Assessing TKO Group Holdings' Valuation Following Major Debt Refinancing and Capital Structure Changes

TKO Group Holdings, Inc. Class A TKO | 203.76 | +1.34% |

Have you been watching TKO Group Holdings (NYSE:TKO) lately? There is a lot to unpack after its indirect subsidiary signed a major amendment to its credit agreement. The company has refinanced its outstanding term loans, added a substantial $1.0 billion first lien term loan to the mix, and extended the maturity of its revolving credit facility until 2030. Moves like these highlight TKO’s evolving capital structure and clearly raise the stakes for both current and potential shareholders.

This debt financing decision comes at a time when TKO’s stock momentum has been on the upswing, gaining 8% over the past month and an impressive 66% over the past year. The performance suggests that investors are at least partly optimistic about the company’s prospects and risk profile, potentially encouraged by recent growth in both revenue and net income. While other stories have emerged in recent quarters, this refinancing may be the headline that shapes perceptions of TKO’s balance sheet strength going forward.

With the share price trending higher and new capital available, the question now is whether TKO is actually undervalued or if the market is already pricing in these ambitious growth moves. Would you step in, or is the best upside already on the table?

Price-to-Earnings of 78.3x: Is it justified?

TKO currently trades at a Price-to-Earnings (P/E) ratio of 78.3x, which makes it look expensive relative to both its industry peers and the overall market. In fact, this figure is substantially higher than the average P/E ratio of the US Entertainment industry, which stands at just 34x. This premium valuation raises questions about whether the market is overly optimistic about TKO’s future growth or if investors see unique qualities in the company that warrant such a significant markup.

The P/E ratio is one of the most widely used measures for valuing a company. It shows how much investors are willing to pay for each dollar of earnings, reflecting both current profitability and future expectations. For a media and entertainment group like TKO, the P/E multiple is especially relevant as it incorporates forecasts for earnings growth and perceived competitive position in a rapidly changing industry.

Trading at such an elevated P/E, TKO appears to be pricing in aggressive earnings growth and a significant premium for its future prospects. This could reflect belief in the company’s revenue and profit growth trajectory or market confidence tied to recent strategic moves. However, it also puts pressure on TKO to deliver substantial performance in coming years.

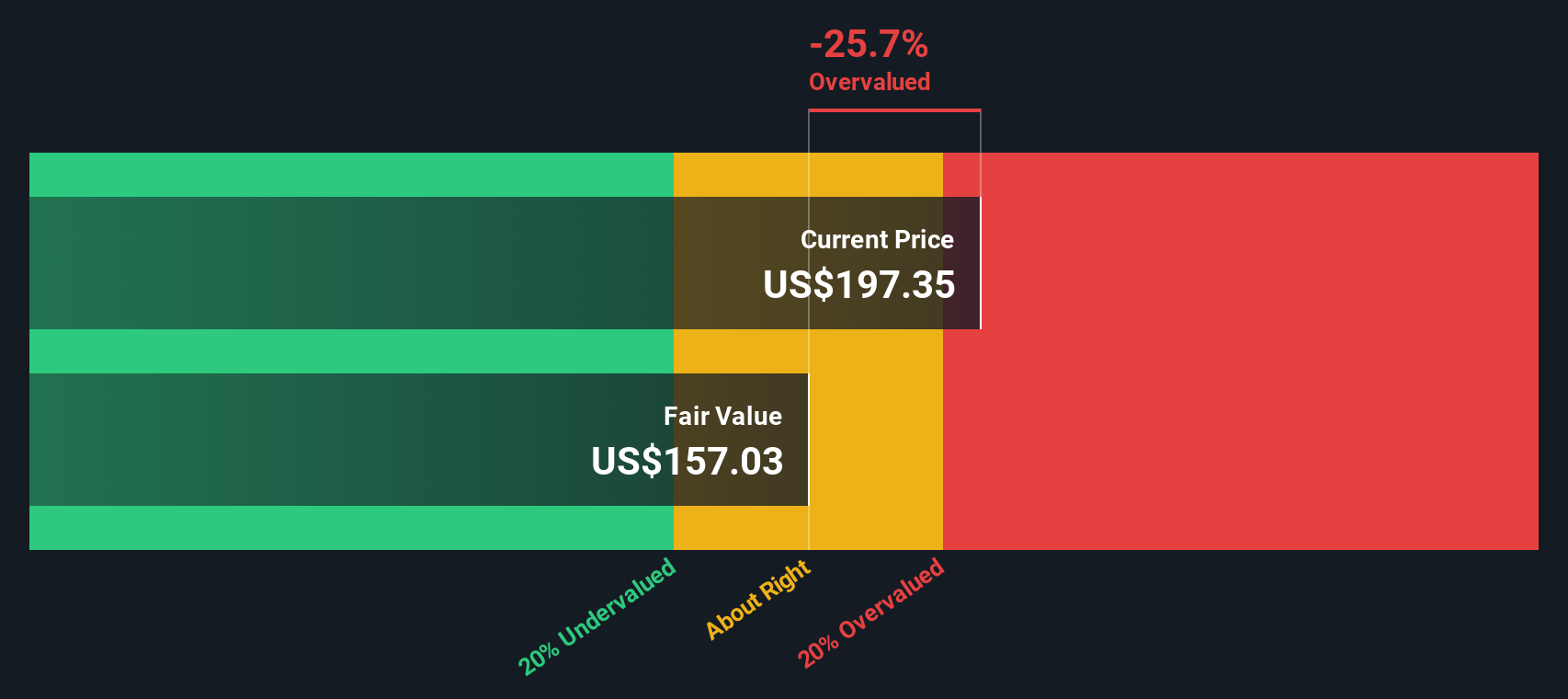

Result: Fair Value of $153.45 (OVERVALUE)

See our latest analysis for TKO Group Holdings.However, slowing revenue growth or unmet earnings expectations could challenge the bullish narrative and lead to a reassessment of TKO’s lofty valuation.

Find out about the key risks to this TKO Group Holdings narrative.Another View: What Does the SWS DCF Model Say?

Taking another angle, our discounted cash flow (DCF) model also suggests TKO is valued above what long-term cash flows might warrant. This method highlights a different risk: are investor expectations running ahead of fundamentals?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own TKO Group Holdings Narrative

If you want to dig deeper or take a different perspective, you have the tools to build your own analysis in just a few minutes. Do it your way.

A great starting point for your TKO Group Holdings research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more smart investment ideas?

Want to stay ahead of the crowd? Let Simply Wall Street’s enhanced screener help you spot new opportunities in markets worth your attention. Give these a try and watch your portfolio take on a fresh edge:

- Amplify your income with stocks offering strong yields by checking out our list of dividend stocks with yields > 3%, and see which companies make every dollar work harder for you.

- Accelerate your research into next-wave tech by tapping into AI penny stocks, and find innovative AI names gaining traction in a data-driven world.

- Unlock real value prospects with our selection of undervalued stocks based on cash flows, to identify businesses priced below their true potential before mainstream investors catch on.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.