Assessing Tronox Holdings (TROX) Valuation After Recent Share Price Volatility And Mixed Fair Value Signals

Tronox Holdings Plc TROX | 9.18 | -2.13% |

Event overview and recent price context

Tronox Holdings (TROX) has drawn attention after recent share price volatility, with the stock down about 10% over the past month but up roughly 43% in the past 3 months.

For investors, that mix of short term weakness and stronger recent momentum raises questions about how the current US$6.76 share price lines up with Tronox Holdings' value score of 4 and its reported financial profile.

Looking beyond the recent pullback, Tronox Holdings has a 7 day share price return of an 8.28% decline and a 90 day share price return of 42.62%, while the 3 year total shareholder return stands at a 39.66% decline. This suggests that recent momentum contrasts with weaker longer term outcomes and may reflect shifting views on its risk and earnings profile at the current US$6.76 share price.

If this kind of rebound after a weak patch has your attention, it could be a good moment to see what else is moving in materials and mining, starting with our 29 best rare earth metal stocks as a focused discovery list.

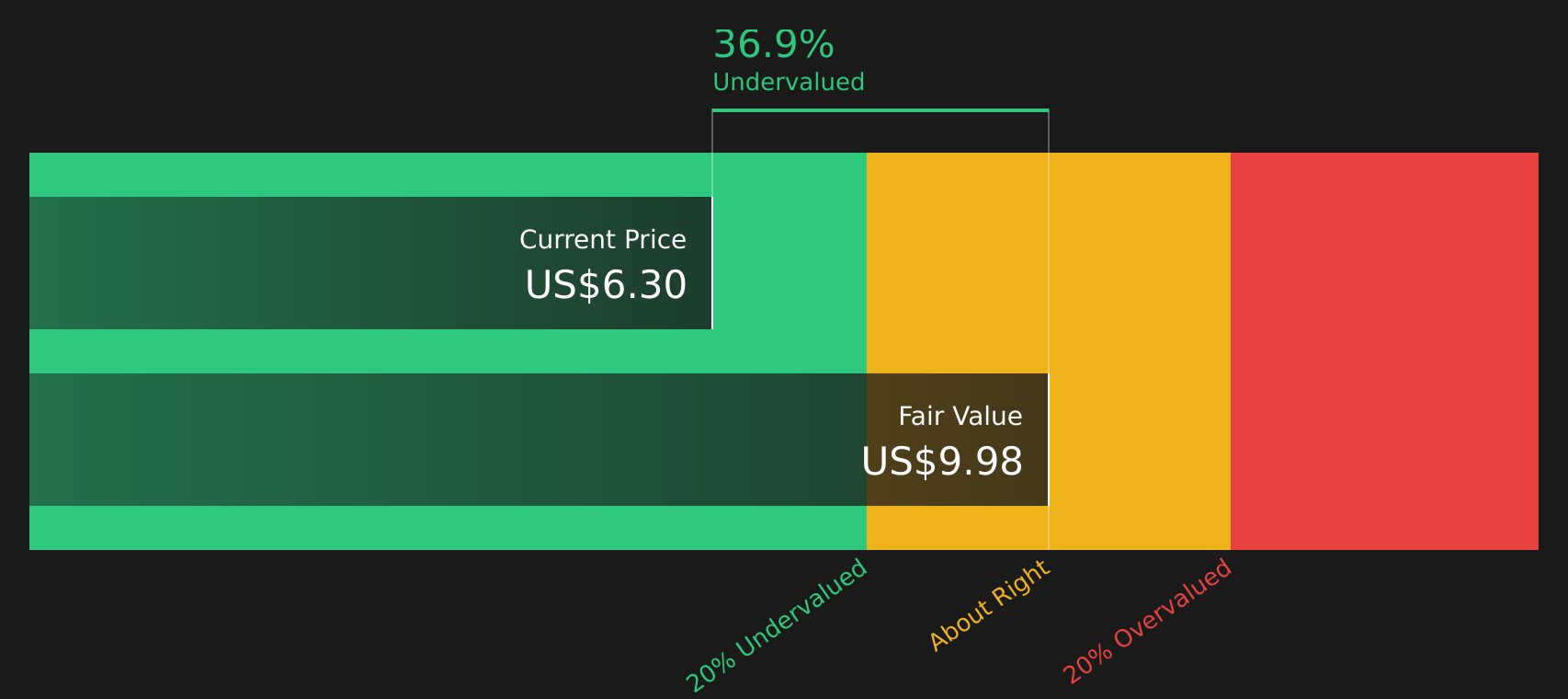

With Tronox trading near its analyst price target and showing a value score of 4 alongside an estimated 5% intrinsic discount, you have to ask: is there still a mispricing here, or is the market already baking in future growth?

Most Popular Narrative: 10.7% Overvalued

Compared with Tronox Holdings' last close at $6.76, the most widely followed narrative points to a fair value of $6.11, built on detailed cash flow and growth assumptions using a 7.8% discount rate.

Rare earth and other specialty mineral side-streams present incremental, higher-margin growth avenues. Tronox is actively progressing partnerships and government funding efforts for these initiatives, which could diversify revenue streams and further boost earnings as new projects come online.

Curious how a company that is currently unprofitable still earns a premium to this fair value estimate? Revenue growth assumptions, margin rebuild, and future earnings multiples all play a part, and the tension between modest growth forecasts and higher cash flow expectations sits at the core of this narrative.

Result: Fair Value of $6.11 (OVERVALUED)

However, the picture could change quickly if regulatory costs climb further or if Tronox's US$2.9b net debt and 6.1x net leverage begin to bite harder.

Another way to look at value

That 10.7% overvalued narrative sits awkwardly next to our DCF model, which points to a fair value of $7.11, about 4.9% above the current $6.76 share price. If the cash flow work is right, is the market underestimating Tronox, or are the DCF assumptions too generous?

Next Steps

If this mix of signals leaves you unsure which way to lean, take a closer look at the underlying data now and weigh both sides carefully. You can start with 2 key rewards and 2 important warning signs.

Looking for more investment ideas?

If this story has you thinking more broadly about your portfolio, do not stop at a single stock when there are plenty of other angles to consider.

- Target consistent cash returns by scanning companies that aim to support regular income, starting with our 14 dividend fortresses as a shortlist of yield focused names.

- Hunt for quality at a sensible price by reviewing our 50 high quality undervalued stocks, built to spotlight companies with solid fundamentals that may not be fully appreciated yet.

- Strengthen your downside protection by checking the 67 resilient stocks with low risk scores, a set of businesses that our models flag with relatively lower overall risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.