Assessing TransMedics Group (TMDX) Valuation After New Headquarters And Campus Expansion Commitment

TransMedics Group TMDX | 100.69 | +0.29% |

TransMedics Group (TMDX) has committed to a long-term lease for a new global headquarters at Assembly Innovation Park in Somerville, and it has acquired adjacent land to build an integrated campus and expand its transplant therapy operations.

The headquarters announcement follows a period of strong recent momentum, with a 1-day share price return of 5.98% lifting TransMedics Group to US$142.71 and contributing to a 30-day share price return of 12.56%. The 1-year total shareholder return of 128.19% indicates sustained interest in the story.

If this kind of growth-focused healthcare story interests you, it could be a useful moment to scan healthcare stocks for other potential opportunities in the sector.

With TransMedics now committing to a larger, integrated campus and the share price already up sharply over 1 and 3 years, the key question is simple: is there still upside left here, or is the market already pricing in future growth?

Most Popular Narrative: 1.4% Undervalued

With TransMedics Group last closing at US$142.71 against a narrative fair value of about US$144.73, the current setup leans slightly in favor of the valuation story that analysts are tracking.

Analysts are assuming TransMedics Group's revenue will grow by 18.8% annually over the next 3 years.

Expansion into new organ types (notably kidney) and next-generation product launches (Gen 3 OCS platforms for heart, lung, and liver) are expected to materially grow TransMedics' total addressable market, improve product mix, and support higher average selling prices, benefiting earnings and longer-term net margins.

Curious what sits behind that slight uplift in fair value? The narrative leans on faster transplant volumes, richer margins, and a future earnings multiple that is usually reserved for top tier medical names. Want to see exactly how those growth, margin, and valuation assumptions stack together into that US$144.73 figure?

Result: Fair Value of $144.73 (UNDERVALUED)

However, there is still meaningful risk if upcoming heart and lung trials disappoint or if higher R&D and headquarters spending keep margins under pressure for longer than expected.

Another View: Earnings Multiple Sends A Different Signal

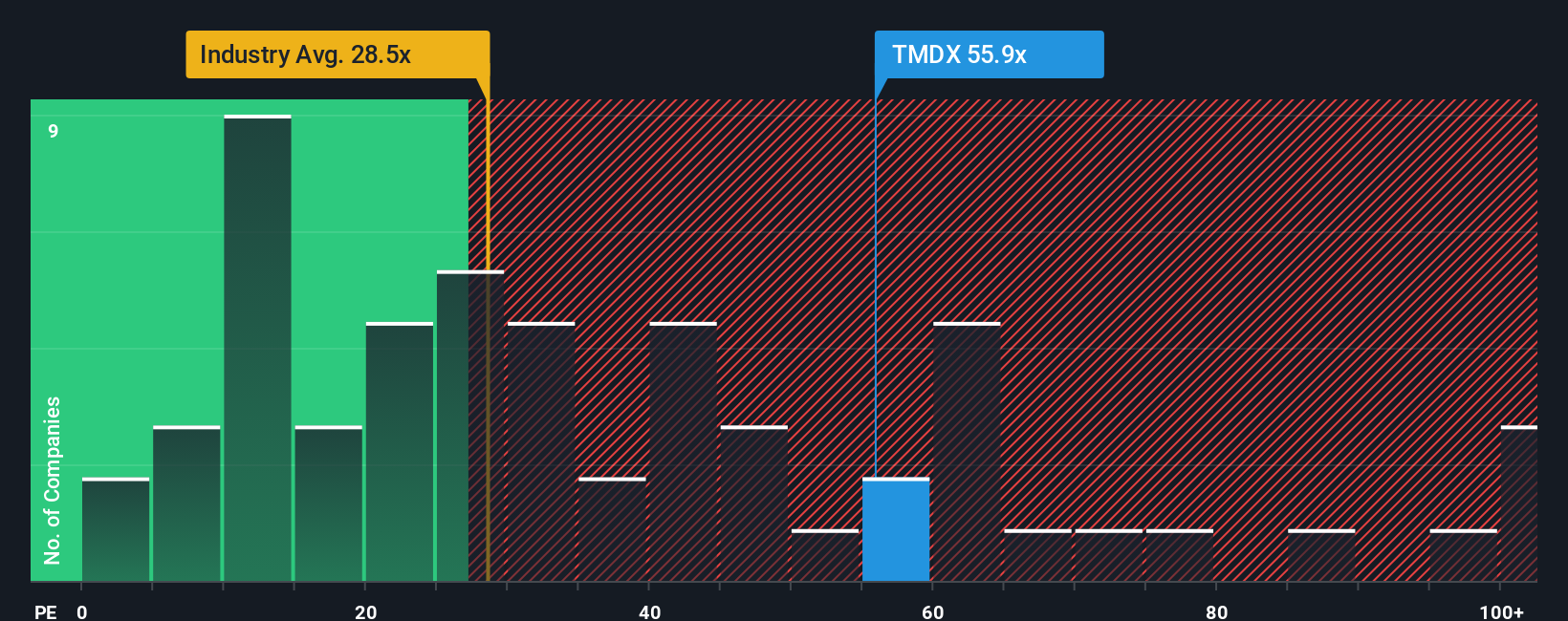

While the narrative fair value suggests only a small 1.4% uplift, the current P/E ratio of 53.1x tells a different story. It sits well above the Medical Equipment industry at 31.2x, above peers at 39.4x, and above a fair ratio of 24.1x. This points to meaningful valuation risk if expectations cool.

Build Your Own TransMedics Group Narrative

If you see the story differently or prefer to review the numbers yourself, you can build a custom view in minutes with Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding TransMedics Group.

Ready for more investment ideas?

If TransMedics has caught your attention, do not stop here. Broaden your watchlist with a few targeted ideas that could sharpen how you think about risk and reward.

- Zero in on potential mispricings by scanning these 884 undervalued stocks based on cash flows that may offer more appealing entry points based on cash flow fundamentals.

- Ride accelerating themes in automation and machine learning by checking out these 25 AI penny stocks that put artificial intelligence at the core of their business models.

- Tap into income focused ideas by reviewing these 13 dividend stocks with yields > 3% that may offer yields above 3% while you assess long term prospects.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.