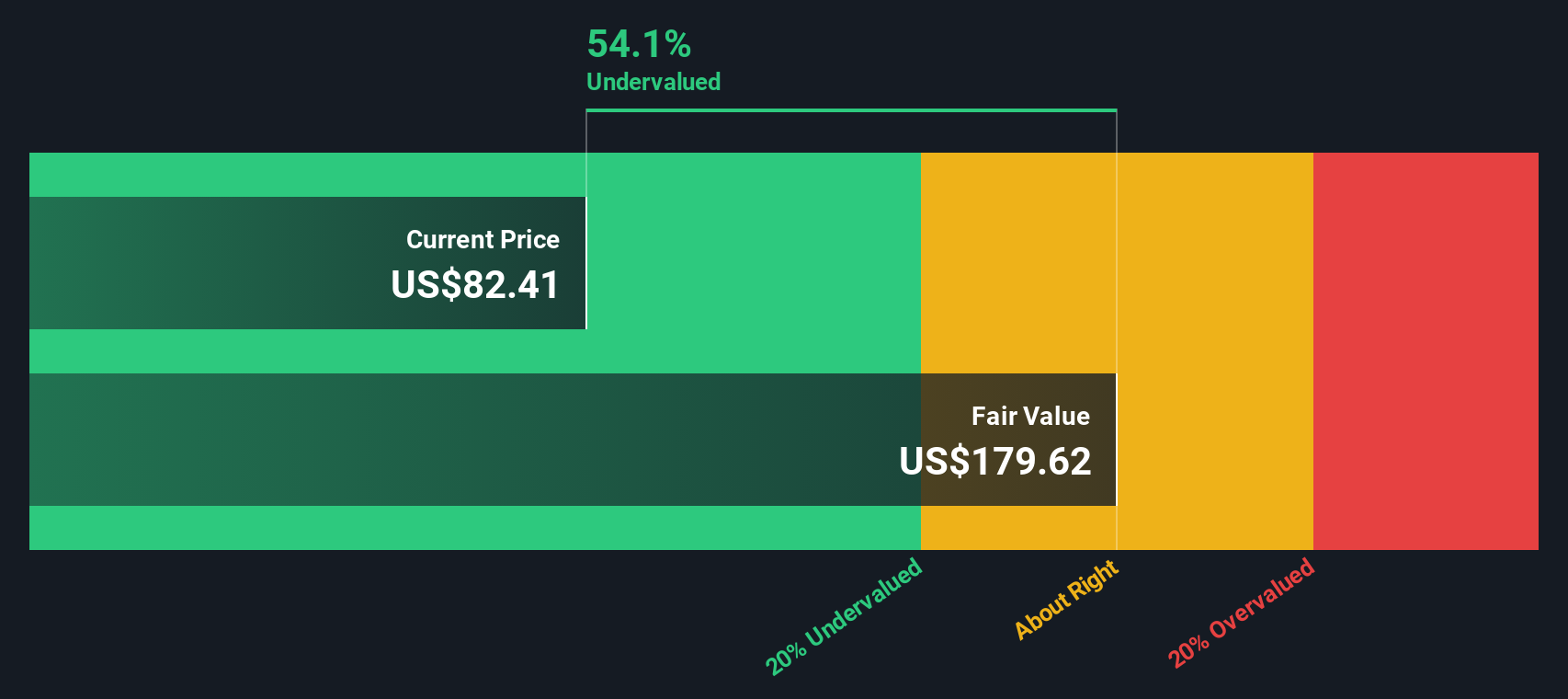

Our DCF model suggests Stanley Black & Decker’s shares trade about 53.2% below an estimated fair value of US$180.33, which points to an undervalued setup. That is a very different message to a fair value of roughly US$85 based on consensus earnings assumptions. Which signal do you trust more: the cash flow math, or the cautious analyst bridge?

Build Your Own Stanley Black & Decker Narrative

If you look at these numbers and reach a different conclusion, or simply prefer to test your own assumptions, you can build a complete view yourself in just a few minutes, starting with Do it your way.

A great starting point for your Stanley Black & Decker research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If SWK has you thinking more broadly about where to put fresh capital to work, do not stop here. You could miss some compelling setups elsewhere.

- Spot early stage opportunities with real business traction by scanning these 3539 penny stocks with strong financials before the crowd starts paying closer attention.

- Explore developments in automation and data driven tools by checking out these 24 AI penny stocks for companies tied to practical AI use cases.

- Focus on potential mispricings by reviewing these 868 undervalued stocks based on cash flows, which screens for companies trading below what their cash flows may support.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.