Assessing Stevanato Group (STVN) Valuation After Recent Share Weakness And Undervalued Fair Value Narrative

Stevanato Group SpA STVN | 13.73 | -0.15% |

Recent share performance and what it might signal

Stevanato Group (STVN) has drawn attention after a stretch of weaker share performance, including negative returns over the past week, month, past 3 months and year, prompting investors to reassess what the current price implies.

With the share price at US$16.97, Stevanato Group’s recent 7 day share price return of 11.15% and 30 day and 90 day declines of 18.02% and 34.22% suggest fading momentum, and the 1 year total shareholder return of 18.62% points to pressure over a longer holding period as well.

If this kind of move has you rethinking your exposure to healthcare suppliers, it could be worth scanning other healthcare stocks that might fit your portfolio criteria.

With STVN trading at US$16.97, annual revenue of about €1.17b and net income of roughly €140.6m, the key question for you is simple: is this a chance to buy on weakness, or is the market already pricing in future growth?

Most Popular Narrative: 41% Undervalued

At $16.97, the most followed narrative sees Stevanato Group’s fair value closer to $28.78, which frames today’s price as a sizeable discount.

Scaling commercial production at the Latina and Fishers greenfield sites, along with business optimization and an increased mix of high-value solutions, is expected to unlock meaningful operating leverage as utilization ramp-up reduces margin dilution and supports consolidated gross margin and EBITDA margin improvements over the next several years.

Want to see what sits behind that confidence in higher earnings and margins over time? The narrative leans on steady revenue expansion, rising profitability, and a future earnings multiple that assumes investors will keep paying up for this growth profile. Curious how those moving parts combine to reach that higher fair value target? The full story joins those pieces together.

Using a 10.78% discount rate, the narrative’s fair value estimate of $28.78 for Stevanato Group rests on earnings, margin and growth assumptions that differ from what the current share price suggests. Analysts behind this view are building in ongoing revenue growth, expanding profit margins and a future P/E level that remains above the broader US Life Sciences industry, while still below where the company is implied to trade today in that scenario.

Result: Fair Value of $28.78 (UNDERVALUED)

However, this story can change quickly if rising costs at new facilities or prolonged weakness in the Engineering segment put sustained pressure on margins and earnings.

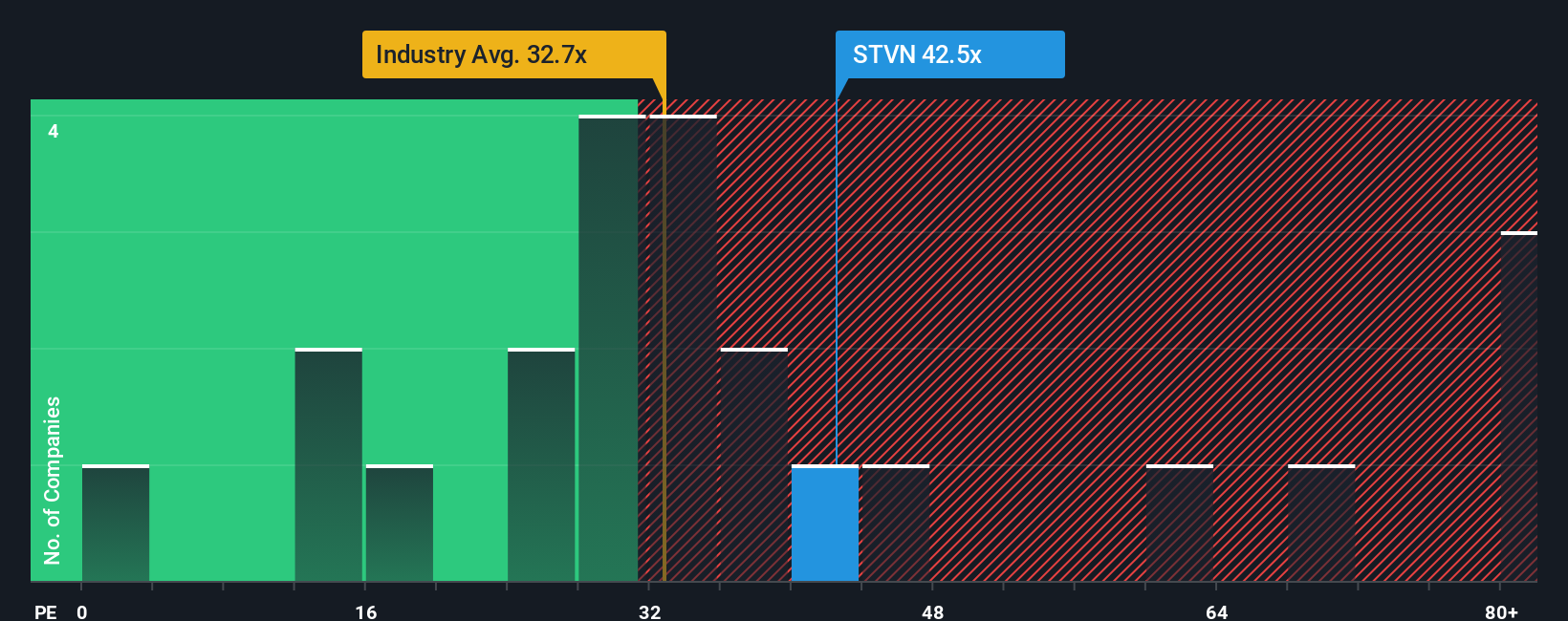

Another View: What the current P/E might be telling you

Analysts see upside to $28.68, yet Stevanato Group currently trades on a P/E of 27.3x. That is below the North American Life Sciences average of 35.9x, but above its own fair ratio of 22.1x. This could mean there is less room for error if earnings progress stalls.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Stevanato Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 876 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Stevanato Group Narrative

If you look at the numbers and reach a different conclusion, or simply prefer to run your own checks, you can build a custom view in just a few minutes with Do it your way.

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Stevanato Group.

Looking for more investment ideas?

If Stevanato Group has you thinking harder about where your next opportunity might come from, this is the moment to widen your search and pressure test fresh ideas.

- Spot potential value in companies the market may be overlooking by scanning these 876 undervalued stocks based on cash flows, which is built around discounted cash flow fundamentals.

- Back big themes in artificial intelligence by sorting through these 24 AI penny stocks, which connect growth potential with clear business models.

- Target regular income streams by reviewing these 13 dividend stocks with yields > 3%, focused on yields above 3% with supporting fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.