Assessing TFS Financial (TFSL) Valuation After Strong One Year Shareholder Returns

Tfs Financial TFSL | 0.00 |

TFS Financial (TFSL) is drawing investor attention after recent share price moves. The stock last closed at $15.91 as traders reassess its retail consumer banking footprint and earnings profile.

While the latest move to $15.91 is modest on the day, it sits against a 30 day share price return of 5.9% and a 90 day share price return of 11%. The 1 year total shareholder return of 30.9% suggests momentum has been building over time.

If recent gains in TFS Financial have you thinking about where else value might be hiding, it could be a good moment to broaden your search and look at 20 top founder-led companies

With TFSL trading around $15.91, some metrics hint at a possible discount while others suggest expectations are already optimistic. Is this a genuine value opportunity, or is the market already pricing in future growth?

Price-to-Earnings of 48.4x: Is it justified?

Based on the preferred P/E multiple, TFS Financial appears expensive, with a 48.4x P/E against a last close of $15.91 and lower comparative benchmarks.

The P/E ratio compares the share price to earnings per share, so a higher figure often reflects higher expectations for future profits. For a bank like TFSL, such a high P/E suggests the market is assigning a premium to its earnings profile relative to many peers.

Here, that premium is clear. TFSL's P/E of 48.4x is well above the estimated fair P/E of 12.2x, and also above the US Banks industry average of 11.5x and the peer average of 11.3x. This gap is substantial and indicates a valuation level that is significantly higher than what earnings alone would suggest if the market moved closer to the fair ratio benchmark.

Result: Price-to-Earnings of 48.4x (OVERVALUED)

However, there are clear risks, including the stock trading above the US$15.50 analyst target, and a P/E far above both its estimated fair P/E and industry peers.

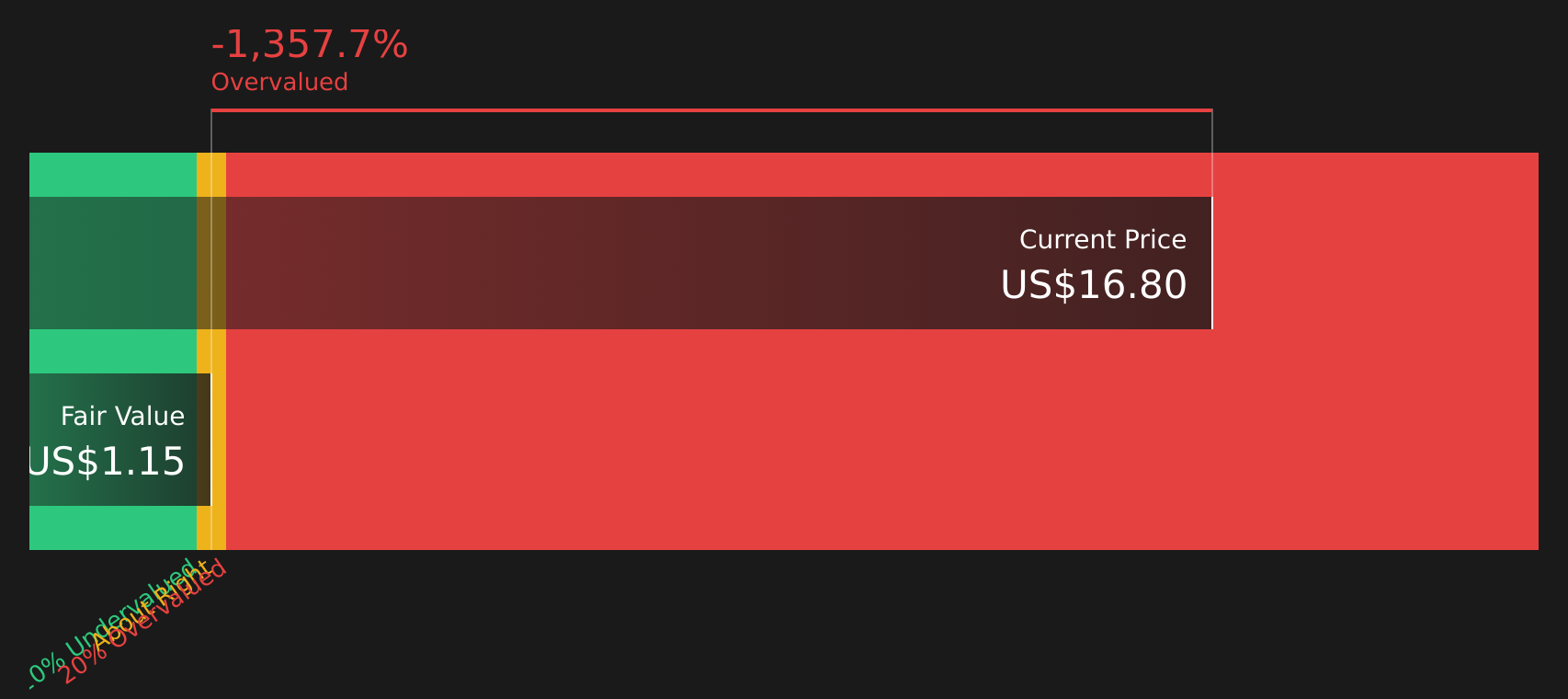

Another View: Cash Flows Paint a Harsher Picture

While the P/E ratio points to an expensive stock, the SWS DCF model goes further, with an estimated future cash flow value of $1.14 versus the current $15.91 share price. That gap signals a very rich price. If earnings growth slows, how much patience will investors really have?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out TFS Financial for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of rich valuation and cautious cash flow signals leaves you unsure, now is the time to review the full picture yourself. Weigh both sides by checking the 2 key rewards and 1 important warning sign

Looking for more investment ideas?

If you are weighing what to do next, do not stop with a single stock. Broaden your watchlist so you are not missing other potential opportunities.

- Broaden your search for quality at a compelling price by reviewing the 46 high quality undervalued stocks that pass strict earnings and balance sheet filters.

- Strengthen your focus on income by scanning the 10 dividend fortresses that combine higher yields with supporting fundamentals.

- Protect your downside by concentrating on the 63 resilient stocks with low risk scores that show resilient financial profiles and lower overall risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.