Assessing Tyson Foods (TSN) Valuation After Recent Share Price Momentum

Tyson Foods, Inc. Class A TSN | 64.63 | +0.51% |

Recent performance snapshot

Tyson Foods (TSN) has drawn fresh attention after a strong recent run in the share price, with the stock showing positive returns over the past month and past 3 months.

Over the past month, Tyson Foods has returned 16.5%, while the past 3 months show a gain of 23.8%. The stock closed at US$65.20, with year to date and 1 year total returns also in positive territory.

The recent 30 day share price return of 16.5% and 90 day share price return of 23.8%, alongside a 1 year total shareholder return of 17.6%, suggest momentum has picked up after a steadier year to date.

If Tyson Foods has you rethinking where defensiveness fits in your portfolio, this can be a good moment to broaden your search and check out 22 top founder-led companies.

With Tyson Foods trading at US$65.20, sitting about 6% below the average analyst price target and showing an estimated intrinsic discount near 53%, you have to ask: is there real value left here, or is the market already baking in future growth?

Most Popular Narrative: 5.6% Undervalued

With Tyson Foods at $65.20 against a widely followed fair value estimate of $69.08, the narrative is framing the current price as modestly below its calculated worth, anchored in a detailed view of protein markets and margin recovery.

The company is capitalizing on strong, resilient consumer demand for protein across beef, pork, and chicken, with volume and dollar share gains in top brands such as Tyson, Hillshire Farm, and Jimmy Dean; this leverages growing global consumption of animal protein, and is expected to support sustained revenue growth and earnings expansion.

Momentum in prepared and value-added foods, driven by a robust innovation pipeline and product launches targeting convenience and protein-oriented lifestyles, is shifting the product mix toward higher-margin categories and is expected to improve net margins and top-line growth.

Want to see what is sitting behind that fair value gap? The story hinges on how fast margins rebuild and where earnings settle against a lower future P/E. Curious which revenue and profit assumptions need to line up for that to work?

Put simply, the narrative ties a higher fair value to a path where earnings grow meaningfully from today, profit margins step up from current low levels, and Tyson trades on a future P/E multiple below where the broader US Food group sits. Those expectations are filtered back to today using a 6.96% discount rate, so small shifts in growth, profitability, or required return can move that $69.08 figure.

For context, analysts in this narrative are working with steady but not rapid revenue expansion, a meaningful lift in profit margins over the next few years, and earnings in the low single digit billions. On top of that, they are assuming the share count stays broadly flat and that investors are comfortable valuing those future earnings at a P/E multiple in the low teens.

As always, the usefulness of this fair value depends on how closely your own expectations match those inputs and how you view Tyson's position across beef, pork, chicken, and prepared foods.

Result: Fair Value of $69.08 (UNDERVALUED)

However, the story can change quickly if cattle supply constraints keep Beef earnings under pressure or if input cost inflation squeezes Prepared Foods margins again.

Another angle on valuation

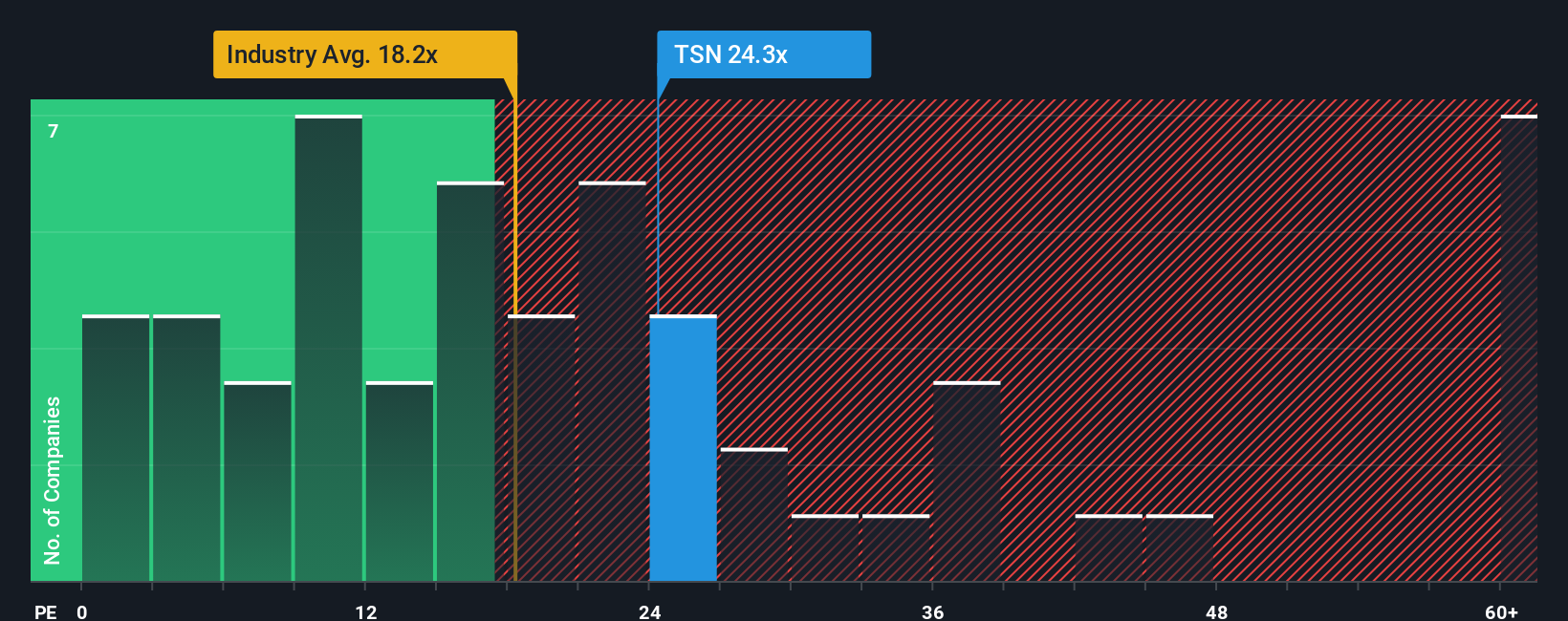

The fair value narrative points to Tyson Foods trading 52.7% below an estimated worth, yet the current P/E of 114.8x is far above both the US Food industry at 22.8x and an estimated fair ratio of 37x. That gap raises a simple question for you: is the share price already running ahead of near term earnings power?

Build Your Own Tyson Foods Narrative

If parts of this narrative do not line up with how you see Tyson Foods, take it as a starting point, pull apart the assumptions, and shape a version that truly reflects your own view, all in just a few minutes with Do it your way.

A great starting point for your Tyson Foods research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Tyson Foods has sharpened your focus on quality and value, do not stop here. Use these curated shortlists to pressure test and broaden your watchlist today.

- Zero in on quality at a discount by reviewing our list of 55 high quality undervalued stocks identified by their cash flows and balance sheet strength.

- Prioritize resilience by checking companies in our 81 resilient stocks with low risk scores that our model scores as relatively robust on business and financial risk.

- Get ahead of the crowd by scanning our screener containing 25 high quality undiscovered gems before the rest of the market starts paying attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.