Assessing TransMedics Group (TMDX) Valuation After FDA IDE Approval For ENHANCE Heart Trial

TransMedics Group TMDX | 100.69 | +0.29% |

The trigger for TransMedics Group (TMDX) stock today is the U.S. FDA granting full IDE approval for its Next Generation OCS ENHANCE Heart trial, a key step for advanced heart transplant procedures.

Despite today’s reaction, with the share price at $128.52 after a 1-day share price return of a 3.59% decline and a softer 30-day share price return of a 9.94% decline, momentum over the past quarter remains positive and the 1-year total shareholder return of 80.45% highlights how strongly sentiment has shifted ahead of trial progress, leadership changes and the upcoming full year 2025 results update.

If this FDA update has you thinking more broadly about where growth stories can come from in healthcare, you may want to scan our screener for 24 healthcare AI stocks as a starting point for other ideas.

With the stock up 80.45% over the past year and trading at $128.52 against an analyst price target of $144.20 and a modelled intrinsic value gap, the real question is whether there is still an opportunity here or if the market is already pricing in future growth.

Most Popular Narrative: 10.9% Undervalued

At $128.52 against a widely followed fair value estimate of $144.20, the current price sits below where the narrative framework places TransMedics Group, using a discount rate of 7.89%.

Expansion into new organ types (notably kidney) and next-generation product launches (Gen 3 OCS platforms for heart, lung, and liver) are expected to materially grow TransMedics' total addressable market, improve product mix, and support higher average selling prices, benefiting earnings and longer-term net margins.

Curious what kind of revenue ramp, margin profile and future earnings multiple are baked into that fair value line? The narrative leans on transplant volume growth, richer OCS mix and recurring services to justify its earnings path and valuation anchor, but the exact numbers sit inside the full write up.

Result: Fair Value of $144.20 (UNDERVALUED)

However, this hinges on TransMedics staying ahead on technology and trials, and on competition or regulation not squeezing transplant volumes or future margins.

Another View: High Multiple, Higher Expectations

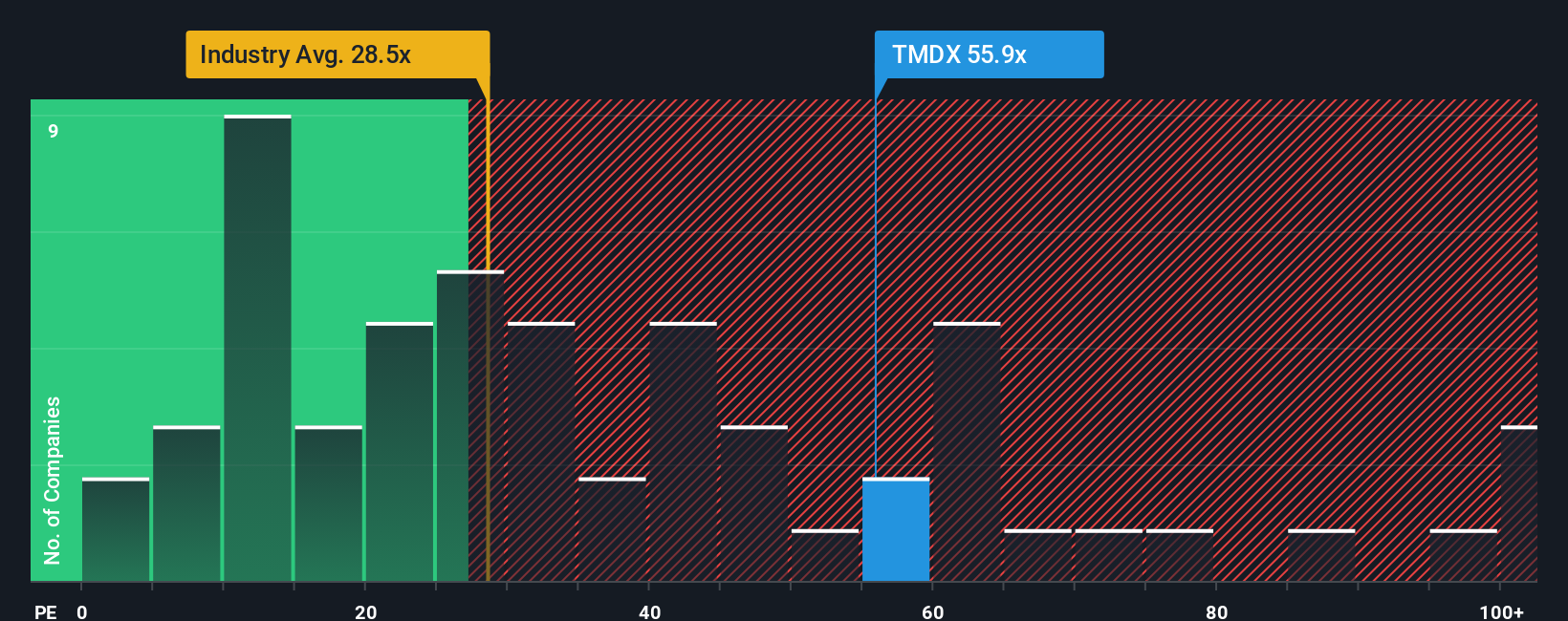

That 10.9% gap to the $144.20 fair value line sits awkwardly next to the current P/E of 47.9x. The fair ratio sits at 23.9x, the US Medical Equipment industry is around 29.7x and peers are near 43.5x. This points to rich pricing and less room for errors. What convinces you this premium is justified?

Build Your Own TransMedics Group Narrative

If you see the numbers differently or prefer to test your own assumptions against the data, you can shape a fresh TransMedics view in minutes using Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding TransMedics Group.

Looking for more investment ideas?

Once you have formed your view on TransMedics, it is worth lining it up against other opportunities so you can see where it really stands in your portfolio.

- Spot potential mispricings early by checking companies that screen as 55 high quality undervalued stocks before the crowd pays closer attention.

- Strengthen your core holdings by focusing on businesses in the solid balance sheet and fundamentals stocks screener (45 results) that pair financial resilience with fundamentals you can monitor over time.

- Get ahead of the pack by reviewing our screener containing 23 high quality undiscovered gems, where strong financials meet lower market attention and fresh ideas often emerge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.