Assessing TIC Solutions (TIC) Valuation After Loan Repricing And 2029 Investor Day Targets

TIC Solutions TIC | 0.00 |

TIC Solutions (TIC) is back in focus after repricing its roughly $1.6b First Lien Term Loan to SOFR + 2.5%, trimming its margin by 0.25% and reducing annual cash interest expense by about $4m.

The repricing news comes after a softer patch for the stock. The 1-day share price return was 2.17% and the 7-day gain was 1.56%, set against a 30-day share price decline of 8.62% and a 1-year total shareholder return decline of 16.12%. This suggests that recent momentum is improving, while longer term performance remains weak.

If this kind of debt repricing has you thinking about where else capital might find a home, it could be worth scanning 33 power grid technology and infrastructure stocks for other infrastructure linked opportunities.

With the stock down over the past year, trading at $8.48 and flagged with a value score of 4 despite ambitious 2029 targets, is TIC Solutions quietly undervalued at this level, or are markets already pricing in future growth?

Most Popular Narrative: 28% Undervalued

With TIC Solutions last closing at $8.48 and the most followed narrative pointing to a fair value of $11.79, the implied gap is hard to ignore and hinges on some punchy long term assumptions.

The company's resilient core recurring revenue base (run and maintain work) combined with mandatory service requirements in sectors like energy, transportation, and industrials, position it to outperform through economic cycles, enhancing confidence in sustainable revenue and cash flow growth.

Curious what underpins that higher fair value? The narrative leans on faster top line expansion, improving margins, and a future earnings multiple far above the sector. The exact mix of those inputs may surprise you.

Result: Fair Value of $11.79 (UNDERVALUED)

However, that upside story relies heavily on smoothing out recent margin pressure and successfully integrating NV5, where slower synergy delivery or cost creep could quickly weaken the thesis.

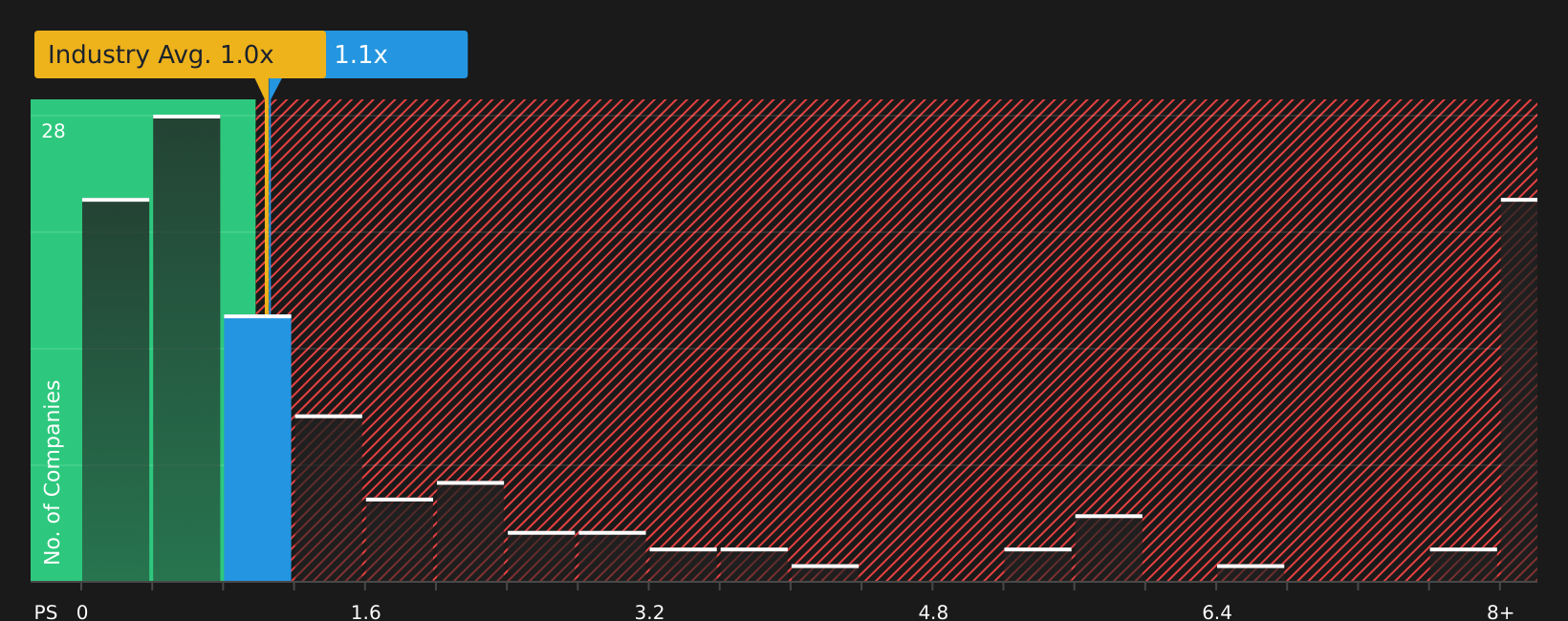

Another View: What The P/S Ratio Is Saying

The narrative and analyst targets frame TIC Solutions as undervalued, yet the current P/S ratio of 1.1x sits slightly above the US Professional Services industry at 1x. Compared with peers on 4.1x and a fair ratio of 1.3x, the stock screens cheaper than many. The key question is whether this discount reflects compensation for execution and leverage risk, or something else.

Next Steps

Mixed signals on value and risk so far? Take a moment to review the numbers yourself, weigh both sides, and see the 2 key rewards and 1 important warning sign.

Looking for more investment ideas?

If you stop with just one stock, you risk missing other opportunities that might fit your goals even better, so keep casting the net wider.

- Spot potential value plays early by scanning 47 high quality undervalued stocks before the crowd fully pays attention.

- Strengthen your focus on stability by reviewing companies in the 63 resilient stocks with low risk scores that score well on resilience.

- Hunt for lesser known opportunities with solid fundamentals using the screener containing 22 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.