Assessing UFP Industries (UFPI) Valuation As Profitability And Returns Face Ongoing Pressure

UFP Industries, Inc. UFPI | 93.02 | -3.23% |

Why UFP Industries’ recent trends are back in focus

UFP Industries (UFPI) is back under the microscope after ongoing declines in unit sales, earnings per share, and returns on capital over the past two years raised fresh questions about the durability of its profit drivers.

At a share price of $112.72, UFP Industries has seen strong recent momentum, with a 30 day share price return of 18.82% and a 90 day share price return of 22.52%. This comes even as the 1 year total shareholder return shows a decline of 2.23%, compared with its 5 year total shareholder return of 92.16%.

If this mix of near term strength and longer term volatility has you looking wider, it could be a good moment to scan 22 top founder-led companies as potential next ideas.

With earnings pressure, a recent share price surge and a value score of 3, the key question is whether UFP Industries is quietly undervalued right now or whether the market is already factoring in any future growth.

Most Popular Narrative: 6.1% Undervalued

Panayiotis sets fair value for UFP Industries at $120 per share, which sits above the last close of $112.72 and frames a mildly optimistic outlook.

Catalysts

• Cost Reductions: Over $70M in annualized savings from facility consolidation and SG&A cuts could boost margins.

• Acquisitions: Recent deals may enhance growth.

• Share Repurchases: A $200M program could support the stock.

• Market Recovery: A rebound in housing/construction demand would benefit UFP.

Assumptions

• 9% EPS growth to 2025 ($7.42), per consensus.

• 3% long-term revenue growth, as forecasted.

• 12% discount rate and 16x P/E reflect UFP’s risk and prospects.

Risks

• Earnings Weakness: Further misses or downgrades (e.g., Wedbush cut 2025 EPS to $7.36 from $7.42).

• Economic Slowdown: Impacts construction demand.

• Competition: Pricing pressure in a cyclical industry.

• Volatility: Beta of 1.45 indicates higher risk.

If you want to see how projected earnings growth, modest revenue expansion and a chosen profit multiple all work together in this fair value, the full narrative lays out the entire playbook in plain numbers.

Result: Fair Value of $120 (UNDERVALUED)

However, this depends on earnings remaining stable. Any further downgrades or a weaker construction market could quickly challenge the optimistic fair value story.

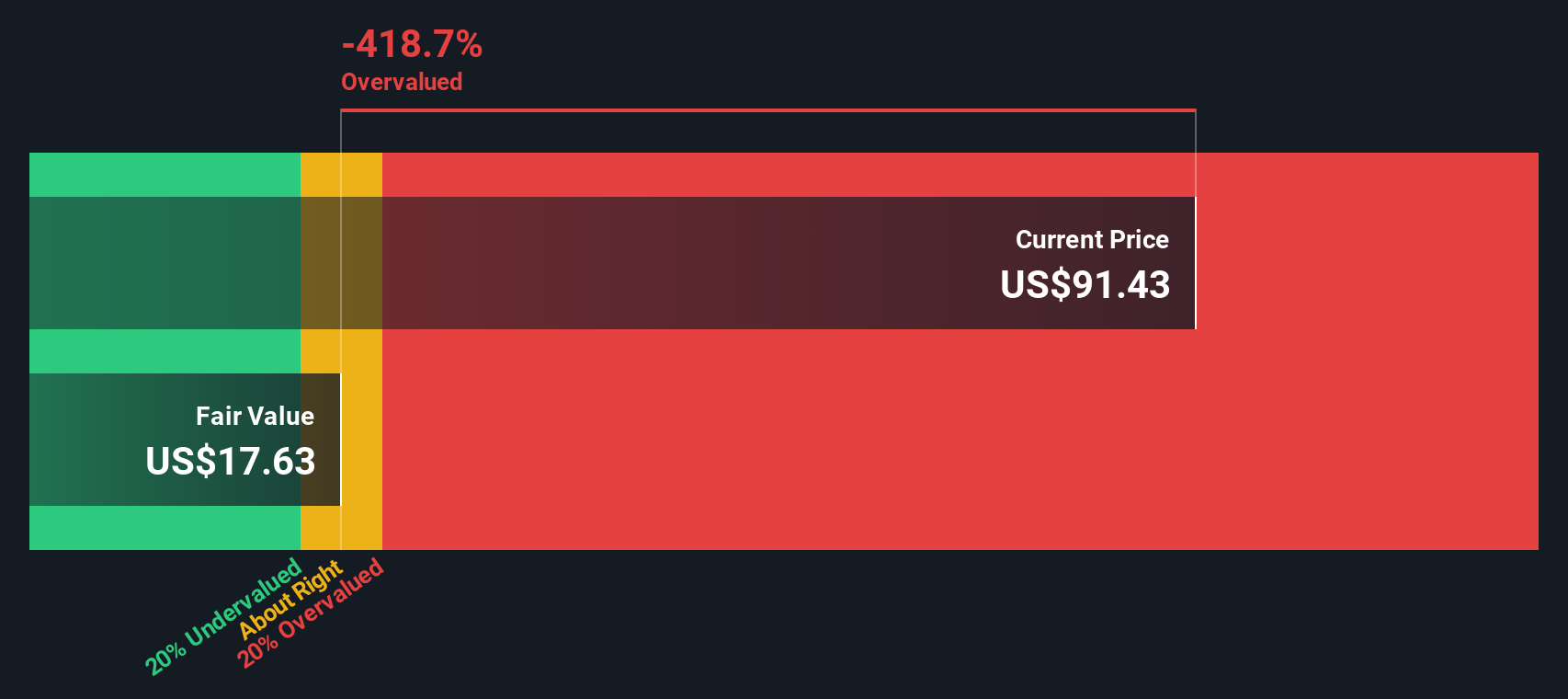

Another View: Our DCF Model Sees Things Differently

Panayiotis’ fair value of $120 suggests UFP Industries looks mildly cheap, but our DCF model points the other way. On those cash flow assumptions, fair value comes out at $70.56, which would put the current $112.72 share price in overvalued territory. So which story do you trust more: earnings multiples or cash flows?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out UFP Industries for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 55 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own UFP Industries Narrative

If you look at the numbers and reach a different conclusion, or simply prefer to test your own assumptions, you can build a custom view in just a few minutes, starting with Do it your way

A great starting point for your UFP Industries research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If UFP Industries has sharpened your focus, do not stop here. Broaden your watchlist with a few targeted stock ideas that fit different goals and risk levels.

- Chase potential value opportunities by reviewing 55 high quality undervalued stocks that currently screen well on quality and pricing metrics.

- Strengthen your income focus by scanning 15 dividend fortresses that pair higher yields with resilient dividend profiles.

- Dial up resilience by checking 81 resilient stocks with low risk scores that score well on stability and lower overall risk.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.