Assessing Tidewater (TDW) Valuation After Expanded Rimini Street Partnership And Financial Platform Upgrade

Tidewater Inc TDW | 84.38 | +1.13% |

Tidewater (TDW) is back in focus after extending its collaboration with Rimini Street to cover SAP systems and new tax software, a material upgrade aimed at unifying global financial operations.

The extended Rimini Street partnership lands at a time when the 30-day share price return of 18.91% and 90-day share price return of 22.45% suggest building momentum, while the 1-year and 5-year total shareholder returns indicate a strong longer term record from a low base.

If this kind of operational upgrade has your attention, it may be a moment to see what else is moving in energy and infrastructure, including aerospace and defense stocks.

With TDW up 22.45% over 90 days and trading near a published analyst target of US$62.83, the real question now is whether the stock still trades at a discount or if the market is already pricing in future growth.

Most Popular Narrative: 0.6% Overvalued

With Tidewater last closing at $60.38 against a narrative fair value of $60, the current setup hinges on how future earnings power is interpreted.

Fleet modernization and disciplined operational execution have delivered three consecutive quarters of 50%+ gross margin, underpinning the expectation of structurally higher operating margins and net earnings as the company benefits from lower repair/maintenance costs and higher reliability.

Curious what has to happen for that earnings story to hold up? The narrative leans heavily on rising margins, disciplined capital use, and a valuation multiple that has to compress over time. The exact mix of revenue growth, margin expansion, and discount rate assumptions is doing a lot of work here, but the details sit beneath the headline fair value.

Result: Fair Value of $60 (OVERVALUED)

However, that story can run into trouble if offshore demand stays soft for longer or if acquisition and integration efforts fail to deliver the expected benefits.

Another View: Cash Flows Tell a Different Story

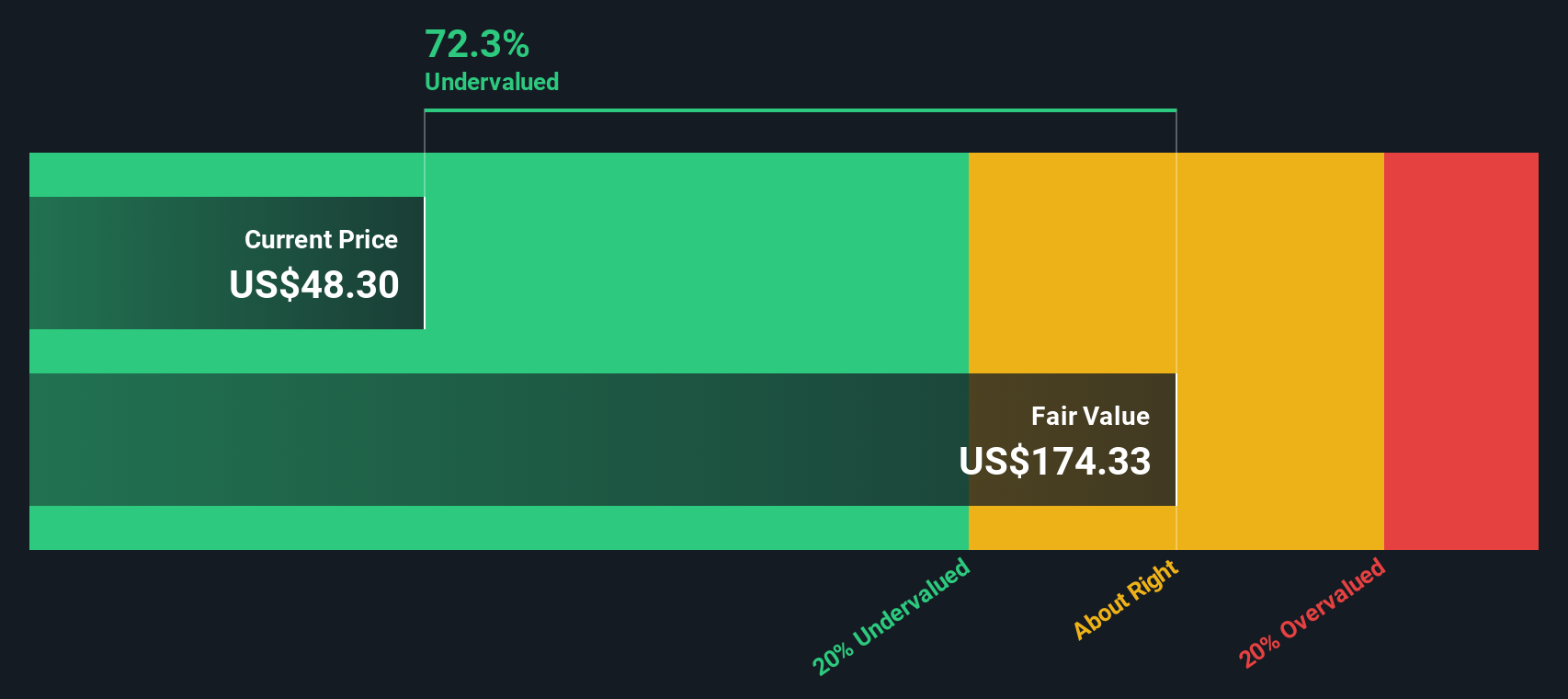

The narrative fair value suggests Tidewater is slightly overvalued at $60 against a $60 fair value, but the SWS DCF model points a very different way. On that cash flow view, TDW at $60.38 is trading around 68% below an estimated value of $187.67.

When one approach flags a mild premium and another implies a wide discount, it raises a simple question for you: which set of assumptions about future earnings and risk feels more realistic?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Tidewater for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 862 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Tidewater Narrative

If you look at these numbers and reach a different conclusion, or simply want to stress test the assumptions yourself, you can build a tailored view in minutes: Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Tidewater.

Looking for more investment ideas?

If Tidewater has sparked your interest, do not stop here. Use the Simply Wall Street Screener to spot other stocks that might better fit your plan.

- Target reliable cash generators by checking out these 13 dividend stocks with yields > 3% that may offer income potential alongside business stability.

- Position yourself for long term themes by scanning these 24 AI penny stocks that are tied to artificial intelligence adoption.

- Hunt for potential mispricings with these 862 undervalued stocks based on cash flows, where the focus is on businesses trading below estimated cash flow value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.